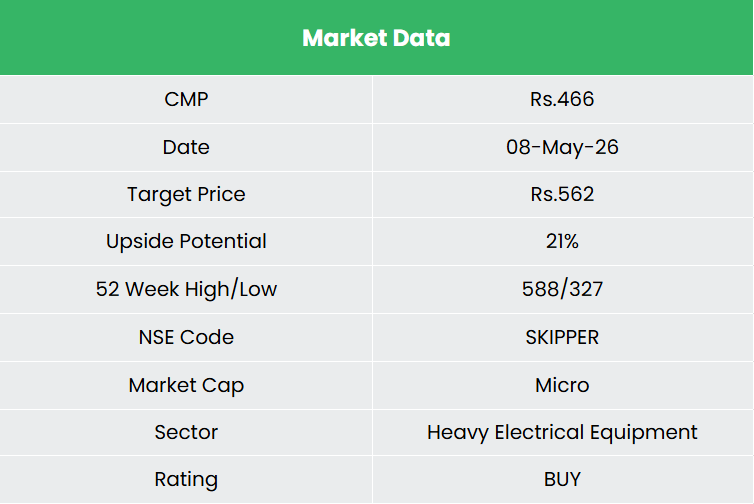

Skipper Ltd. – Leader in T&D Infrastructure

Established in 1981 and headquartered in Kolkata, Skipper Ltd. is a well-established manufacturer of Transmission and Distribution (T&D) structures (Towers and Poles), with over four decades of operating heritage. The company is also one of India’s fastest-growing players in the polymer pipes and fittings segment and a trusted partner for executing critical high-voltage transmission EPC projects. It is the largest manufacturer of integrated T&D structures in India and ranks among the top 5 transmission tower manufacturers globally. With 4 manufacturing facilities across Uluberia, Junglepore, BCTL (Howrah) and Guwahati, the company has a combined annual capacity of 300,000 MTPA for engineering products and 62,000 MTPA for polymer pipes and fittings. It currently serves customers across more than 65 countries worldwide.

Products and Services

The company’s offerings can be classified across 3 segments:

- Engineering – Production of T&D structures such as power transmission structures, railway structures, power distribution poles, MS and high tensile angles, monopoles, test station, telecom towers, solar structures, wind towers, fasteners and tower accessories.

- Infrastructure – Tower, telecom and water EPS, coating solutions, etc.

- Polymer – PVC pipes and fittings, HDPE pipes, bath accessories, tanks, borewell pipes and fittings, CPVC solvent cement, etc.

Subsidiaries: As of FY25, the company has 1 joint venture and no other subsidiary/associate company.

Investment Rationale

- Record Order Book & Unmatched Revenue Visibility – Skipper’s closing order book as of March 2026 stands at an all-time high of ₹85,019 Mn, backed by the highest-ever annual order inflow of ₹56,780 Mn (+6% YoY) – and critically, this isn’t just volume, it’s quality. The company has broken into the North American market with its largest-ever export order with a top-tier utility, secured the prestigious 800 KV Khavda HVDC project alongside multiple 765 KV/400 KV wins domestically, and is currently executing approximately 5,000 circuit kilometres of EHV & HVDC transmission line work. With 77% of the order book concentrated in domestic T&D – precisely where India’s grid modernisation, renewable integration, and HVDC buildout are driving the most capital deployment – and the remaining split across exports (10%) and non-T&D segments like telecom, railways, and solar (13%), the portfolio is aligned to where the structural opportunity is largest while retaining diversification as a buffer. With a bidding pipeline at an all-time high of over ₹33 Bn, PGCIL’s increased capex guidance for FY27, and Skipper commanding ~50% of India’s transmission capex spend as a preferred supplier across 25 active projects, the order book provides a revenue runway that is both quantifiable and underpinned by policy-backed capital allocation.

