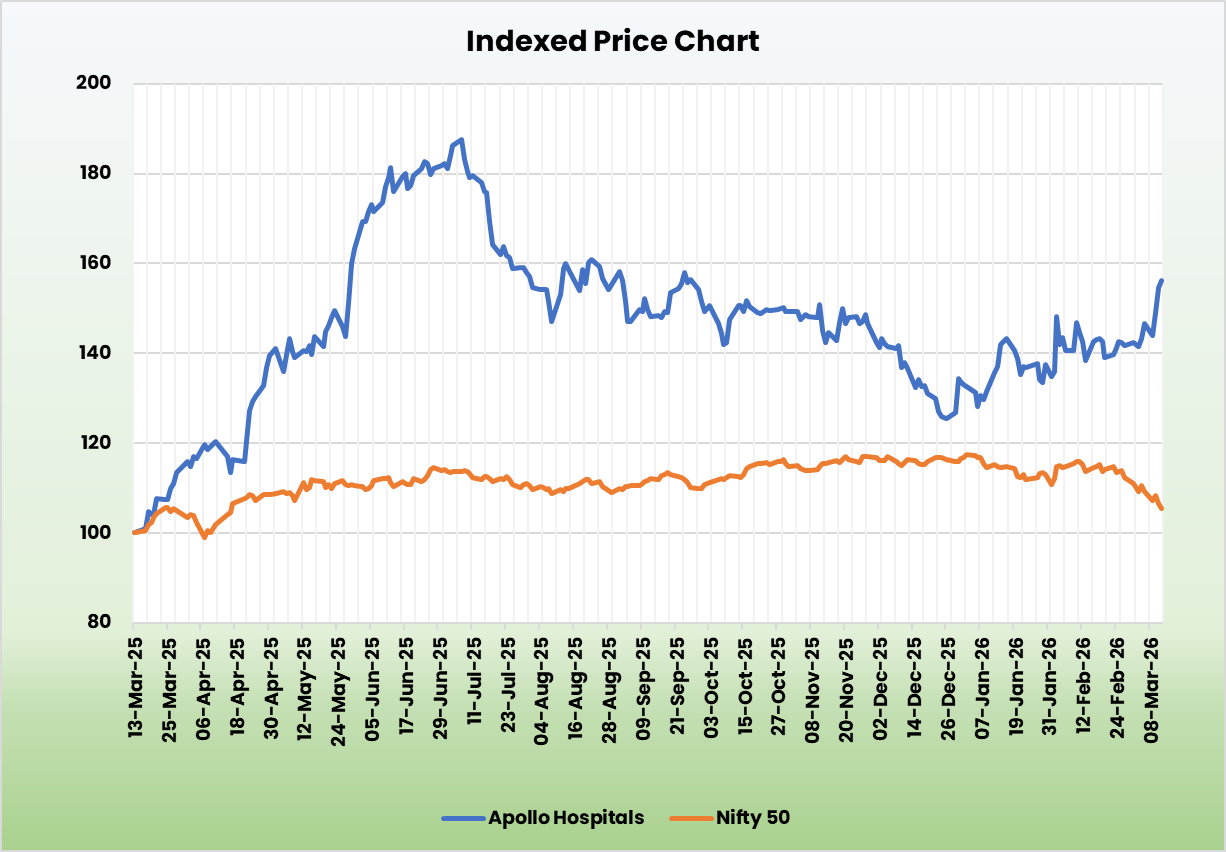

Apollo Hospitals Enterprise Ltd. – Touching Lives

Apollo Hospitals Enterprise Limited, incorporated in 1979 and headquartered in Chennai, Tamil Nadu, is India’s largest integrated healthcare provider, operating across three verticals: Healthcare Services (hospitals), Diagnostics & Retail Health (AHLL), and Digital Health & Pharmacy Distribution (Apollo HealthCo). The company operates a pan-India network of 76 hospitals with 9,561 operational beds, supported by 3,328 AHLL out-of-hospital touchpoints and 7,113 Apollo Pharmacy stores as of Q3FY26. Apollo’s integrated model creates a continuity-of-care ecosystem, with hospital-generated demand feeding downstream into pharmacy dispensing, diagnostics, and the Apollo 247 digital platform, serving over 46 million registered users. The company holds a dominant position in high-acuity CONGO-T specialties (Cardiac, Oncology, Neurosciences, Gastroenterology, Orthopaedics, Transplants).

Products and Services

The company operates through three key verticals:

- Apollo Hospitals Enterprise Ltd – Operates through a wide network of hospitals that provide tertiary and quaternary care with specialisations in cardiology, oncology, neurology, gastroenterology, transplants and robotic surgery.

