Mahindra & Mahindra Ltd. – Bold by Design

Mahindra & Mahindra Ltd., incorporated in 1945 and headquartered in Mumbai, is the flagship company of the Mahindra Group, a federated conglomerate with business presence across 100+ countries. The Company manufactures a diversified portfolio of SUVs, pickups, commercial vehicles, tractors, farm machinery, and electric three-wheelers across 24 plants in India, organised under three core portfolios – Automotive, Farm Equipment, and Services. The Company is India’s #1 SUV player by revenue market share (24.1% in Q3 FY26), #1 in LCV <3.5T (51.9%), the world’s largest tractor company by volume, and market leader in electric three-wheelers. Key brands include Thar, Scorpio, XUV 3XO, XUV 7XO, Bolero, BE 6, XEV 9e, XEV 9S, and Swaraj tractors, complemented by listed subsidiaries Tech Mahindra, Mahindra Finance, Mahindra Lifespaces, Mahindra Logistics, and Mahindra Holidays.

Products and Services

The company has its business spread across 3 main segments:

- Auto – SUVs and LCVs, 3-wheeler, motorcycles, trucks and buses.

- Farm – Tractors and agri services, farm machinery and genset manufacturing.

- Services – Financial, hospitality, logistics, renewable energy, technology, real estate, auto components, auto recycling, pre-owned cars, aerospace and defence.

Subsidiaries: As of FY25, the Mahindra Group comprises 122 subsidiaries, 30 associate companies, and 22 joint ventures.

Investment Rationale

- Structural industry tailwind & M&M’s pole position in the UV/EV space – India’s PV industry closed FY26 at a record ~4.7 million units, up 8.4% YoY, surpassing the previous peak of 4.34 million units, with the more critical structural signal being that SUVs now command ~67% of the PV market – up from 51% in FY23 and just 25% a decade ago. Within this landscape, M&M has not merely participated but has actively gained disproportionate share, overtaking its competitor to become the 2nd largest PV manufacturer in FY26, with revenue market share expanding from 21% in Q3FY24 to 24.1% in Q3FY26, and SUV volumes scaling from 118,900 units in Q3FY24 to 178,900 units in Q3FY26 a near 50% absolute volume jump in just two years. On EVs, where the industry is at an inflection point, the EV PV penetration jumped from 2.8% to 4.9% in a single year with volumes up over 85% YoY to ~2.29 lakh units. M&M is one of the very few incumbents with a credible, multi-model EV portfolio already in market; the BE 6, XEV 9E and XEV 9S are live, the XUV 3XO EV was launched in January 2026, and the 9S and 7XO together recorded 93,689 bookings as of January 2026, with 80% of EV buyers being new-to-Mahindra customers, meaning EV volumes are additive, not cannibalistic. With GST 2.0 having structurally improved affordability, replacement cycles resuming, and M&M’s pricing architecture allowing the 9S EV to compete on-road at near-parity with the 7XO ICE thereby eliminating the price penalty that has historically suppressed EV adoption. The company is simultaneously leveraging both the ICE SUV supercycle and the EV inflection, a combination that we believe is difficult for any competitor to replicate at this scale and speed.

- Broad-Based Financial Outperformance Underpinned by a Multi-Year Capacity & Earnings Growth Runway – Q3FY26 operating PAT grew 66% YoY, consolidated topline crossed ₹50,000 crores for the first time ever, and YTD profit growth is tracking ~38%, ahead of management’s own internal targets set at the start of the year. Auto standalone EBIT margins expanded from 8.5% in Q3FY24 to 10.4% in Q3FY26 (ex-contract manufacturing and ex-eSUV), with SUV volumes up 26%, LCV volumes up 20% YoY to 81,000 units, and Truck & Bus volumes up 36% YoY – all three sub-segments growing simultaneously. Farm delivered 23% volume growth with margins up 240 bps and Farm Machinery revenue surging 45%, now consistently above ₹100 crores/month. The capacity investment roadmap gives the volume growth story a clear and quantified multi-year runway: 5,000 – 6,000 ICE units and ~3,000 EV units added by July/August FY27; a further 7,000 – 8,000 ICE units from the new IQ platform at Chakan in CY27; and the Nagpur Greenfield with a ₹15,000 crore investment across 2,000 acres, plans to commence production in FY28 with an eventual capacity of over 5 lakh vehicles and 1 lakh tractors annually, making it M&M’s single largest integrated manufacturing footprint.

- Q3FY26 – During the quarter, the company reported consolidated revenue of ₹52,100 crore, up 26% YoY. EBITDA improved by 23% to ₹10,160. Net profit stood at ₹4,455 crore, up 47% YoY.

