Man Infraconstruction Ltd. – A key player in infrastructure development

Man Infraconstruction Ltd (MICL), established in 2002 and headquartered in Mumbai, is an integrated EPC (Engineering, Procurement & Construction) company renowned for its expertise in various construction segments. With a track record of delivering landmark projects across India, MICL is particularly recognized for its superior quality construction and timely project delivery in the real estate sector.

Product Portfolio of MICL

- Port infrastructure: Onshore container terminals, land reclamation, operational services.

- Commercial & Institutional Constructions: IT parks, office complexes, hotels, malls, schools, hospitals.

- Road constructions: Earthwork, paving, electrification, landscaping.

- Residential Constructions: High rise buildings, townships, luxury villas.

- Industrial Constructions: Factories, cold storages, warehouses, manufacturing units.

- Subsidiaries: 17 subsidiaries, 3 associate companies, and 1 joint venture as of FY23.

Growth Strategies of MICL

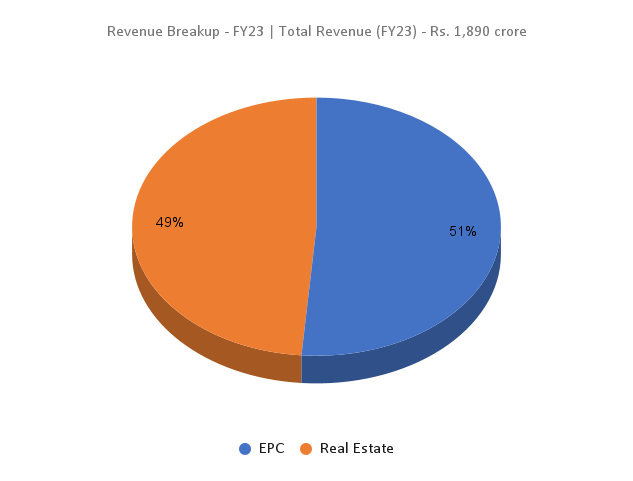

- Diversified business model encompasses Engineering, Procurement, and Construction (EPC) alongside Real Estate Development.

- EPC segment generates income from infrastructure projects like ports, institutional buildings, and residential projects.

- Potential for additional income through Project Management Consultancy (PMC) fees.

- Emphasis on an asset-light approach through subsidiaries, joint ventures, and associates.

- Upcoming projects include ultra-luxurious residential ventures in Mumbai and redevelopment projects.

- International expansion with investments in the US market, including projects in Fort Lauderdale and Miami.

Financial Highlights of MICL

Q3FY24 Performance

- Revenue: Rs.242 crore, reflecting a 47% decline compared to Q3FY23.

- Operating Profit: Recorded at Rs.103 crore, marking a 20% decrease from Q3FY23.

- Net Profit: Stood at Rs.87 crore, with a marginal 4% decline.

- Noteworthy Improvement: Operating profit margin increased to 43%, and net profit margin rose to 36%, up from 28% and 20% respectively in Q3FY23.

- Quarter-over-Quarter Growth: Compared to the previous quarter (Q2FY24), revenue increased by 13%, operating profit surged by 61%, and net profit improved by 34%.

Financial Performance (FY20-23)

- Compound Annual Growth Rate (CAGR): MICL has achieved a commendable revenue and Profit After Tax (PAT) CAGR of 24% and 31% respectively over the period from FY20 to FY23.

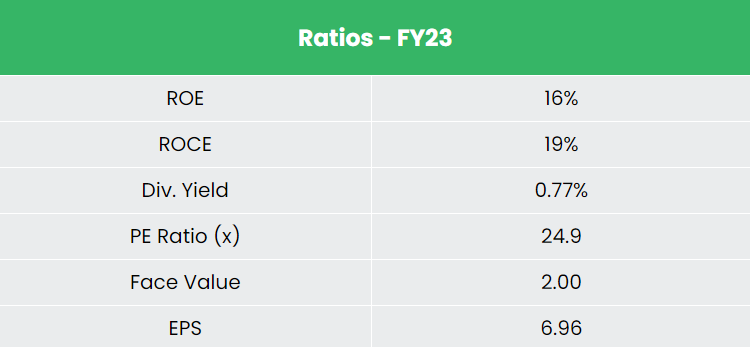

- Return on Equity (ROE) & Return on Capital Employed (ROCE): The average 5-year ROE and ROCE stand at around 14% and 18% respectively for the FY18-23 period.

