National Aluminium Company Ltd – Asia’s largest bauxite-alumina-aluminium complex

Founded in 1981 and headquartered in Bhubaneswar, National Aluminium Company Ltd. (NALCO) is a “Navratna” company with a 51.28% ownership by the Indian Government. It is one of the country’s largest integrated bauxite, alumina, aluminium, power and coal complex. The company has captive bauxite mines (capacity of 6.8 MTPA) in Panchpatmali and alumina refinery (capacity of 2.1 MTPA) at Damanjodi, in the District of Koraput in Odisha and aluminium smelter (0.46 MTPA) & captive power plant (1,200 MW) at Angul. Additionally, NALCO has coal reserves and wind power plants, with respective generation capacities of 4 MTPA and 198 MW to support its power needs.

Products and Services

The company produces and sells alumina and aluminium products (ingots, billets, wire rods and roll products) in both domestic and international markets.

Subsidiaries: As of FY24, the company has 4 joint ventures and no subsidiaries/associate companies.

Investment Rationale

- Major expansion projects – The company has outlined expansion plans across all its operational segments. It aims to commission new Pottangi bauxite mines with a capacity of 3.5 MTPA in FY26. Additionally, a new conveyor belt is being installed from the existing Panchpatmali bauxite mines to the refinery. To accommodate the higher mining throughput, the company is setting up new 5th stream alumina refinery (to be commissioned in FY26) with a capacity of 1 MTPA. Over the next 3-5 years, the company is expanding its aluminium smelter capacity by 0.5 MTPA and its captive power capacity (for which it has signed an MoU with NTPC). The combined capex for these two projects is Rs.30,000 crore. To further optimise its operations, the company has decided to appoint a Mine Developer and Operator (MDO). Simultaneously, the company is also developing a 25.5 MW wind power plant in Tamil Nadu and developing the Utkal-D & E coal blocks with a combined peak production capacity of 4 MTPA.

- The KABIL JV – The company, holding a 40% stake, has formed a joint venture called KABIL with Hindustan Copper Ltd (30% stake) and Mineral Exploration and Consultancy Ltd. The joint venture aims to identify, acquire, develop, process, and commercially utilize strategic minerals in international locations for supply to India, thereby supporting the Government of India’s “Make in India” initiative. KABIL’s main focus is sourcing key battery minerals such as Lithium and Cobalt. In FY24, the company signed an exploration and development agreement with CAMYEN, Argentina, for five lithium mines. Additionally, KABIL, in partnership with the Critical Minerals Office (CMO) of Australia, has engaged a Commercial Advisor to assist with the shortlisting and due diligence of Lithium and Cobalt mineral assets in Australia.

- Q3FY25 – During Q3FY25, the company generated revenue of Rs.4,662 crore, an increase of 39% as compared to the Rs.3,348 crore of Q3FY24. EBITDA increased by 206% from Rs.756 crore of Q3FY24 to Rs.2,311 crore of the current quarter. Net profit increased from Rs.471 crore of Q3FY24 to Rs.1,566 crore of Q3FY25, a growth of 232% YoY. The improved financial performance is attributed to better realization and sales of alumina, use of captive coal and reduction in the cost of raw materials.

