Hindustan Zinc Ltd. – Zinc and Silver of India

Hindustan Zinc Limited (HZL), incorporated in 1966 and headquartered in Udaipur, Rajasthan, is the world’s largest integrated zinc producer and India’s only primary silver producer. A subsidiary of Vedanta Limited, with the Government of India retaining a significant stake.

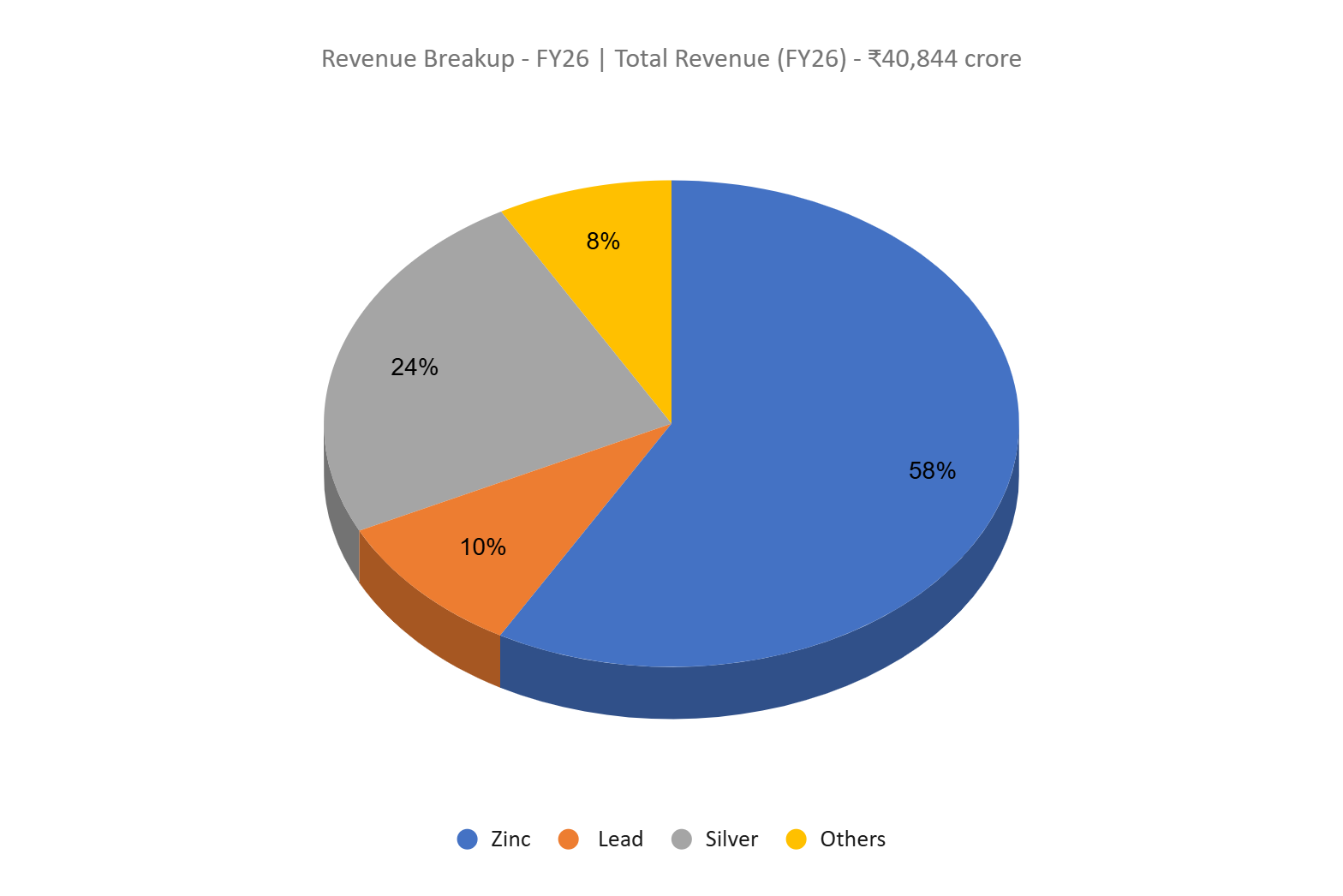

HZL’s primary revenue streams are zinc (58% of FY26 revenue), silver (24%), lead (10%), and by-products including sulfuric acid and cadmium. Its mining portfolio spans five underground mines, underpinned by record ore resources and reserves of 468.6 million tonnes as of FY26, representing 25+ years of mine life. On the smelting side, HZL operates integrated facilities at Chanderiya, Dariba, and Debari, with a current refined metal capacity of approximately 1,129 Ktpa of zinc and lead combined.