- Strong Balance Sheet: MICL boasts a robust debt-to-equity ratio of 0.18, indicating a healthy financial position and efficient capital management.

Industry Outlook

- The infrastructure sector remains pivotal for India’s economic advancement, spearheading comprehensive development initiatives.

- Government focus on policy implementation ensures the time-bound creation of top-tier infrastructure, driving economic growth.

- The construction market is poised to expand significantly, expected to reach US$ 1.42 trillion by 2027.

- Urbanization trends indicate a burgeoning demand for housing, with an estimated 600 million urban dwellers by 2030.

- Infrastructure development acts as a catalyst, fostering growth in ancillary sectors like townships, housing, and construction projects.

- Robust growth is forecasted, with a projected CAGR of 17.26% during the 2022-2027 period, signaling ample opportunities for sectoral expansion.

Growth Drivers

- Government initiatives like the National Infrastructure Pipeline and Make in India.

- Budget allocation of Rs.10 lakh crore for infrastructure.

- 100% FDI in completed construction projects.

Competitive Advantage

Compared to competitors like Macrotech Developers Ltd, NCC Ltd etc, MICL has the following advantages:

- Superior undervalued stock with consistent sales growth.

- Effective utilization of capital compared to competitors.

Outlook

- Indian real estate sector expected to grow to $1 trillion by 2030, comprising 13% of India’s GDP by 2025.

- MICL poised for growth with a real estate sales visibility of Rs.12,000 crore from FY24 launches and upcoming projects.

- Niche in redevelopment and cluster projects promises better returns on capital.

- Track record of delivering projects ahead of schedule with superior quality and execution.

- Active addition of new projects with faster completion pace and ongoing project fund raise.

- Series of projects slated for launch next year, including Pali Hill, Kala Nagar, Marine Lines, Ghatkopar, Dahisar, and Goregaon.

- Holding a substantial EPC order book of Rs.1,047 crore, indicating a robust pipeline for future revenue.

Valuation

- Favorable economic fundamentals and positive consumer sentiments driving real estate sector growth.

- MICL’s healthy balance sheet and expanding order book indicate steady growth potential.

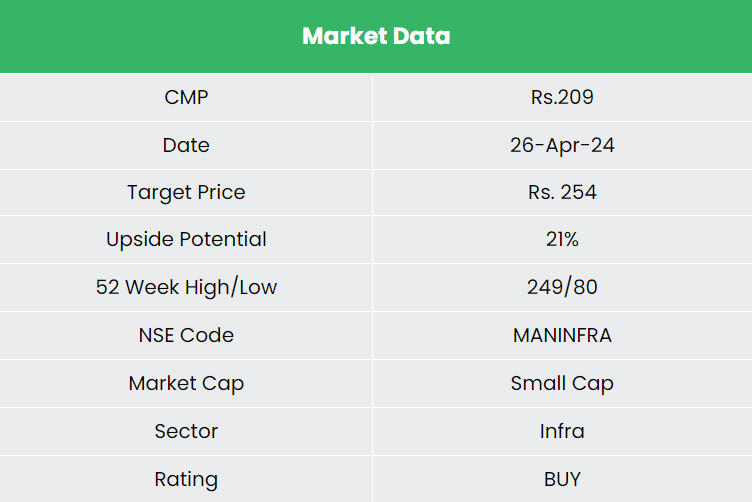

- BUY rating with a target price of Rs.254 30x FY25E EPS.

Risks

- Geographic concentration in Mumbai and MMR may lead to sales impact due to delays or inventory accumulation.

- A rise in input costs and regulatory changes could affect margins and cash flow.

