This article was originally published in Financial Express. Click here to read it.

Let’s say you have some money requirement (read as financial goal) coming up within the next five years. You want to save and invest for it.

Where would you invest?

There is a natural temptation to choose investment options such as Equity funds that can potentially offer higher returns.

Why?

Simple. Higher the return, lower the amount we need to save.

Though there is a risk of higher volatility (read as higher temporary declines) with equity investments, this often gets brushed off with the thought that it can’t be THAT bad or it won’t happen to us.

But is it really the case?

Let’s crunch the numbers!

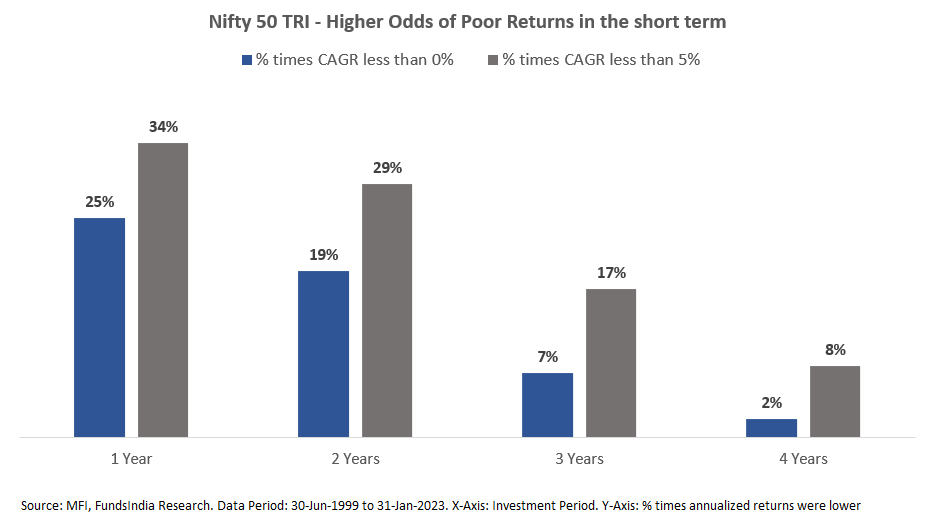

What are the chances of losing money in equities in the short term?

Historically, over 1-year periods, the equity market (represented by Nifty 50 TRI) delivered negative returns 25% of the times i.e. you would have lost money one in four times if you had invested with a 1-year timeframe.

Over 3-year periods, your returns were negative 7% of the times.

The odds of subpar returns are even more significant. You would have made annualized returns lower than inflation (assuming inflation to be 5%), 34% of the times over 1-year periods and 17% of the times over 3-year periods.

This makes it pretty clear that there is a decent chance of us ending up on the wrong side of odds.

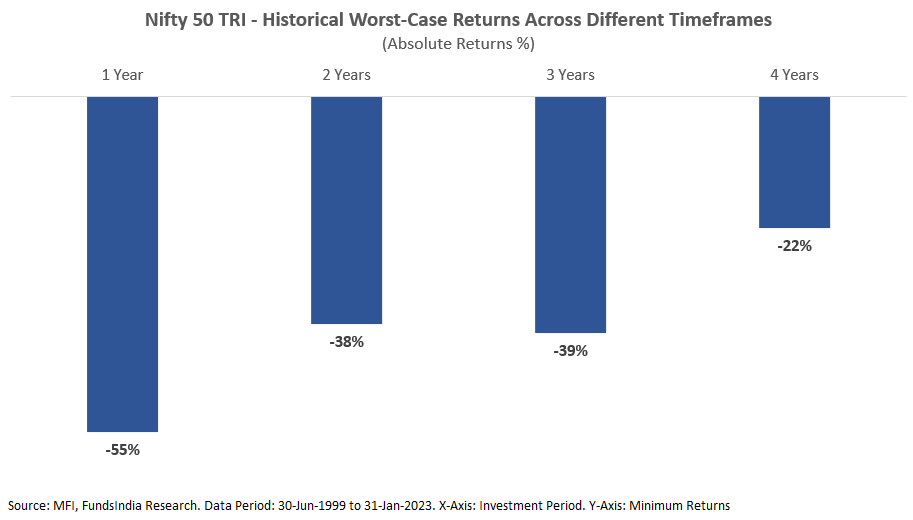

If we end up on the wrong side of odds, how bad can the impact be?

Over 1-year periods, in the worst case, your equity investments would have fallen a whopping 55%!

And over 3-year periods, equity investments fell up to 39%.

