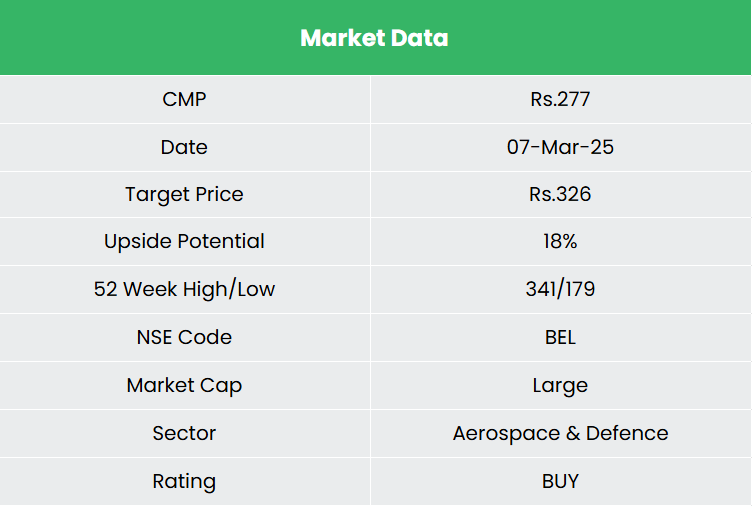

Bharat Electronics Ltd – Empowering the Nation’s Defence Forces

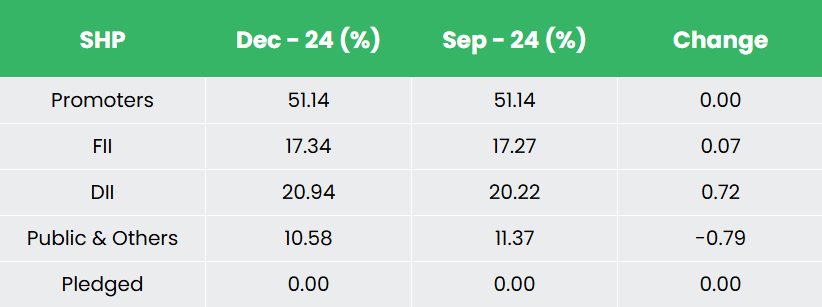

Established in 1954, Bharat Electronics Ltd. (BEL) is a Navratna Public Sector Undertaking primarily engaged in developing electronics technology solutions for the defence and civilian segments. It holds a prominent position in the Indian Defence segment with ongoing expansion into international defence and civil markets. Headquartered in Bengaluru, it has 9 manufacturing units, 2 research units and 29 strategic business units (SBU). The Government of India (GoI) remains the largest shareholder of BEL with the shareholding of 51.14% as on 31 December 2024.

Products and Services

The company majorly functions in defence and non-defence business segments. Defence products comprise of navigation systems, communication products, land-based radars, naval systems, electronic warfare systems, avionics, electro optics, weapon systems, shelters and masts, arms and ammunition, seekers and missiles, etc. Non-defence includes products and services for cyber security, e-mobility, railways/metro/airport solutions, e-governance systems, solar cells/power plants, homeland security, civilian radars etc.

Subsidiaries: As of FY24, the company has 2 subsidiaries and 2 associate companies.

Investment Rationale

- Growth strategies – The company has incorporated 5 new strategic business units (SBUs) during H1FY25. First one is EW (Electronic Warfare) land systems at Hyderabad with a Rs.1,500 crore turnover expected in FY25. Other SBUs are for RF and IR seekers, arms and ammunition, network and cybersecurity and unmanned systems which the company anticipates contributing Rs.1,000+ crore revenue from next 2-3 years. The company is setting 5 new factories for various operations that includes advanced night vision, EW systems for land, weapon system and integration, fuse complex and explosives, airborne equipment and missiles. The company has also signed an MoU with Safran Electronics & Defence, France to create a Joint Venture for manufacturing, customising, sales and maintenance of HAMMER, a precision guided air-to-ground weapon, in India.

- Expanding order book – The company has secured order worth Rs.1,220 crore from Indian Coast Guard for supplying software defined radios. It has also won another contract at Rs.610 crore to supply Electro-Optic Fire Control System (EOFCS) to the Indian Navy. It has won additional orders worth Rs.577 crore for airborne electronic warfare products, an advanced composite communication system for submarines, Doppler weather radar, train communication systems, radar upgrades, spares, and services, taking the order book to ~Rs.14,000 crore won in FY25 as of current date. During FY26, the company is expecting major orders including QRSAM (valued at Rs.25,000 crore – Rs.30,000 crore), NGC (valued at Rs.14,000 to Rs.15,000 crore) and additional 5/6 orders in the range of Rs.2,000 crore to Rs.3,000 crore. Majority of these orders are to be executed within a time frame of 2-5 years.