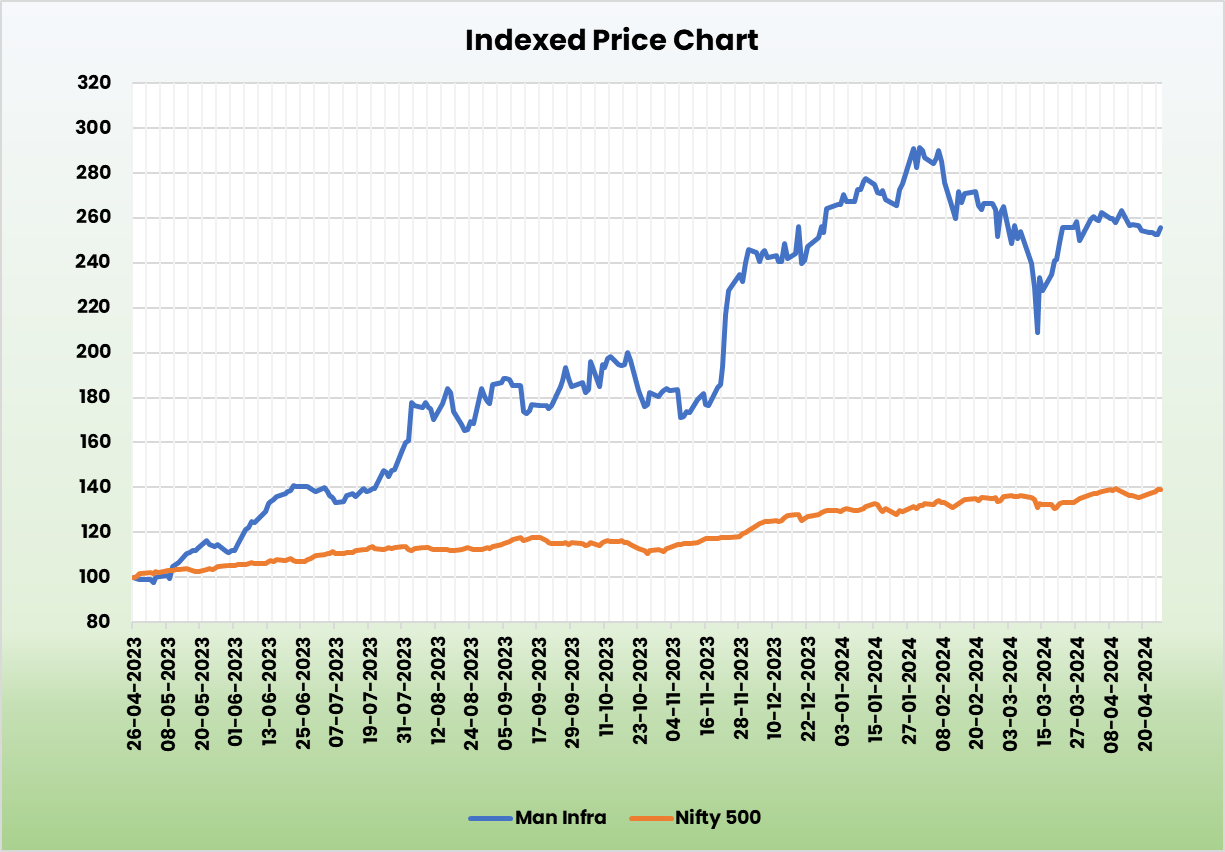

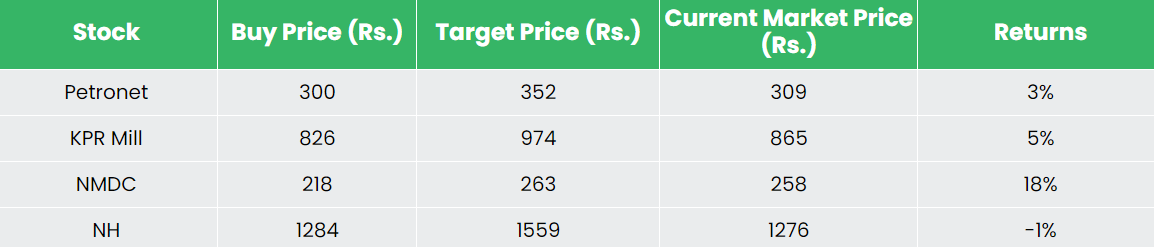

Recap of our previous recommendations (As on 26 Apr 2024)

[fbcomments]