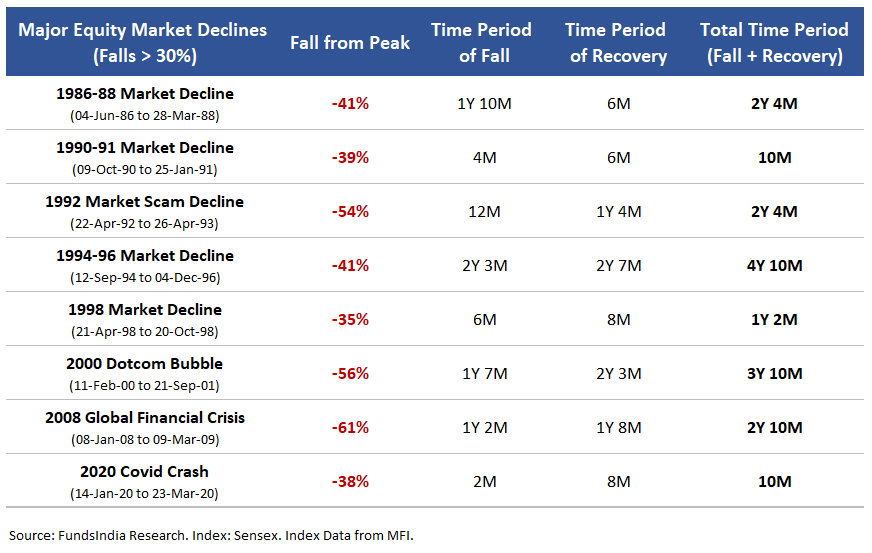

These sharp declines are almost always a result of major market falls (declines over 30%). While such declines are not very frequent, they have historically occurred once or twice every decade.

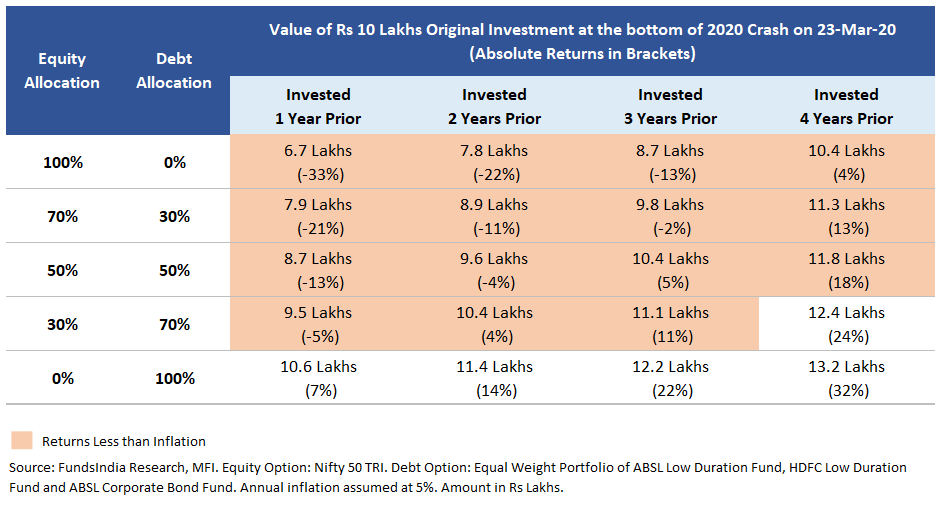

To get a better sense of this, let us understand the impact of such declines by taking a recent example

During the 2020 Covid Crash, the Nifty 50 TRI fell 38% from its all-time highs as on 23-Mar-20.

If you had made an all-equity investment of Rs 10 lakhs one year prior (on 23-Mar-19), the investment value would have fallen to Rs 6.7 lakhs (losing 33%).

When the holding period was two years, the loss was Rs 2.2 lakhs (22%).

And when the investments were held for four years, you would not have lost money. But the returns were just 4% (in absolute terms) much lower than inflation.

The return outcomes turned out to be poor, even when the equity allocation was relatively lower (50-70% Equity). For instance, investment with only 50% in equities (and remaining in debt) made two years prior would have lost 4%.

Why does this happen?

Using history as a rough guide, major declines (falls > 30%) and subsequent recoveries together have usually taken almost 1-4 years to play out.

Given this, your equity investments might not always recover in time to cover your short term goals. And at higher equity exposure levels, you run the risk of missing out on your goals (due to the chances of getting hit by a large market fall).

Taking all these into account, here is how you can plan for your short term goals (those coming up in the next 5 years)

1. If the time to goal is less than 3 years, invest only in debt funds

2. If the time to goal is 3-5 years

- Timeline is not flexible (Eg: college tuition fees for your children) : Invest only in debt funds

- Timeline is flexible (Eg: buying a house, vacation plans) : You can choose to allocate some portion to equities. This can be done by investing up to 30% in diversified equity funds and 70% into debt funds or by going for Equity Savings Funds or Dynamic Asset Allocation Funds.

Parting Thoughts

When it comes to short-term money goals, it is always better to go for higher debt allocation (along with higher savings rate).

While the journey might not be exciting, you are much more likely to get to your destination!

Happy Investing 🙂