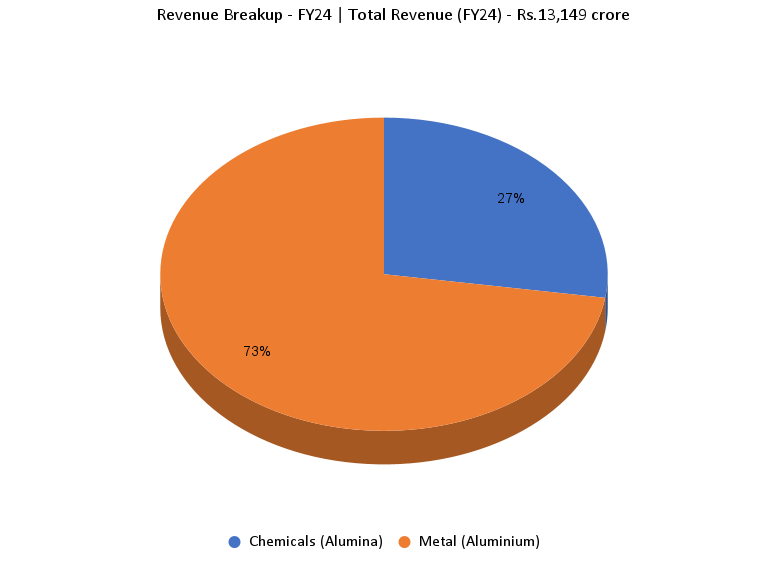

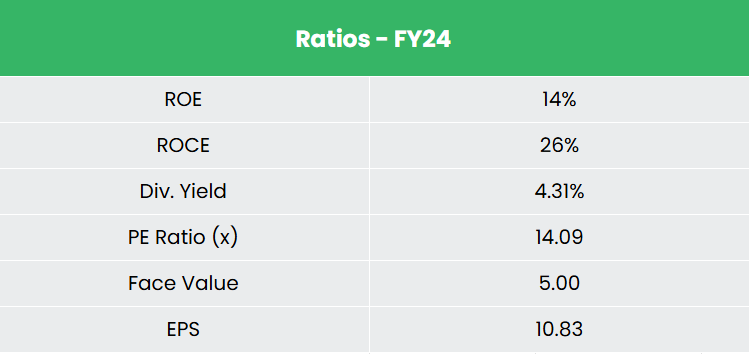

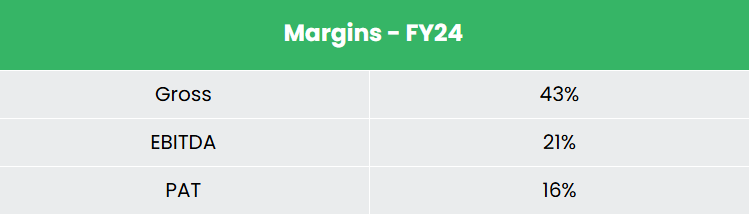

- FY24 – The company generated revenue of Rs.13,149 crore, a decline of 8% compared to FY23 revenue. Operating profit is at Rs.2,801 crore, up by 20% YoY. The company posted net profit of Rs.1,988 crore, an increase of 39% YoY. EBITDA margin improved from 16% to 21% and net profit margin increased from 11% to 15%.

- Financial Performance – The company has generated revenue and net profit CAGR of 14% and 9% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 16% and 22% each for FY21-24 period. The company has a debt-to-equity ratio of 0.01.

Industry

The metals and mining sector is crucial to a nation’s development, supplying essential raw materials for key industries. The growth of a country’s industrial sector is closely linked to the expansion of its mining industry. This sector has the potential to greatly influence GDP growth, foreign exchange earnings, and provide a competitive advantage to industries such as construction, infrastructure, automotive, and energy by securing vital raw materials at affordable prices. India’s strategic location, which facilitates exports, along with its cost-effective production and conversion processes, has helped it become the world’s fourth-largest aluminium producer.

Growth Drivers

- 100% FDI through automatic route in the mining sector.

- The vast resources of numerous metallic and non-metallic minerals is expected to serve as a foundation for the expansion and advancement of the nation’s mining industry.

- Indian government’s initiatives and schemes such as Gati Shakti Master Plan, Make in India, Pradhan Mantri Awas Yojna – Housing for all, Urban Infrastructure development scheme for small and medium towns is expected to foster the growth of Metals and Mining sector in India in the next few years.

Peer Analysis

Competitor: Hindalco Industries Ltd.

Efficient capital allocation and cost optimisation strategies has resulted in the company generating better returns and profit margins (TTM operating profit margin of 39% vs 13% of Hindalco) compared to its competitor.

Outlook

Currently NALCO is one of the lowest cost bauxite and alumina producers across the world. Being a zero-debt company provides the company with better leverage opportunities to raise funds for its future expansion plans. We believe the company’s growth potential is driven by three key factors: 1) integrated operations and strategic location, 2) raw material securitization, 3) expanded refinery capacity and smelter capacity addition to give scope for extrusion and other value-added products. Additionally, the company is actively participating in mining auctions. Looking ahead, NALCO plans to enter the production of value-added aluminium products, which offer higher margin potential and increased profitability.

