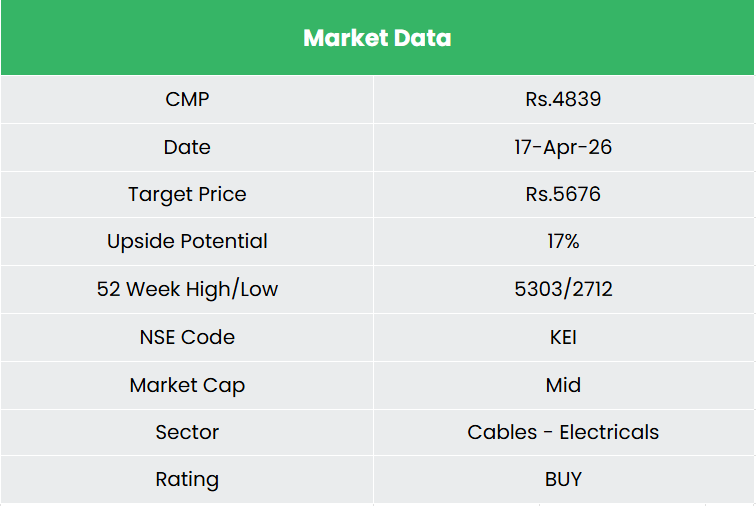

KEI Industries Ltd. – Cables well connected

KEI Industries Limited (KEI), incorporated in 1992 and headquartered in New Delhi, is one of India’s leading manufacturers of wires and cables. Its product portfolio spans Extra-High Voltage (EHV) cables up to 400 kV, HT and LT power cables, control and instrumentation cables, specialty cables (solar, rubber, EV, fire-survival, ESP, MVCC), house and winding wires, and stainless-steel wires. The company is additionally forward integrated into EPC services for power transmission, distribution, and sub-station projects.

KEI operates nine manufacturing plants across Rajasthan, Dadra & Nagar Haveli, and Gujarat, supported by an in-house NABL-accredited R&D facility. On the distribution side, KEI serves 2,000+ institutional customers and reaches retail markets through a pan-India network of over 2100 active dealers, 27 depots, and 38 marketing offices. Its export presence spans 60+ countries across four overseas offices. As of 31st December 2025, KEI carried a consolidated order book of ₹37,243 Mn.

Products and Services

The company operates a diversified cables and EPC portfolio spanning EHV (up to 400kV), HT/LT power cables, and value-added segments such as instrumentation, control, and specialty cables (EV, solar, fire-resistant, marine and offshore). Revenue exposure is well distributed across core infrastructure and industrial end-markets, including power, oil & gas, renewables, railways, roads & highways, real estate, and telecom, providing demand visibility and reducing sector-specific cyclicality.

Subsidiaries – As of FY25, the company has an associate company and no other subsidiaries/joint ventures.

Investment Rationale

- Sanand Greenfield Expansion Driving the Next Phase of Growth – KEI’s Sanand greenfield expansion represents a decisive inflection point, transitioning the company from being capacity-constrained to structurally growth-enabled, with ~₹2,000 crore capex unlocking ~₹6,000 crore peak revenue potential over the next 2–3 years. With Phase 1 (LT/HT) already operational and full commissioning (including high-margin EHV) targeted by FY27, the facility not only adds scale but meaningfully upgrades product mix, being the only plant in India to manufacture the full cable spectrum including upcoming HVDC capabilities aligned with next-gen grid investments. This comes at an opportune time, with existing utilisation at ~76% and a strong order book (~₹3,700 crore), ensuring faster absorption and reducing execution risk. Management guidance of ~₹2,700 crore revenue from Sanand in FY27, scaling to full utilisation by FY29 (implying ~3–3.5x asset turns), indicates strong capital efficiency. Crucially, growth is expected to be margin-accretive, supported by operating leverage, increasing share of EHV and exports, and a structurally improving B2C mix. Backed by proven institutional credentials in global EHV markets, Sanand positions KEI to directly convert incremental capacity into high-quality export and domestic opportunities, making it a key driver of sustained revenue growth and profitability expansion.