- Apollo HealthCo Ltd – Includes Apollo Pharmacy – India’s largest pharmacy distribution network and Apollo 247 – digital health platform that offers teleconsultations, online pharmacy deliveries, home diagnostics, and insurance services.

- Apollo Health & Lifestyle Ltd – Provides shortstay facilities, boutique birthing centers, multi-speciality clinics, diagnostic centres, dental and dialysis facilities, fertility services and preventive care.

Subsidiaries – As of FY25, the company has 39 subsidiaries, 4 associates and 3 joint ventures.

Investment Rationale

- Improvement in Operational Metrics – The company has seen steady improvement in operating efficiency across its core hospital business, supported by stronger demand and better capacity utilization. Bed occupancy has improved significantly from ~55% in FY21 to ~68% in FY25, reflecting stronger patient traction and improved asset productivity. In Q3FY26, the Healthcare Services segment reported 14% YoY revenue growth, driven by a balanced mix of ~5% volume growth, ~4% case mix improvement, and ~5% pricing gains. Group-wide occupancy remained healthy at around 67%, indicating stable demand and efficient utilization of existing capacity. Average revenue per inpatient increased by 11% to Rs.180,917 during the quarter, driven by higher clinical intensity in CONGO-T specialties. Over 9MFY26, ARPP has grown by ~10%, reflecting improving realizations and pricing power. Management also expects margins to remain stable despite ongoing expansion, supported by operating leverage and improving case mix.

- Capacity Additions and Expansion Strategy – The company is undertaking a significant capacity expansion to strengthen its presence across key metropolitan healthcare markets. In Q3FY26, the company operationalized 75 beds at its Pune facility and 30 beds at Defence Colony as part of its ongoing network expansion. Over the next five years, Apollo plans to add around 4,400 capacity beds, translating into roughly 3,600 census beds, which will meaningfully expand its treatment capacity. Projects expected to be commissioned between FY26 and FY27 include facilities in Pune, Sonarpur (Kolkata), Gachibowli (Hyderabad), Gurugram, and Sarjapur, along with expansions at Jubilee Hills, Secunderabad, Malleswaram, and Mysore. These projects together are expected to add about 2,029 total beds (around 1,660 census beds) in the near term. The expansion pipeline includes a mix of asset acquisitions, greenfield developments, leased facilities, and brownfield expansions, enabling the company to scale efficiently while maintaining capital discipline. The total expansion capex is estimated at around Rs.8,200 crore, with approximately Rs.5,400 crore yet to be deployed. As a result, the company’s total census bed capacity is expected to increase from about 9,561 beds in Q3FY26 to nearly 13,100 beds over the medium term. This capacity addition should support sustained volume growth and strengthen Apollo’s positioning in high-demand urban healthcare markets.

- Q3FY26 – In Q3FY26, Apollo reported revenue of Rs.6,477 crore, up 17% YoY. EBITDA stood at Rs.965 crore, up 27% YoY, with EBITDA margins expanding to 14.9% from 13.8% in Q3FY25. PAT came in at Rs.502 crore, up 35% YoY. Within Healthcare Services, revenue grew 14% YoY to Rs.3,183 crore with hospital EBITDA margins at 24.8% (+73 bps YoY); Average Revenue per In-Patient grew 11% YoY to Rs.1,80,917.