- Q3FY25 – During the quarter, the company earned revenue of Rs.5,771 crore, an increase of 39% compared to the Rs.4,162 crore of Q3FY24. EBITDA improved by 56% from Rs.1,072 crore of Q3FY24 to Rs.1,669 crore of the current quarter. The company reported net profit of Rs.1,312 crore, a growth of 53% compared to the corresponding period in the previous year.

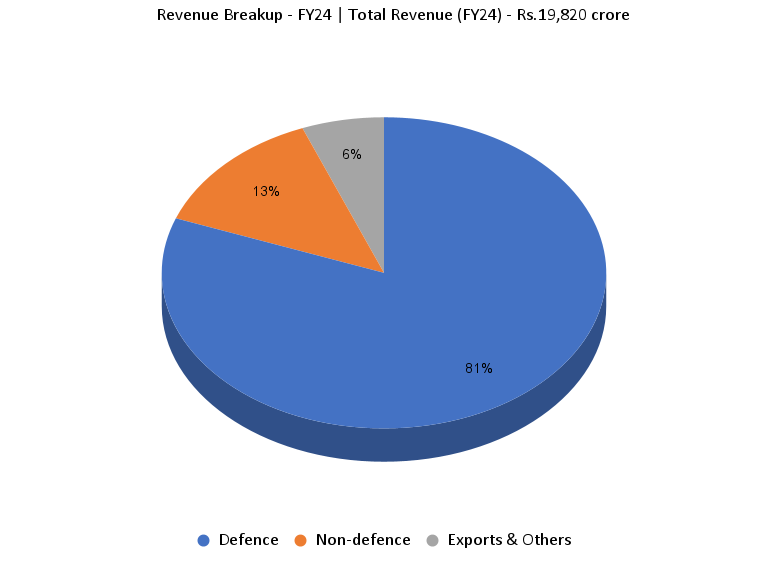

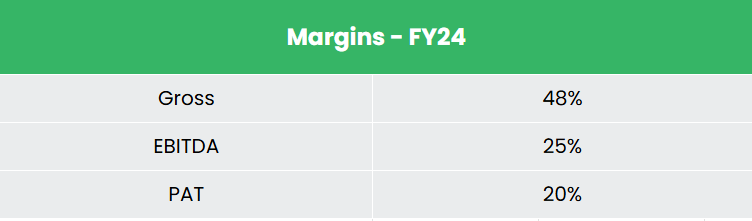

- FY24 – The company generated revenue of Rs.19,820 crore during FY24, an increase of 14% compared to the FY23 revenue. EBITDA was at Rs.4,998 crore, up by 23% YoY. An improved product mix has enabled the company to earn higher profits. The company reported net profit of Rs.4,020 crore, an increase of 34% YoY.

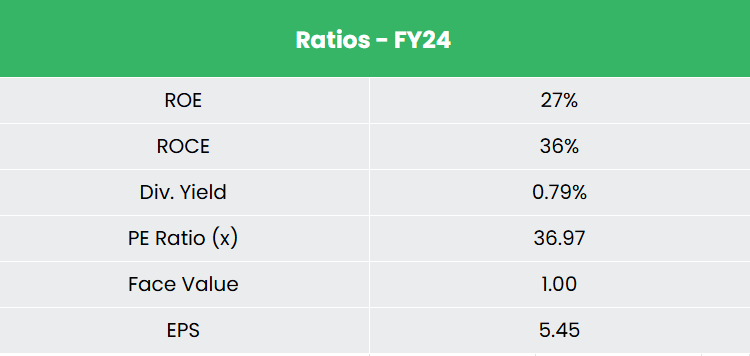

- Financial Performance – The company has generated revenue and net profit CAGR of 13% and 24% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 23% and 31% for FY21-24 period. The company has strong balance sheet without any debt in its capital structure.

Industry

India is one of the strongest military forces in the world and the industry holds a place of strategic importance for the Indian government. The country’s defence manufacturing sector is rapidly expanding, fuelled by substantial government investment, growing exports, and policies that foster self-reliance and technological innovation. The government has prioritized the Defence and Aerospace sector as part of the ‘Aatmanirbhar Bharat’ (Self-Reliant India) initiative, with a strong focus on establishing indigenous manufacturing capabilities supported by a robust research and development ecosystem. To modernize its armed forces and reduce reliance on external defence procurement, the government has launched several initiatives to promote ‘Make in India’ activities through policy support. Furthermore, India has set an ambitious target of achieving US$ 6.02 billion (Rs. 50,000 crore) in annual defence exports by 2028-29.

Growth Drivers

- In 2025-26 the central government has allocated Rs.6,81,210 crore for the Ministry of Defence which is 6% higher than the previous year.

- Growing demand for defence manufacturing given the rising concerns of national security.

- Provision for 100% Foreign Direct Investment (FDI) through Government route and 74% through Automatic route into the defence sector.

Peer Analysis

Competitors: Hindustan Aeronautics Ltd, Bharat Dynamics Ltd, etc.

Compared to the above competitors, BEL has generated stable return ratios in line with the growth in the sales. This indicates the company’s ability to generate better profits for the capital invested.