Beyond its core metals, HZL holds composite licenses for three critical mineral blocks – potash (Rajasthan), tungsten (Andhra Pradesh), and rare earth elements (Uttar Pradesh) – as part of its multi-metal diversification strategy.

Products and Services

The company offers a diverse portfolio primarily consisting of refined zinc, lead, and silver, along with value-added products like specialized zinc alloys, die-casting alloys, and its low-carbon green zinc, etc. Additionally, the company provides mineral exploration services and is expanding its offerings to include DAP/NPK fertilisers.

Subsidiaries – As of FY26, the company has 5 subsidiaries.

Investment Rationale

- Structural Cost Leadership Creating a Durable Margin Floor – The company achieved its lowest-ever zinc cost of production since underground transition at $903/MT in Q4FY26, and closed the full year at $959/MT – well below its own guided range of $1,000/MT. What makes this particularly compelling for an investor is that this cost reduction is not a one-quarter anomaly driven by commodity luck, but a structural shift powered by multiple concurrent levers: domestic coal usage surged to 64% in Q4 (versus ~53% for the full year), mine grades improved to 7.9% in Q4 versus a 7.5% annual average (and management has confirmed that every 10 bps of grade improvement saves ~$7/MT), renewable energy consumption reached 18% and is guided to jump to 30 – 35% in FY27 and 70% by FY28 (with every 2% RE increase equating to $1/MT cost savings – implying ~$25/MT further reduction potential by FY28), and byproduct realization from sulphuric acid (~₹1,400 crore annually) and ancillary waste-to-wealth businesses (~₹600 crore, growing to ₹1,200 – 1,500 crore) are increasingly acting as cost offsets. Even with FY27 COP guidance at $975 – 1,000/MT reflecting geopolitical uncertainty on diesel, propane, and explosives pricing, the structural tailwinds are intact and the company has a demonstrated track record of beating its own guidance. For a zinc price of $3,241/MT in Q4 and a COP of $903/MT, the spread is nearly $2,338/MT – a margin that very few global zinc producers can match, and one that provides a significant buffer even if LME zinc were to correct toward the $2,800 – 2,900/MT range that bears are projecting for H2 FY27.

- Silver as a Structurally Re-Rating Asset – Silver is emerging from a by-product into a core earnings driver, contributing ~45% of profitability in FY26, with the company building clear optionality to scale silver alongside its zinc-led ore base. Management indicates that at elevated LME zinc prices ($3,100 – 3,400/MT), it is optimal to prioritize zinc volumes even at the expense of silver, but if zinc moderates to $2,800 – 3,000/MT while silver remains strong (> $60/toz), the mix would tilt toward higher lead and silver output, potentially pushing silver volumes beyond 700 MT effectively embedding a natural hedge in the business where silver upside offsets weaker zinc realizations. This flexibility is further supported by three distinct silver growth triggers: (a) the Hot Acid Leaching plant at Dariba, a first-of-its-kind in India, expected to recover ~27 MT of silver annually from jarosite waste with commissioning in 2QFY27, (b) the upcoming 250 ktpa Debari smelter with an integrated fumer to enhance silver recovery, and (c) a 10 Mtpa tailings reprocessing project (₹3,823 crore, targeted by 4QFY28) with potential to recover up to ~3 ktpa of silver equivalent from legacy waste. With FY27 guidance at ~680 MT (and already ~664 MT on a silver-equivalent basis including MIC sales), alongside medium-term targets of 1,000 MT and 1,500 MT at 2 Mtpa scale, the company offers a leveraged play on the silver upcycle, with downside supported by zinc’s strong domestic demand and its industry-leading cost position.

