Company Overview

Clean Max Enviro Energy Solutions Limited is a renewable energy solutions provider focused on supplying clean power to commercial and industrial (C&I) customers through long-term contracted arrangements and energy infrastructure services. The company operates through two segments: (i) Renewable Energy Power, under which it owns or co-owns solar, wind and hybrid assets and supplies electricity under long-term Power Purchase Agreements (PPAs) and Energy Attribute Purchase Agreements (EAPAs); and (ii) Renewable Energy Services, comprising turnkey development, engineering, procurement and construction (EPC), operation and maintenance (O&M), and capex solutions enabling customers to deploy captive renewable power projects.

As of October 31, 2025, the company had 2.80 GW of operational, owned and managed capacity and 3.17 GW of contracted capacity yet to be executed across onsite and offsite renewable energy projects. Its customer base comprises technology customers, including data centre and digital infrastructure operators, alongside conventional commercial and industrial enterprises.

Objects of the offer

The company is carrying out a book build issue of Equity Shares of face value of Rs. 1 each aggregating up to Rs. 3,100 crore, comprising a Fresh Issue aggregating up to Rs. 1,200 crore by the Company and an Offer for Sale aggregating up to Rs. 1,900 crore by the Selling Shareholders.

The proceeds of the fresh issue are to be utilized towards the following objects:

- Repayment and/or pre-payment, in part or full, of all or certain outstanding borrowings of the Company and/or certain of its Subsidiaries.

- General corporate purposes.

Investment Rationale

- Customer stickiness supported by group captive structure – CleanMax’s renewable power model is anchored in long-term contracted arrangements with customers, with operational and contracted capacity carrying a weighted average PPA tenure of approximately 22.73 years. A significant portion of projects are structured under the group captive framework, wherein customers acquire equity stakes (at least 26%) in project-specific subsidiaries (SPVs) and procure power as captive consumers, enabling exemption from certain grid surcharges, under which customers have invested ~Rs. 841 crore through equity participation across 97 subsidiaries as of September 30, 2025, aligning power consumption with ownership interests. Group captive projects contributed 52.48 % of Renewable Energy Power Sales revenue as of H1FY26, up from 48.26% in H1FY25. Customer equity participation materially increases switching costs, as termination would require exit from both long-term PPAs and invested project entities, supporting demand stability beyond contractual enforcement alone.

- Integrated platform enabling capital-efficient scalability – The company operates across asset ownership, EPC execution, O&M services and captive project development, allowing deployment under multiple contracting structures. As of October 31, 2025, CleanMax had 3.17 GW of contracted capacity yet to be executed, with 74.72% backed by firm PPAs/EAPAs and the balance governed by letters of intent across 29 customers, providing forward visibility into capacity addition.

The company also maintains a proactive development strategy by securing land, evacuation approvals and regulatory clearances well in advance of customer contracting to reduce execution timelines. The ability to switch between ownership and service-led deployment models allows growth without proportionate balance sheet expansion, partially mitigating the inherent capital intensity of renewable infrastructure.

- Visible growth pipeline and partnership-led expansion – CleanMax’s growth strategy is supported by a sizable execution pipeline, including 1.35 GW of capacity under construction scheduled for commissioning by July 31, 2026, alongside continued expansion of CTU-connected projects targeting technology customers. The company has entered strategic collaborations including a partnership with Toyota Tsusho Corporation to develop and operate approximately 300 MW of renewable energy projects by March 2028, and a co-investment arrangement with Apple South Asia Pte. Ltd., under which its subsidiary Clean Max Hyperion Power LLP is developing a portfolio of six rooftop solar projects aggregating 14.4 MW to supply renewable energy to Apple’s offices, retail stores and operations in India. The company has also undertaken international expansion through a joint venture in Bahrain with 10.90 MW of onsite solar capacity deployed as of October 31, 2025. Additionally, projects are being expanded across high-resource states such as Gujarat, Rajasthan and Karnataka to serve growing data centre clusters and industrial demand.