Outlook

The company anticipates receiving an order inflow of Rs.25,000 crore in FY25 and between Rs.25,000 crore and Rs.50,000 crore in FY26. For FY25, it has set a revenue growth target of 15%, gross margin range of 42%-44% and EBITDA margin range of 23%-25%. In FY24, the company invested Rs.1,236 crore in R&D. The management is confident about securing significant orders from the Ministry of Defence (MoD). Additionally, the company plans to gradually increase its non-defence revenue share over the medium term, aiming to raise it from the current 8%-10% to 10%-15%, and eventually to 20%-25% in the long term. With a stronger product mix and as a leading player in defence, equipped with diverse technological competencies, a robust innovation strategy, a well-capitalized balance sheet, and a diversified product portfolio, we expect the company to successfully meet its targets.

Valuation

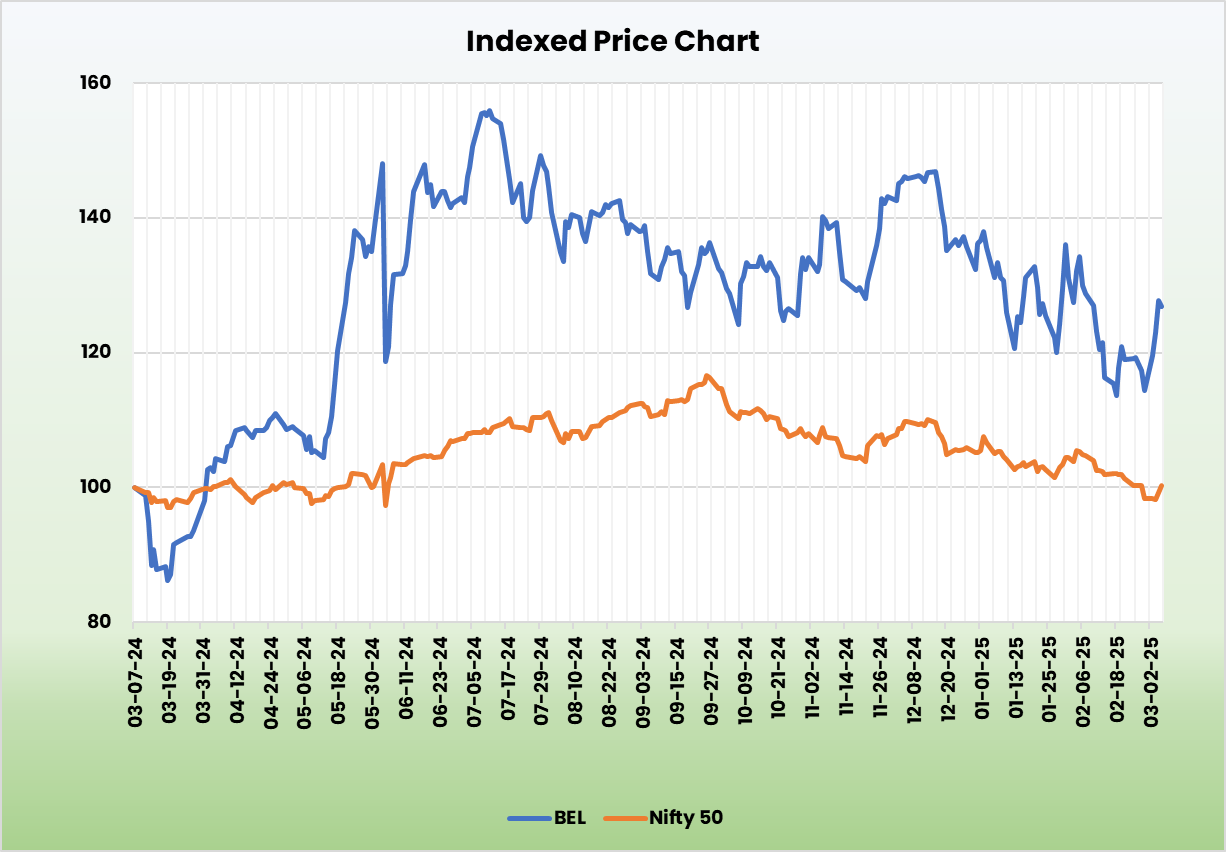

Given the robust financial profile, expanding order book and strong execution capabilities, we believe that BEL will further solidify its strategic position as a dominant supplier of electronic equipment to India defence forces. We recommend a BUY rating in the stock with the target price (TP) of Rs.326, 36x FY26E EPS.

Risk

- Client Concentration Risk – BEL is deriving more than 80% of its revenue from the Indian defence sector. Any major cut in the defence spending by the Government will significantly impact the order book and thereby revenue.

- Input cost variations – Potential delays in receiving input materials and components due to supply chain discontinuities, long lead times, and vendor defaults caused by increased raw material prices might impact operations.

Recap of our previous recommendations (As on 07 March 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.