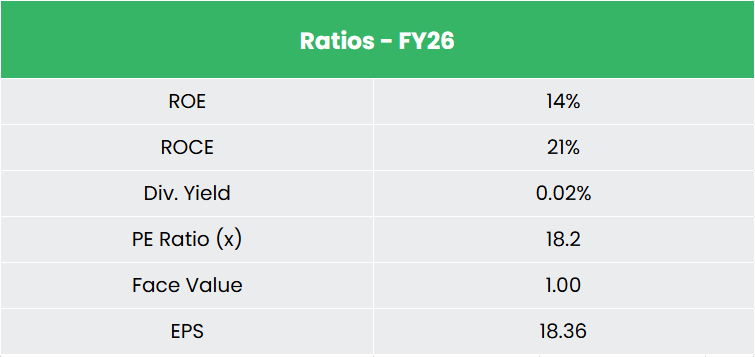

- Capacity, Geography & Financial Profile Inflecting Together – The company’s capacity utilisation has been running above 85 – 90%, and the company is expanding from 375,000 MTPA to 450,000 MTPA by June 2026 with the new 75,000-tonne facility already in commercial production – meaning incremental revenue can flow through without proportionate cost increases, directly expanding margins. On the global front, the company has completed plant audits with new potential customers from North America, Middle East, LATAM, Australia, and Europe, and has formally incorporated a subsidiary in Brazil (Skipper LATAM LTDA), signalling a structured, not opportunistic, export push. Financially, ROE has improved 180 bps YoY to 14.1%, finance cost ratio has declined to 3.3%, cash profit surged 58% QoQ to ₹971 Mn, and the company has entered the Substation EPC segment to complement its transmission line business – adding a higher-margin adjacency. The key risk to watch is debtor days going up, which has nudged working capital despite improvements elsewhere; if cash conversion normalises as management guides, the return ratios and free cash flow profile could re-rate meaningfully from current levels.

- Q4FY6 – During the quarter, the company generated its highest-ever quarterly revenue of ₹1,667 Cr, an increase of 29% compared to ₹1,288 Cr of Q4FY25. Operating profit increased from ₹124 Cr in Q4FY25 to ₹173 Cr in Q4FY26, a growth of 40%. The company reported consolidated net profit of ₹78 Cr, an increase of 63% YoY compared to ₹48 Cr in the corresponding period of the previous year.