- Structural Shift Toward High-Margin B2C Driving Earnings Quality – KEI’s increasing tilt toward the B2C (retail) segment, now contributing ~50%+ of revenues marks a structural improvement in business quality, with higher margins, better working capital cycles, and lower earnings volatility compared to the lumpy institutional segment. Supported by strong brand recall, expanding dealer/distributor network, and robust demand from real estate and housing, the wires segment (growing ~22–23%) is emerging as a consistent compounding engine. This shift not only enhances margin stability but also improves return ratios and cash flow visibility, making overall growth more durable and less cyclical.

- Q3FY26 – KEI reported consolidated net sales of ₹2,955 crore, up 19.5% YoY, with EBITDA rising 39% YoY to ₹354 crore and PAT growing 42.5% YoY to ₹235 crore. EBITDA margin expanded by ~170 bps YoY to 12.0% (vs 10.29% in Q3FY25), driven by a richer product mix with the export share rising to ~18% of sales and continued traction in the retail segment.

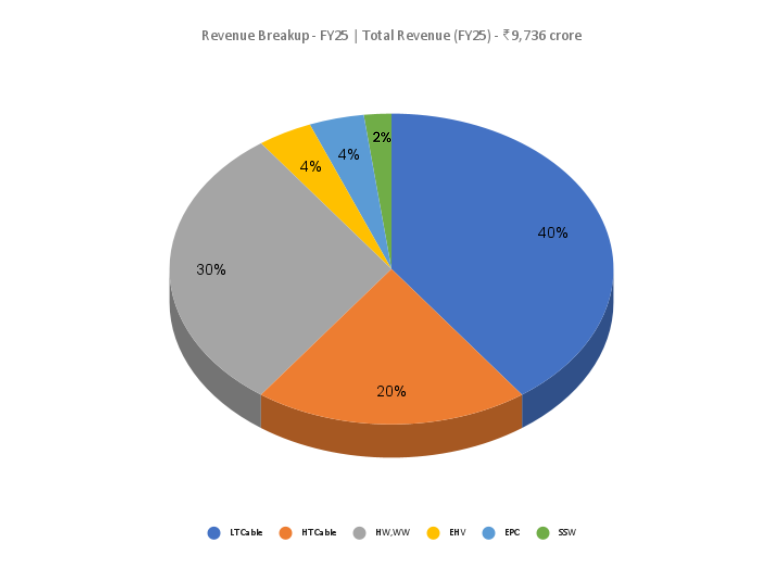

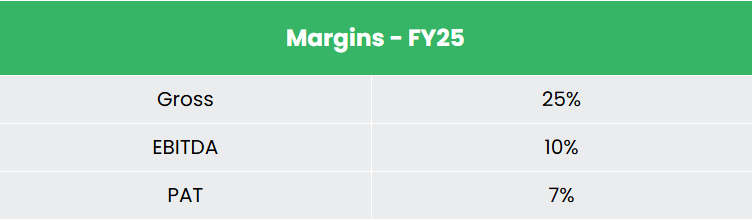

- FY25 – Consolidated net sales grew 20% YoY to ₹9,736 crore, with EBITDA at ₹1,063 crore up 20% YoY, posting a margin of 10.92%, and PAT at ₹696 crore, up 20% YoY.

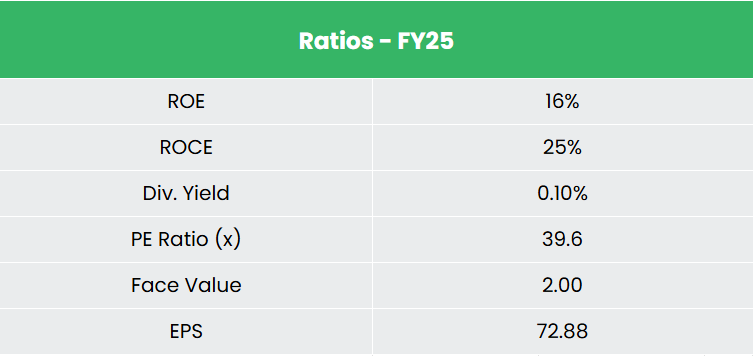

- Financial Performance – The 3-year revenue and net profit CAGR stands at 19% and 23% respectively between FY23-25. Notably, the TTM revenue and net profit growth stand at 22% and 35%. The balance sheet remains largely unencumbered, with a debt-to-equity ratio of 0.04, and the 3-year average ROE and ROCE are around 18% and 25% for FY23-25 period.