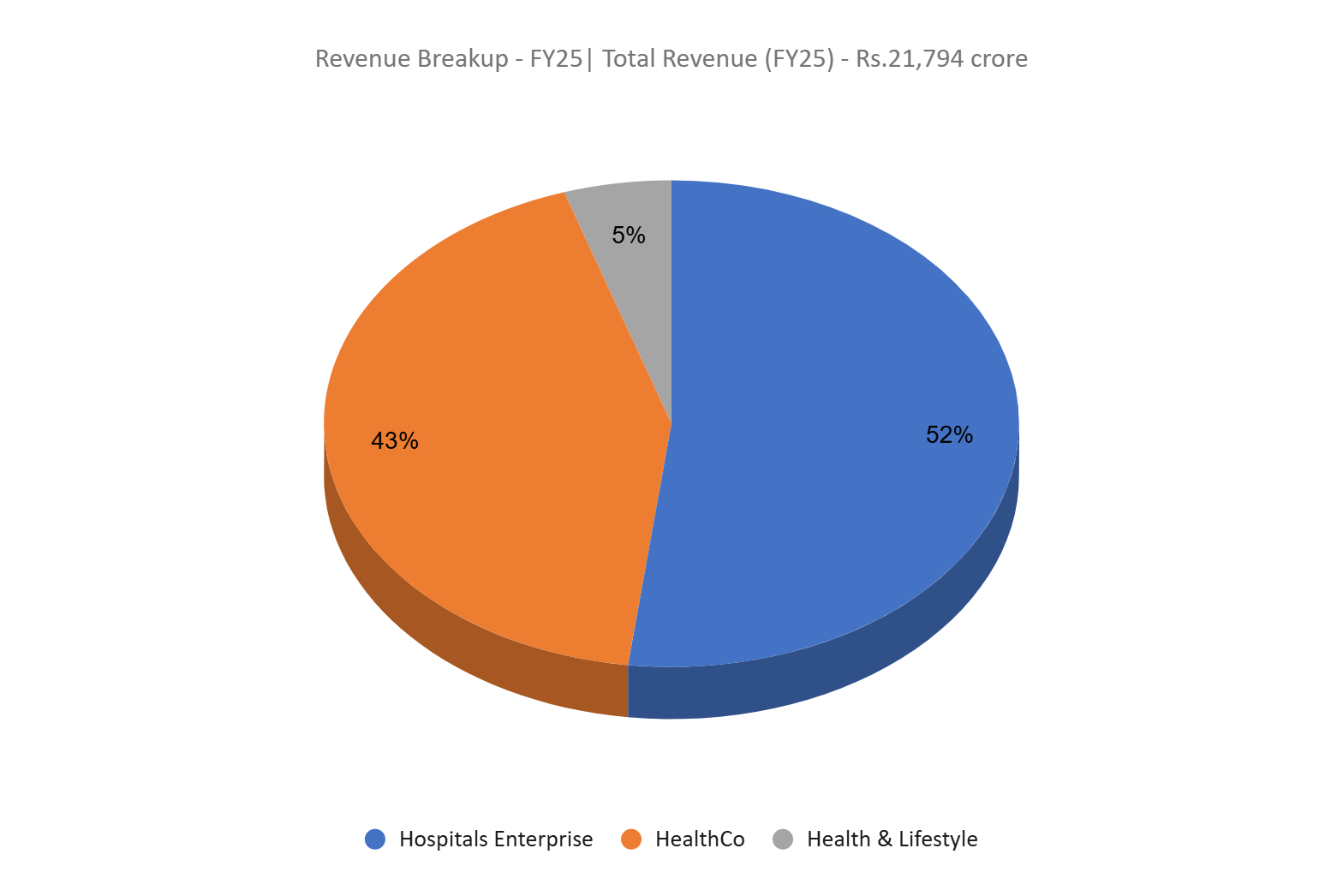

- FY25 – For FY25, Apollo reported a revenue of Rs.21,794 crore, up 14% YoY. EBITDA grew 26% YoY, to Rs.3,022 crore. PAT stood at Rs.1,446 crore, up 61% YoY from Rs.899 crore in FY24.

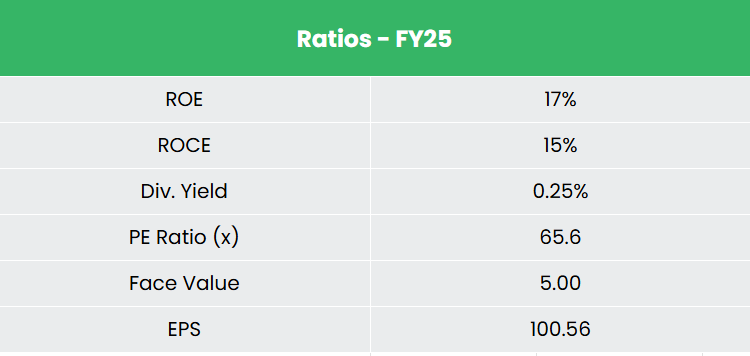

- Financial Performance – The 3-year revenue and net profit CAGRs stand at 14% and 18% respectively (FY23–25). Notably, TTM revenue and net profit CAGRs have improved to 15% and 39% respectively. The 3-year average ROE and ROCE are approximately 15% each, and the company carries a debt-to-equity ratio of 0.88x, serviced by a strong interest-coverage of ~6.6.

Industry

The Indian healthcare sector is among the fastest-growing segments of the domestic economy, supported by favourable demographics, rising income levels, and improving access to medical services. The sector has seen unprecedented growth in the recent years, driven by expansion across hospitals, pharmaceuticals, diagnostics, and digital health. Healthcare spending as a share of GDP stood at 3.3% in 2022 and is expected to rise to 5% by 2030, supported by a Union Budget FY26 allocation of Rs.99,858 crore, a 9.8% increase YoY. The hospital segment specifically was valued at US $126 billion in FY24 and is projected to grow at ~8% CAGR to US $193.6 billion by FY32, with India’s structural bed shortfall of ~3 million beds providing long-run demand visibility for organised private operators. Demand in Tier II and III cities is projected to grow at 16-18% CAGR, outpacing metro growth of 12-14%, reflecting the next leg of expansion for established networks.