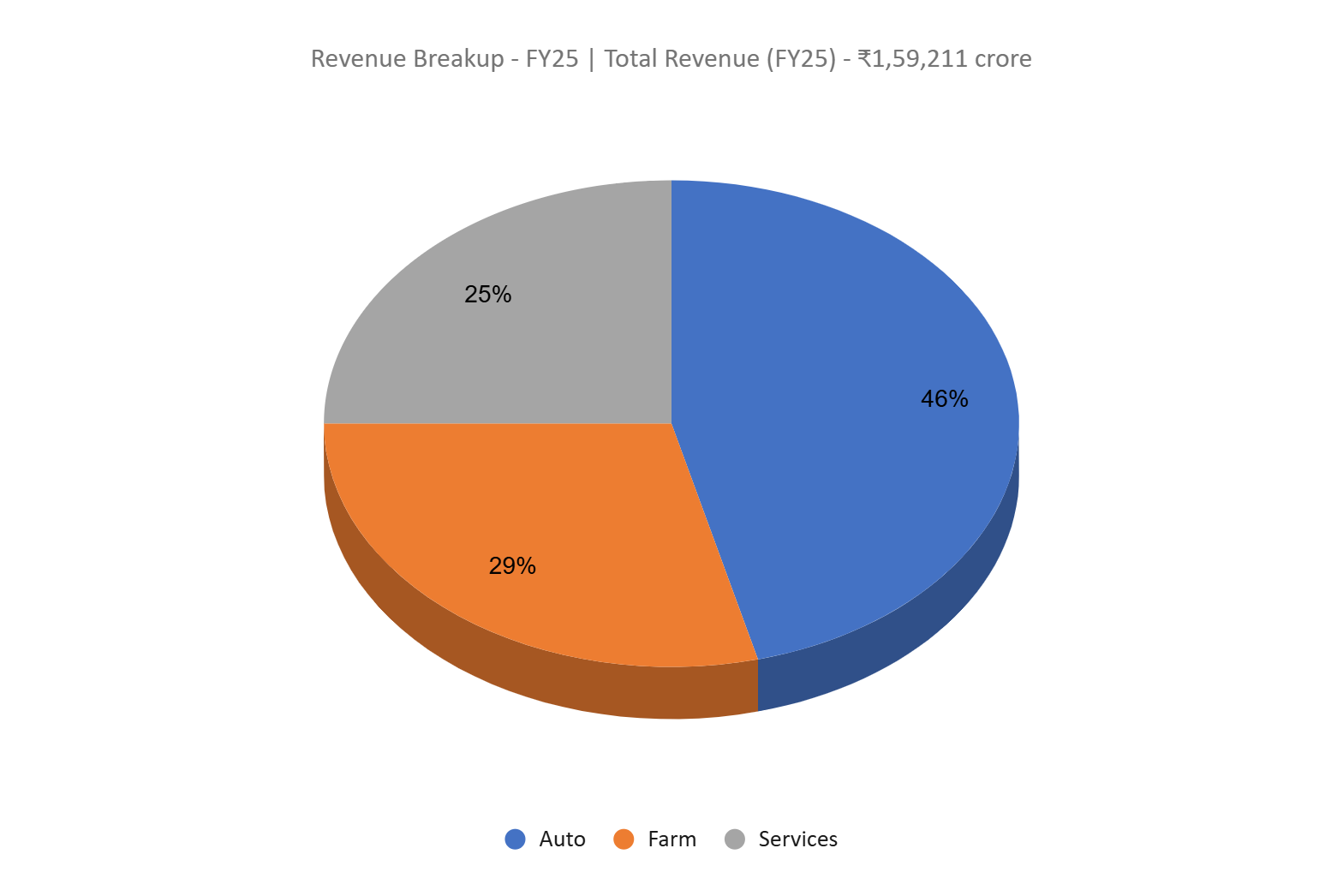

- FY25 – During FY25, the company reported consolidated revenue of ₹1,59,211 crore, representing a 14% YoY increase. EBITDA stood at ₹30,518 crore, up 23% YoY, and net profit was recorded at ₹14,073 crore, posting a growth of 15% YoY.

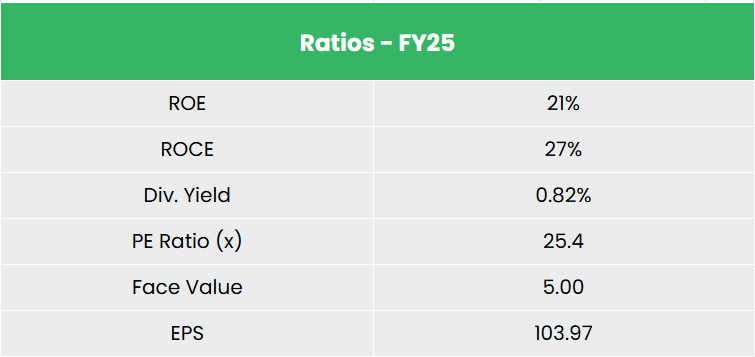

- Financial Performance – The 3-year revenue and net profit CAGR stands at 21% and 27% respectively between FY23-25. The company has a debt-to-equity ratio of 1.5x and the 3-year average ROE and ROCE are around 18% and 13% for FY23-25 period.

