Krishna Institute of Medical Sciences Ltd – Real Wealth is Good Health

Established in 1973 and headquartered in Secunderabad, Krishna Institute of Medical Sciences Ltd (KIMS) is one of the nation’s leading hospital networks that provides integrated, multi-disciplinary healthcare services, focusing on tertiary and quaternary care. It has strong presence in Telangana, Andhra Pradesh, Maharashtra, Kerala and Karnataka. The company’s flagship hospital in Secunderabad, with a 1,000-bed capacity, is one of the largest private hospitals in India. The company has a widespread network of 12 hospitals, 5,500+ beds and 2,300+ doctors.

Products and Services

KIMS provides multi-speciality care services across various divisions such as neurology, cardiology, pulmonology, ENT, ophthalmology, oncology, orthopaedics, paediatrics, diagnostics etc.

Subsidiaries: As of FY24, the company has 12 subsidiaries and 1 associate company.

Investment Rationale

- Expansion plans – The company is planning to launch three new projects in Thane and two in Bengaluru in Q2FY26. In Q3FY25, it commissioned a 200-bed multispecialty hospital in Guntur under an Operations & Management (O&M) model. As part of its geographic expansion, it is establishing three new facilities in Kerala. The first facility in Kannur has already been launched and achieved breakeven within three months. The second is being set up through an agreement with Valiyath Institute of Medical Sciences Hospital in Kannur, while the third facility in Thrissur is expected to become operational within 12–15 months. Additionally, the company plans to add 500 beds to its Kondapur facility, increasing the total capacity to 800 beds. It has also entered into O&M agreements with several hospitals across Guntur, Visakhapatnam, Hyderabad, and Maharashtra. Furthermore, the company has signed a Rs.700 crore agreement with Wipro GE Healthcare for the procurement of medical technologies and services.

- Pioneering innovative launches in the nation – The company prioritizes the integration of cutting-edge technologies into its operations. Setting a new standard in neuro care, it has introduced South Asia’s first MRI-guided focused ultrasound using the Hero 3T MRI—an innovation proven to alleviate tremor-dominant Parkinson’s disease and essential tremors. Additionally, the company has developed AI-powered smart glasses to assist the visually impaired. It also holds the distinction of being the first private hospital in the country to complete 100 robotic-assisted Whipple procedures, marking a major milestone in the treatment of pancreatic cancer.

- Q3FY25 – During the quarter, the company generated revenue of Rs.772 crore, achieving an increase of 27% as compared to the Rs.606 crore of Q3FY24. EBITDA improved by 37% YoY, from Rs.150 crore to Rs.205 crore. Net profit stood at Rs.93 crore, an increase of 21% from Rs.77 crore of Q3FY24. Compared to the previous year, average revenue per operating bed grew by 25%, average revenue per patient grew by 12% and IP volume grew by 14%. Average length of stay has reduced from 4.18 days to 3.75 days during the quarter.

- FY24 – The company generated revenue of Rs.2,511 crore, an increase of 13% compared to FY23 revenue. Operating profit is at Rs.654 crore, up by 4% YoY. The company posted a net profit of Rs.336 crore, a de-growth of 9% YoY.

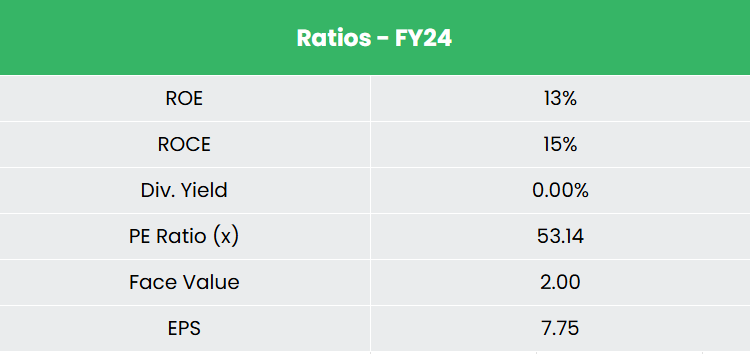

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 23% and 15% between FY21-FY24. The 3-year average ROE and ROCE for the company is around 22% and 25% for the past 3 years. The company has a healthy capital structure with a debt-to-equity ratio of 0.89.