Industry

The Indian wires and cables industry constitutes approximately 39% of the broader electrical industry and is expected to grow at an 11 – 13% CAGR between FY24 and FY29, reaching approximately ₹1,20,000 crore by FY29. Exports have emerged as a high-growth segment – India’s wire and cable exports rose from ₹8,322 crore in FY20 to ~₹16,765 crore in FY24, with a further 8% YoY increase recorded between April and October 2024.

Power demand in India is projected to grow at a 5-7% CAGR between FY25 and FY29, reaching 2,160-2,180 BU. India’s installed power capacity stood at 475.2 GW as of 31st March 2025, of which renewable energy accounted for 220.1 GW (solar at 106 GW and wind crossing 50 GW). Under the National Electricity Plan (2022-32), installed capacity is targeted to reach 609 GW by FY32, with non-fossil sources accounting for 500 GW by 2030, requiring a cumulative investment of ₹33.6 trillion (US$ 384.5 Bn) over the decade. Within this, the T&D sector is set to receive ₹9.15 lakh crore of investment by FY32 – ₹4.2 lakh crore between 2022-27 and ₹4.9 lakh crore between 2027-32 – funding the addition of 1,91,474 ckm of transmission lines and 1,274 GVA of transformation capacity.

Growth Drivers

- Power sector capex and T&D expansion: Total power sector investment is projected to rise 1.7x from ₹14.7 lakh crore over FY19–24 to ₹24.5–25.5 trillion over FY25-29, with inter-regional transmission capacity targeted at 142,940 MW by FY27.

- Renewable energy transition: India’s installed capacity is projected to grow from 416 GW in FY23 to an estimated 770-780 GW by FY30, with renewables (ex-hydro) adding 310-320 GW at an 18% CAGR to reach a 57% share of total installed capacity.

- Construction and data centre demand: Construction spending in the building segment is projected to grow ~1.4x from ₹12.5-13.5 lakh crore over FY20-24 to ₹18-19 lakh crore over FY25-29, while India’s data centre operational capacity is expected to nearly double from 1,150 MW in December 2024 to 2,000-2,100 MW by March 2027.

- Railway electrification and infrastructure push: Railway electrification is expected to generate incremental power demand of ~23 BUs annually between FY25 and FY29, while Union Budget FY26 allocated ₹11.21 lakh crore to the infrastructure sector, directly supporting specialised cable demand across metro rail, EV charging, and Smart City projects.

Peer Analysis

Competitors: Polycab India Ltd, RR Kabel Ltd, etc.

Among listed peers, KEI stands out for its consistent return profile and operational discipline. Its FY25 ROCE of 21.3% and virtually debt-free balance sheet (D/E of 0.04x) reflect a well-capitalised growth platform, while its operating margin of ~10-11% has held steady through commodity cycles. KEI has also delivered the sharpest working capital improvement in the peer set, with debtor days compressing from 118 in FY21 to 67 in FY25. Its FY25 fixed asset turnover of ~10x comfortably outpaces Polycab’s ~7x, underscoring capital efficiency.

Outlook

The outlook remains strong, with management guiding ~20% growth in FY26 supported by sustained demand across both retail (B2C) and institutional segments, alongside a gradual improvement in operating margins. Over the medium term, the company targets ~20% CAGR over the next 3–4 years, with EBITDA margins expected to reach ~11% by FY27, driven by operating leverage and a richer product mix. The wires segment continues to be a key growth driver, expected to sustain 22–23% growth, led by strong traction in the retail channel. Notably, the B2C segment’s contribution has increased to ~52% of revenues (vs ~46% earlier), reflecting a strategic shift toward higher-margin, non-cyclical retail business, which enhances margin stability, improves working capital cycles, and reduces dependence on lumpy institutional orders. Capacity additions at Chinchpada and Pathredi (~₹1,500–1,600 crore incremental capacity) further support near-term growth, while the institutional segment (~35% of revenues) remains critical given high entry barriers and strong demand from railways, real estate, and renewables. Backed by continued capex and execution strength, the company is targeting a scale-up to ~₹25,000 crore revenue over the next five years.