Industry

The Indian automobile industry contributes approximately 6% to India’s GDP, employs over 30 million people directly and indirectly, and is the third-largest automobile market globally. Total vehicle sales reached 2.56 crore units in FY25, growing 7% over FY24. The industry spans four segments – two-wheelers, three-wheelers, passenger vehicles, and commercial vehicles – with passenger vehicles accounting for 15.60% of domestic volumes in FY26 (April–September 2025), translating to over 20.51 lakh units sold in the first half. On the commercial vehicle side, total sales in FY26 (April–September 2025) stood at 4,63,502 units, underpinned by infrastructure-driven freight demand. The sector attracted equity FDI of ₹3,48,752 crore (US$ 39.3 billion) between April 2000 and June 2025, and the overall industry is projected to reach US$ 300 billion by 2026.

Growth Drivers

- Structural demand in PVs and SUVs – Rising incomes, a young population, and improving credit availability are driving sustained demand in passenger vehicles, particularly utility vehicles and SUVs.

- Infrastructure-led CV demand – India’s ongoing infrastructure build-out continues to support freight movement and commercial vehicle offtake across LCV and M&HCV sub-segments.

- Policy support and EV transition – The PLI scheme (₹25,938 crore outlay), PM E-DRIVE scheme (₹10,900 crore), and FAME incentives are accelerating EV adoption and rewarding localised manufacturing.

- Export-led scale-up – Automobile exports rose 19% to over 5.3 million units in FY25, with India increasingly positioned as a global manufacturing and export hub.

Peer Analysis

Competitors – Hyundai Motor India Ltd, Maruti Suzuki India Ltd, etc.

Compared to peers, M&M stands out for its valuation discount, with a 12x EV/EBITDA, a material discount to Hyundai (14x) and Maruti Suzuki (16x), despite demonstrating a strong return profile. The consolidated return profile is dragged down due to its large asset base of ₹2,92,930 crore as of H1FY26, which is significantly higher than peers, due to the consolidation of M&M finance’s loan book. On standalone terms, the company posts a strong ROE of 19%, with the automotive segment boasting a 41% return on capital employed. Notably, the company has consistently demonstrated superior DPO (Days payable outstanding) in the range of ~110-150, as opposed to the peer set (~50-70), undermining its buyer power.

Outlook

M&M’s investment case is anchored by a well-sequenced, three-phase capacity expansion plan that converts near-term momentum into a multi-year earnings growth story. By August 2026, ICE capacity additions of 5,000 – 6,000 units/month and EV scale-up to 7,000 – 8,000 units/month across three live models directly support the FY27 target of 80,000+ EV units annually. The CY27 Chakan facility adds another 7,000 – 8,000 units/month for the next-generation NU_IQ platform, sustaining SUV volume growth beyond existing product cycles. The transformative leg is the Nagpur Greenfield – a ₹15,000 crore investment commencing in FY28 targeting 5 lakh vehicles and 1 lakh tractors annually, making it M&M’s largest integrated manufacturing footprint and structurally positioning the company to sustain double-digit volume growth well into the next decade. With the product pipeline executing on plan 7XO launched, two more ICE SUV refreshes and two LCV launch still to come in CY26 we believe the company is well positioned to sustain its growth momentum.

Valuations

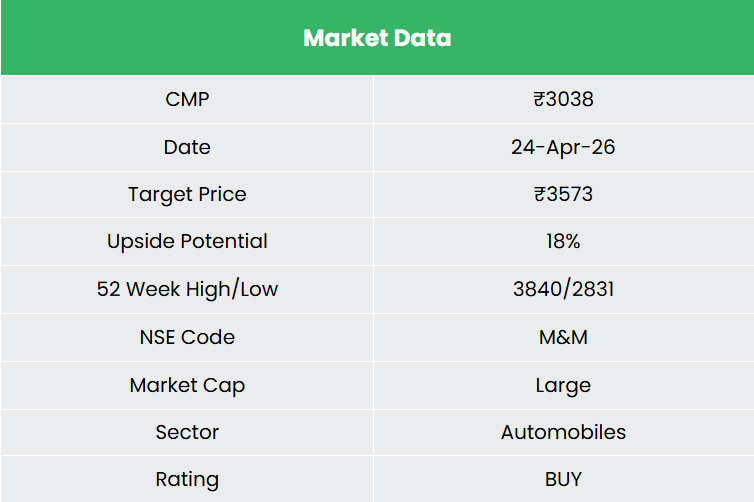

M&M’s auto demand outlook remains robust, underpinned by strong market acceptance of recent launches and a well-stocked product pipeline that provides clear volume visibility over our forecast period. We recommend a BUY rating in the stock with the target price (TP) of ₹3,573, 28x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.