Industry

The healthcare sector in India is one of the largest industries, both in terms of revenue and employment. It encompasses hospitals, medical devices, clinical trials, outsourcing, telemedicine, medical tourism, health insurance, and medical equipment. In 2023, India’s hospital market was valued at US$ 98.98 billion, with projections indicating a CAGR of 8.0% from 2024 to 2032, reaching an estimated value of US$ 193.59 billion by 2032. This growth is expected to be rapid, driven by expanding coverage, improved services, and increasing investments from both public and private sectors. India is also a cost-effective option compared to other countries in Asia and the West, making it an attractive destination for international patients and contributing to the rise of medical tourism. The Indian medical tourism market was valued at US$ 7.69 billion in 2024, with expectations to grow to US$ 14.31 billion by 2029.

Growth Drivers

- Government allocation of Rs.99,858 crore (US$ 11.50 billion) to the healthcare sector in the Union Budget 2025-26, a 9.78% increase compared to the previous year.

- FDI of Rs.97,208 crore (US$ 11.19 billion) into the hospitals and diagnostics sector between April 2000-September 2024.

- Rising income levels, ageing population, growing health awareness and greater penetration of health insurance.

Peer Analysis

Competitors: Global Health Ltd, Aster DM Healthcare Ltd, etc.

We believe KIMS is fairly valued relative to its peers, supported by its solid fundamentals, robust revenue growth, and consistent returns on invested capital.

Outlook

KIMS is aiming for a growth rate of 18–20% in FY26, driven by the launch of new hospitals and operations & management (O&M) contracts. Over the next two years, the company plans to add between 2,000 and 2,500 beds, with more than 2,300 beds already under construction. Its strategic expansion into Tier-2 and Tier-3 cities, along with the enhancement of services in its core regions, appears promising—supported by robust infrastructure and a capable team. Additionally, KIMS’s focus on introducing innovative healthcare solutions is expected to boost its customer base and strengthen its brand value.

Valuation

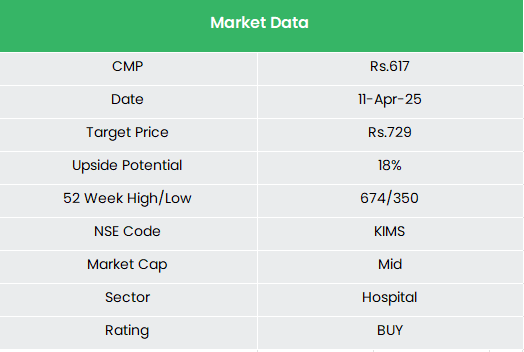

We expect the company to sustain its growth momentum given the multiple capex plans in progress through various greenfield and brownfield projects. We recommend a BUY rating in the stock with the target price (TP) of Rs.729, 50x FY26E EPS.

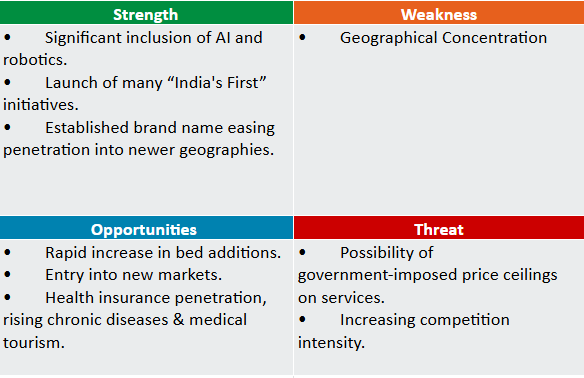

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.