Growth Drivers

- Favourable FDI Policy – 100% FDI is permitted under the automatic route for greenfield hospital projects; cumulative FDI inflows into hospitals and diagnostic centres reached US $12.25 billion between April 2000 and June 2025

- Rising Demand from Demographics and Disease Burden – Life expectancy is projected to reach 84 years by 2045, and lifestyle diseases now account for ~50% of in-patient spending, driving sustained demand for specialised care.

- Expanding Health Insurance Coverage – Total health insurance premiums reached Rs.1,18,688 crore in FY25, with standalone health insurers projected to grow 20–21% in FY26, directly expanding the addressable market and improving payor mix for organised hospital chains.

Peer Analysis

Competitors – Max Healthcare Institute Ltd, Fortis Healthcare Ltd, etc.

Compared to its peers, Apollo Hospitals demonstrates superior scale, return ratios, and a strong cash position. Apollo is the only player in the peer set with a fully integrated three-vertical structure spanning hospitals, retail health, and omni-channel pharmacy, creating cross-referral synergies, and patient data driven moat.

Outlook

The outlook for Apollo Hospitals remains positive, supported by a strategic focus on improving case mix and expanding high-complexity treatments across its flagship hospitals. The company is increasingly prioritizing complex procedures and specialty care, which should support higher realizations and stronger margins over time. In parallel, Apollo is pursuing multiple growth levers including expanding surgical volumes, improving occupancy levels, and enhancing operational efficiency across its network. A key growth driver will be the operationalisation and expansion of around 15 hospitals with a combined capacity of nearly 4,300 beds across both new and existing markets. These additions are expected to strengthen the company’s presence in high-demand urban clusters while supporting long-term volume growth. Combined with rising patient intensity and improving pricing power, these initiatives are expected to drive sustainable earnings growth and support improvement in return on capital employed (ROCE) over the medium term.

Valuations

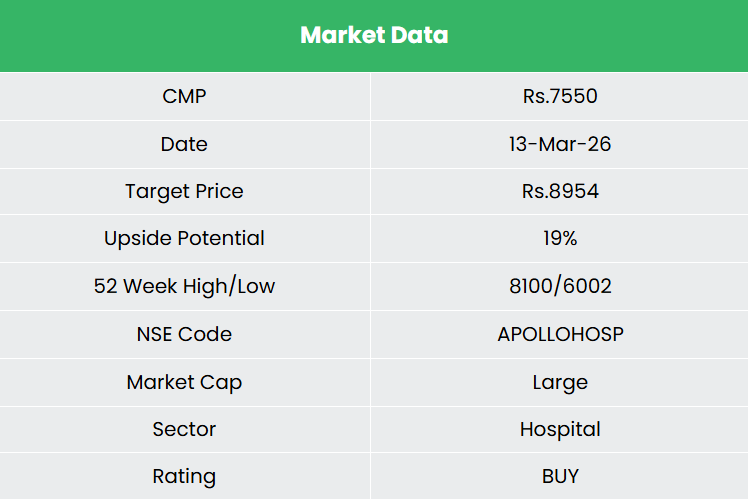

We believe the company is well positioned to capitalise on the rising healthcare demand, supported by consistent bed additions and operational efficiencies. We recommend a BUY rating in the stock with the target price (TP) of Rs.8,954, 64x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

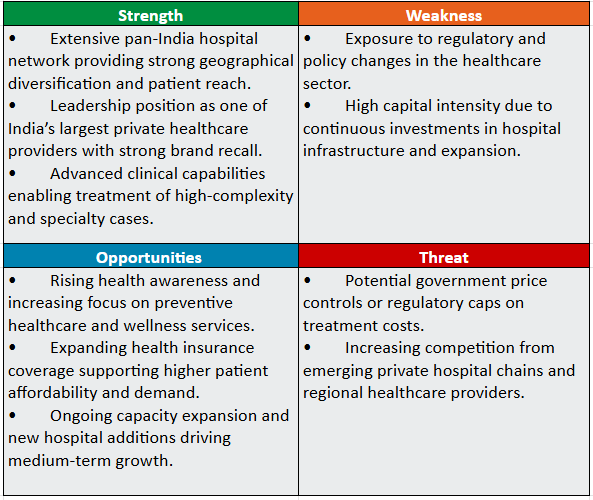

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.