Valuations

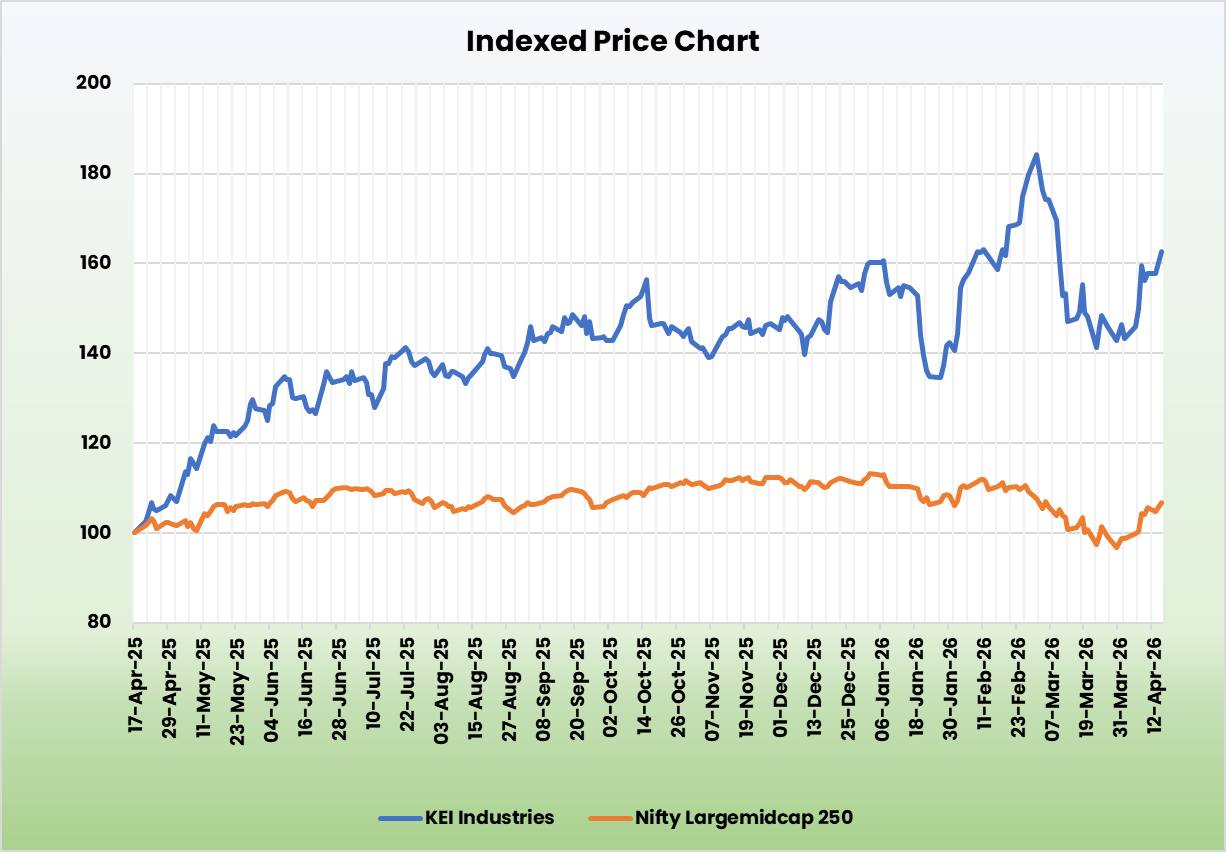

We believe Sanand-led capacity expansion positions the company for a multi-year growth upcycle, unlocking scale, improving product mix, and driving margin-accretive earnings growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.5,676, 45x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.