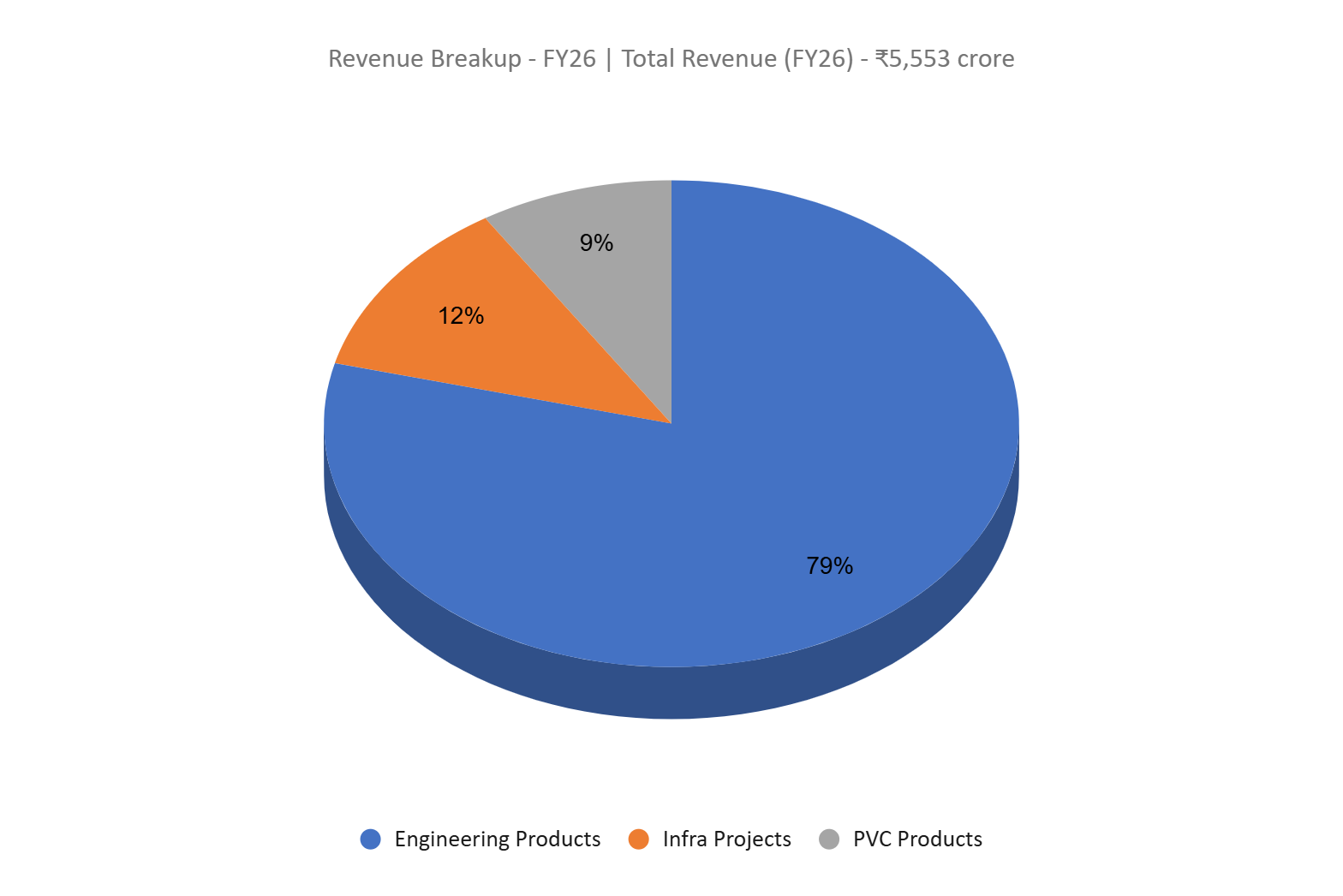

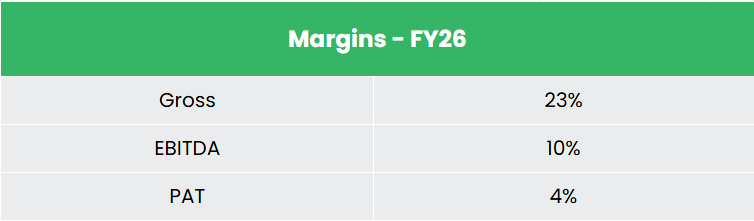

- FY26 – During the FY, the company generated revenue of ₹5,553 Cr, an increase of 20% compared to FY25 revenue. Operating profit stood at ₹573 Cr, up by 27% YoY, with EBITDA margin expanding ~50 bps to 10.3%. The company reported consolidated net profit of ₹213 Cr, an increase of 43% YoY. Growth was led by the Engineering segment, where revenue rose 24% YoY to ₹4,359 Cr and segment results rose 35% YoY to ₹517 Cr; the Polymer segment grew 17% to ₹507 Cr (crossing the ₹500 Cr mark for the first time), while Infrastructure Projects revenue was largely flat at ₹687 Cr.

- Financial Performance – The 3-year revenue and net profit CAGR stands at 41% and 88% respectively between FY24-26. The 3-year average ROE and ROCE are around 14% and 23%. The company has a debt-to-equity ratio of 0.64.

Industry

India’s power sector is at an inflection point, supported by sustained capital investment and the country’s energy transition agenda. India is the world’s third-largest electricity producer and consumer, with all-time peak power demand of 250 GW met during FY25. To support projected peak demand of 458 GW by 2032, the National Electricity Plan (2023 – 32) outlines investments of ₹9.15 Lakh Crore for grid expansion and renewable integration, and the country’s transmission network is targeted to expand from to 6.48 lakh ckm by 2032, with transformation capacity scaling from to 2,342 GVA.

Growth Drivers

- Government initiatives such as the National Electricity Plan, PM Gati Shakti National Master Plan, Green Energy Corridor, NIP and the PLI Scheme are catalysing transmission capex, with PGCIL alone driving the bulk of high-voltage line additions.

- Integration of renewable energy is a structural driver -India targets 500 GW of renewable capacity by 2030 (vs. 220.1 GW as of March 2025), necessitating new evacuation and inter-regional transmission lines (interregional capacity to rise from 119 GW to 168 GW by 2032), with 765 kV transmission lines expected to grow at a 13% CAGR till FY32.

- Rising electricity demand from accelerated urbanisation, low per-capita consumption (1,538 kWh vs. global average of ~3,700 kWh), grid digitalisation (HVDC, smart grids, digital substations), and the China+1 sourcing shift in international markets are expected to serve as long-duration growth catalysts for the T&D industry.

Peer Analysis

Competitors: Transrail Lighting Ltd, Bajel Projects Ltd, etc.