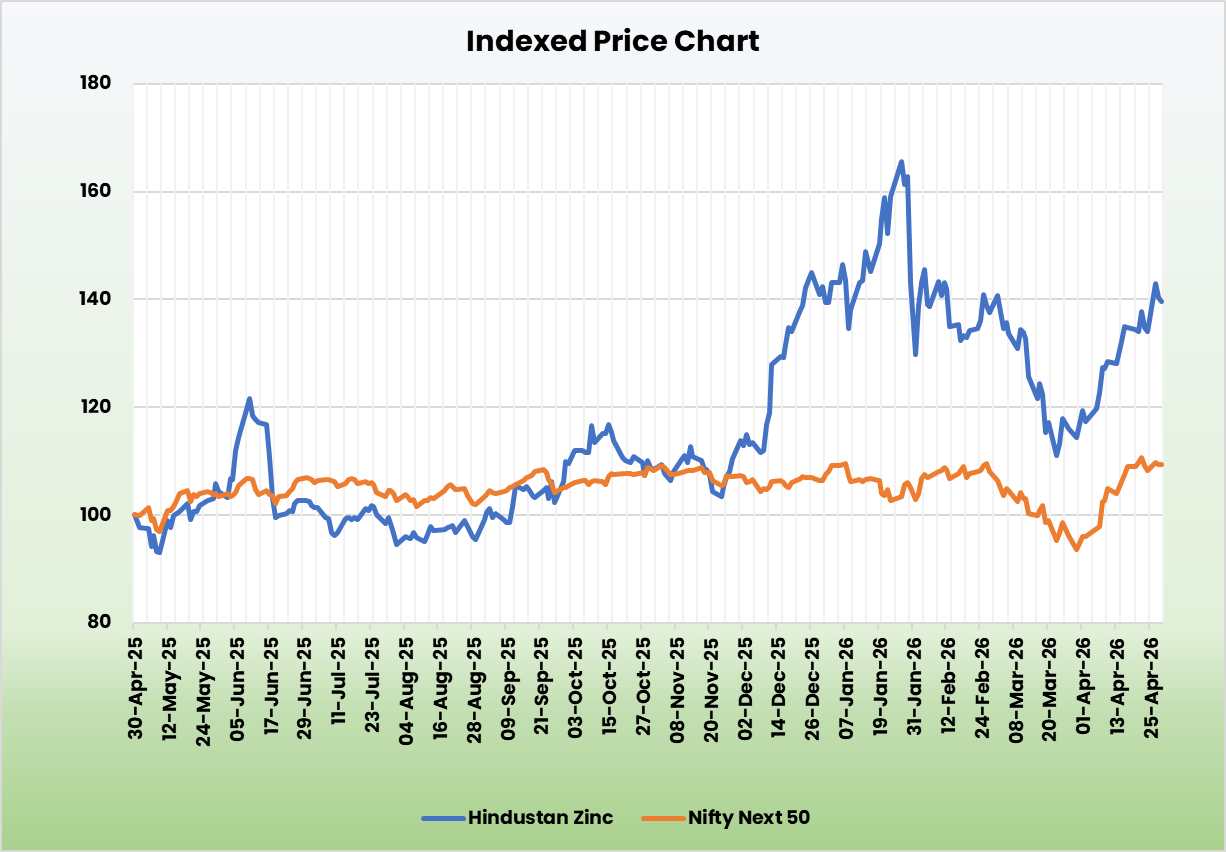

- Q4FY26 – HZL reported consolidated revenue of ₹13,544 crore, up 49% YoY, with EBITDA rising 61% YoY to ₹7,747 crore and PAT growing 68% YoY to ₹5,033 crore.

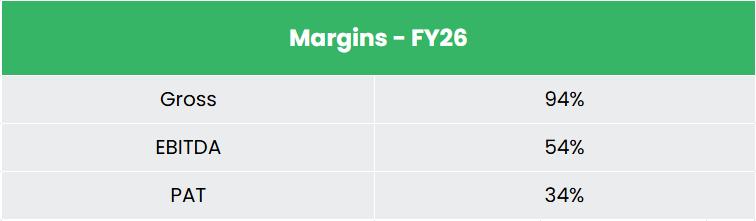

- FY26 – Consolidated revenue grew 20% YoY to ₹40,844 crore, with EBITDA at ₹22,162 crore up 27% YoY, posting a margin of 54% (300bps improvement), and PAT at ₹13,832 crore, up 34% YoY.

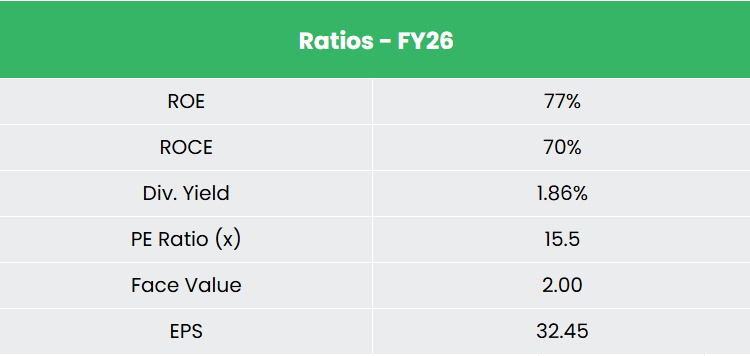

- Financial Performance – The 3-year revenue and net profit CAGR stands at 6% and 10% respectively between FY24-26. Notably, the TTM revenue and net profit growth have accelerated to 20% and 33%. The 3-year average ROE and ROCE is at 69% and 59% respectively. The company has a debt-to-equity ratio of 0.39.