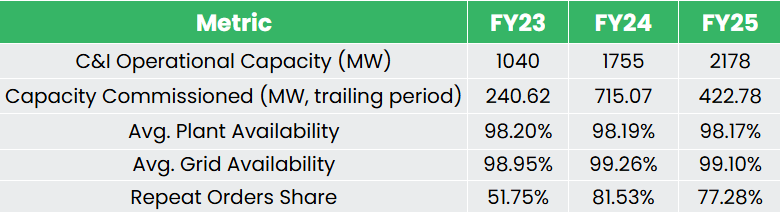

- Strong execution and asset reliability – CleanMax’s operational track record reflects consistent execution across commissioning, asset performance and customer expansion. The company has scaled its C&I operational capacity from 1,040 MW in FY23 to 2,178 MW in FY25, alongside commissioning 422.78 MW during the trailing twelve months ended FY25, indicating sustained execution momentum. Operational reliability remains strong, with portfolio-level plant availability maintained at approximately 98% and grid availability around 99%, supporting stable power delivery under long-term contractual arrangements. Additionally, repeat orders accounted for 77.28% of new contracted volumes in FY25, reflecting a meaningful contribution from existing customers to incremental capacity additions.

Key Risks

- Limited growth capital infusion – Majority of the IPO is an OFS, representing shareholder monetisation rather than growth capital infusion. A significant portion of the Fresh Issue proceeds is proposed to be utilised toward repayment or prepayment of borrowings, positioning the offering largely as a balance sheet deleveraging exercise. While debt reduction may improve leverage metrics, limited primary capital deployment toward capacity expansion implies that future growth will continue to depend on project-level financing, internal accruals and partnership-led capital deployment.

- Regulatory dependence – A substantial portion of projects operate under group captive and open-access structures that benefit from regulatory concessions and surcharge exemptions. Any adverse changes in state electricity policies, withdrawal of incentives, or tightening of open-access regulations could increase effective power tariffs for customers and reduce demand under these arrangements.

- Capital-intensive model and margin sensitivity – The renewable energy business requires significant upfront capital investment, resulting in elevated finance and depreciation expenses during asset ramp-up phases. In FY25, despite EBITDA of Rs. 1,015 crore, profit after tax stood at only Rs. 19.4 crore, reflecting the impact of interest and depreciation. As capacity scales, earnings remain sensitive to borrowing costs, refinancing conditions and asset amortisation timelines, which may constrain profitability despite operating growth.

- Execution risk – As of October 31, 2025, the company had 3.17 GW of contracted capacity yet to be executed, including 1.35 GW under construction, requiring timely completion across land acquisition, approvals and grid connectivity. Any delays in commissioning could defer revenue recognition and impact expected cash flows.

Outlook

CleanMax Enviro Energy Solutions has positioned itself as a differentiated renewable energy platform with a focus on C&I customers. The company benefits from long-term revenue visibility, complemented by a scalable services segment with a visible execution pipeline and operational strength. However, the business remains inherently capital intensive, with profitability currently moderated by elevated finance and depreciation costs. Growth execution is dependent on continued access to project financing, stable regulatory support for open-access and captive structures, and timely commissioning of a sizeable contracted pipeline. While operational performance and customer partnerships provide visibility, earnings growth will remain linked to balance sheet discipline and successful conversion of contracted projects into operating assets.

According to the RHP, the company’s listed peers are ACME Solar Holdings Ltd, NTPC Green Energy Ltd and Adani Green Energy ltd, among others. The industry peer group is trading at an average EV/EBITDA of 22.72x, the highest being 41.91x, and the lowest being 9.85x. At the upper price band, the listing market capitalization of CleanMax would be Rs. 12,325 crore, and the company is demanding an EV/EBITDA of ~16.63x, based on the post issue EV, and annualized H1FY26 EBITDA. When compared to its peers, the issue appears fairly valued. The valuation gap relative to larger renewable energy platforms reflects the company’s relatively smaller operating scale, and evolving profitability profile. Investors should view the company as a steady compounding renewable infrastructure play driven by capacity scale-up rather than near-term earnings acceleration. We assign a ‘Subscribe’ rating for long-term investors.

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.