Valuation

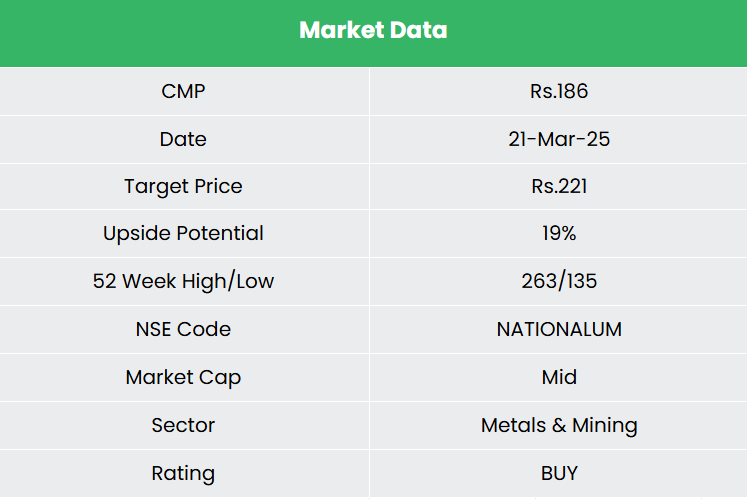

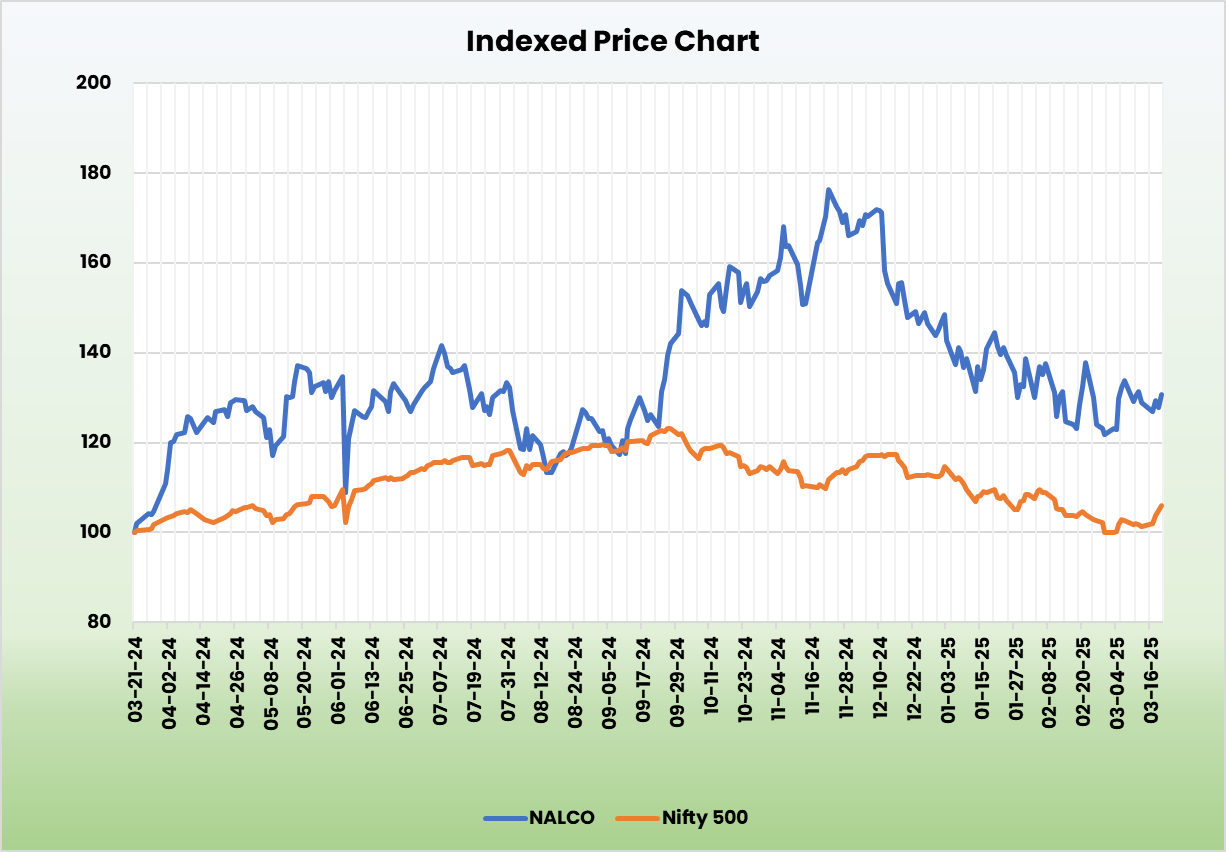

The company’s all-round expansion plans are expected to payoff and accelerate its growth momentum. We recommend a BUY rating in the stock with the target price (TP) of Rs.221, 12x FY26E EPS.

Risk

- Execution delays – Any unexpected delays in the completion of expansion projects might impact the company operations.

- Forex Risk -The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

Recap of our previous recommendations (As on 21 March 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.