Industry

India’s zinc demand is projected to double over the next 5 – 10 years, driven by sustained infrastructure and steel investments. Demand is anchored by galvanizing, which dominates zinc end-use and is directly linked to India’s steel sector – the world’s second-largest, with crude steel production at 151.14 MT in FY25 and a targeted capacity of 300 MT by 2030. Steel demand is expected to grow ~10%, with building and infrastructure contributing 60–65% of consumption.

On the lead front, demand is supported by automotive battery growth and industrial applications, while silver, a key by-product for integrated producers benefits from accelerating solar PV deployment as India’s installed power capacity reached 505 GW in October 2025.

Growth Drivers

- Steel and infrastructure capex: Crude steel capacity is targeted at 300 MT by 2030 (vs. 151.14 MT in FY25) with steel demand growing ~10%, while Union Budget FY26 raised infrastructure outlay 11.1% to ₹11.2 lakh crore (US$ 129 billion) – directly anchoring galvanized zinc volumes.

- Silver demand from renewables – India’s renewable build-out toward 50% non-fossil capacity by 2030 (from 49% in October 2025) drives silver demand via solar PV, supporting realisations for integrated producers where silver is a high-margin by-product.

- Favourable Policies: Policy tailwinds include the National Critical Mineral Mission (January 2025) with a ₹16,300 crore (US$ 1.9 billion) outlay and expected ₹18,000 crore (US$ 2.1 billion) PSU co-investment, alongside the MMDR Amendment Bill 2025 which removes captive-sale caps, simplifies deep-seated mineral leasing, and introduces mineral exchanges – collectively strengthening the operating environment for integrated zinc-lead-silver producers.

Peer Analysis

Competitors: Hindalco Industries Ltd, Hindustan Copper Ltd, etc.

Among domestic listed peers, HZL is in a category of its own as India’s only integrated zinc-lead-silver producer. Among the broader non-ferrous metal players, HZL stands out for its exceptional return profile with a 3-year average ROE and ROCE of ~69% and ~59%, respectively driven by industry leading margins, and strong cash conversion.

Outlook

Hindustan Zinc is entering what its management describes as a “defining phase of growth” – transitioning from 1.1 Mtpa to 2 Mtpa metal capacity by FY30 through the board-approved ₹12,000 crore Debari smelter and ₹3,823 crore tailings reprocessing plant, effectively doubling the earnings base over the next four years. FY27 guidance of 1,150 KT mined metal, 1,100 KT refined metal, and 680 MT silver funded through $500 – 600 million growth capex entirely from internal accruals signals a business that is simultaneously expanding and self-financing, with limited balance sheet risk. With a minimum 30% PAT dividend policy intact, investors get both the compounding upside of a capacity doubling cycle and an income stream – making HZL a rare combination of a growth stock and a yield play, anchored in India’s infrastructure decade and a structural global silver deficit.

Valuations

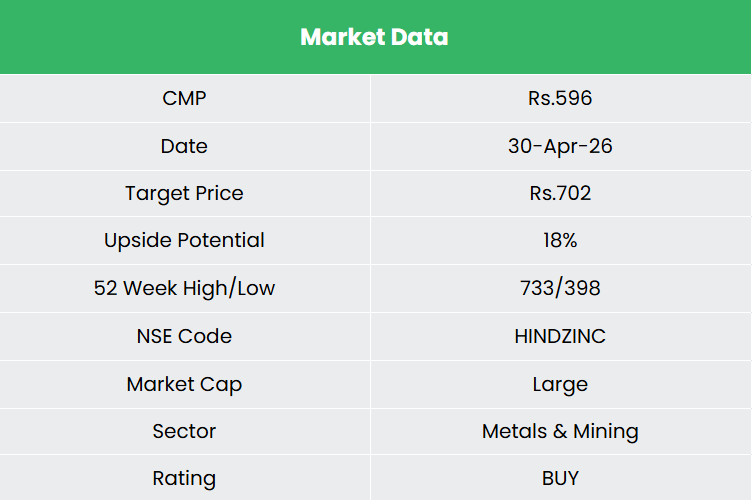

We believe Hindustan Zinc is well-positioned to sustain its growth momentum given its industry-leading cost structure, a clear 2x capacity expansion roadmap to 2 Mtpa by FY30, and a domestic zinc market where demand is only set to accelerate as India marches toward 300 Mtpa steel production by 2030. We recommend a BUY rating in the stock with the target price (TP) of Rs.702, 18x FY28E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.