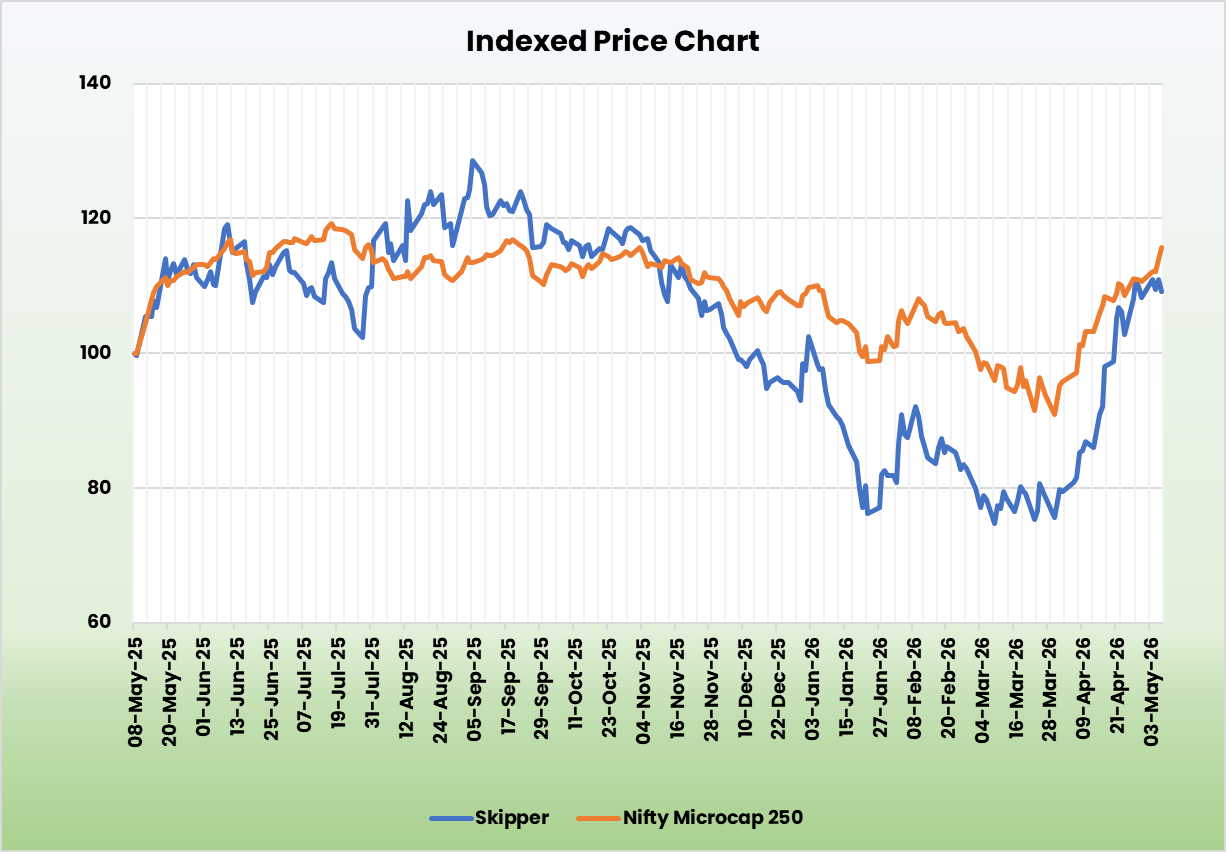

Among domestic listed peers in the T&D manufacturing and EPC space, Skipper stands out for its valuation discount (~11x EV/EBITDA as compared to the industry median of ~22) despite its strong return profile – underpinned by deeper backward integration, a globally diversified revenue base across 65+ countries, and a manufacturing-led business model that affords stronger operating leverage as scale increases.

Outlook

Skipper enters FY27 from a position of genuine operational strength – highest-ever revenue and profits, a 15% topline and 30% bottom line growth in FY26, and an order book that provides clear revenue underpinning for the near term. The return profile is improving in the right direction, with ROE expanding 180 bps to 14.1% and ROCE holding firm at 21.0%, signalling that growth is not coming at the cost of capital efficiency. The ₹250 crore capex guidance for FY27, directed at taking capacity to 450,000 MTPA, is measured rather than aggressive – and with utilisation already running above 85%, incremental volumes have a ready home without the risk of stranded capacity. The long-term aspirational EBITDA margin guidance of 12% is worth watching closely; the company is currently below that threshold, and the path there – through operating leverage, better contract quality, and export mix improvement being the key monitorables.

Valuations

The structural tailwinds in T&D, combined with a record bidding pipeline and a nascent but deliberate global expansion, suggest the demand environment remains supportive and we believe Skipper Ltd.to be at a steady position to be a beneficiary of this. We recommend a BUY rating in the stock with the target price (TP) of ₹562, 21x FY28E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.