Epigral Ltd – India’s Leading Integrated Chemical Manufacturer

Established in 2007 and headquartered in Ahmedabad, Epigral Ltd. is a pioneering force in India’s chemical industry. Previously known as Meghmani Finechem Ltd, the company commenced its operations with the production of Chlor-Alkali in Dahej. It is a leading manufacturer of Caustic Soda, Caustic Potash, Chloromethanes, Hydrogen Peroxide, Chlorine and Hydrogen. From commissioning India’s first Epichlorohydrin (ECH) plant based on 100% renewable resources and setting up India’s largest CPVC plant, the company is contributing to the nation’s infrastructural growth. It has a state-of-the-art manufacturing facility situated across 60 hectares in Dahej (Gujarat).

Products and Services

Epigral offers a diverse range of essential derivatives and specialty chemicals used in over 15 industries.

- Chlor-Alkali (caustic soda, caustic potash, liquid chlorine, hydrogen gas etc.) that finds applications in alumina, textile, chemicals, soaps and detergents, agrochemicals and pharmaceutical industry.

- Derivative Products (chloromethanes, hydrogen peroxide) that find application in industries such as pharmaceutical, PTFE pipes, refrigerant gas, paper and pulp, textile, chemicals and effluent treatment.

- Derivatives and Specialty chemicals (CPVC resin, CPVC compound, epichlorohydrin (ECH) & chlorotoluene value chain) used in pipes and fittings, windmill, automobile, adhesives, agrichemicals and API.

Subsidiaries: As of FY24, the company has one associate company.

Investment Rationale

- Expansion plans – In FY24, Epigral added 45,000 TPA of CPVC resin capacity, bringing its total to 75,000 TPA. The company now plans to double this capacity to 150,000 TPA by H1FY26, positioning it as the world’s largest CPVC resin plant by capacity. Additionally, Epigral intends to double its Epichlorohydrin (ECH) production from 50,000 TPA to 100,000 TPA, making it the largest ECH facility in India. The combined investment for both expansions stands at Rs.780 crore, with volume contributions expected to begin from FY27. The company is also diversifying into chlorotoluene and its value chain – key intermediates in the production of pharmaceutical and agrochemical active ingredients. This facility was commissioned in Q4FY25, with revenue generation expected from H2FY26 and full capacity utilization targeted by the end of FY26.

- Established position – The company ranks among the top chemical producers in India, with the 4th largest caustic soda capacity at 400 KTPA, 3rd largest caustic potash capacity at 21 KTPA, 5th largest chloromethanes capacity at 50 KTPA, and 3rd largest hydrogen peroxide capacity at 60 KTPA. It also holds the country’s largest CPVC resin capacity at 75 KTPA and operates India’s first ECH plant with a capacity of 50 KTPA. Additionally, in Q4FY24, the company commissioned India’s first chlorotoluene value chain facility at its Dahej complex in Gujarat.

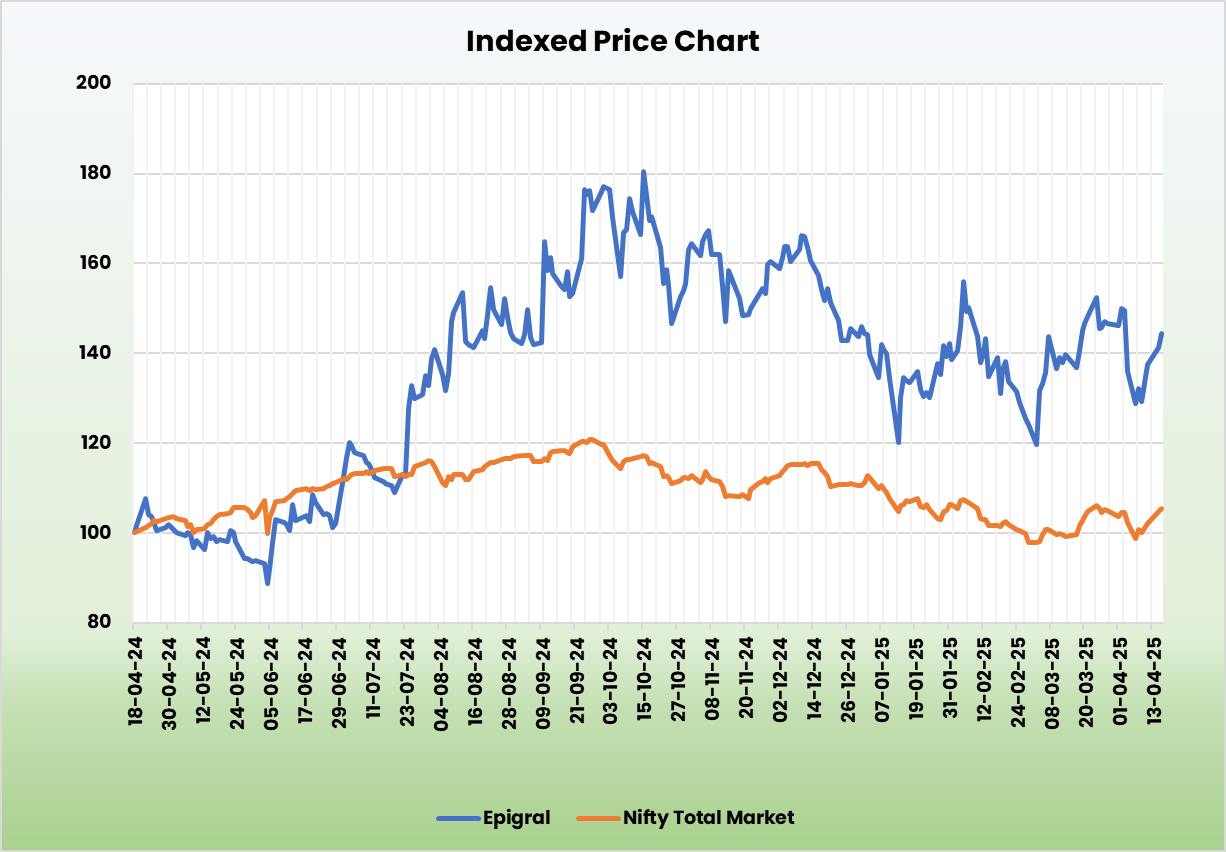

- Q3FY25 – The company has achieved significant volume growth on account of various expansion projects commissioned in the recent quarters. During Q3FY25, the company generated a revenue of Rs.645 crore, achieving an increase of 37% as compared to the Rs.472 crore of Q3FY24. Capacity utilisation was at 81%. EBITDA improved by 49% YoY, from Rs.123 crore to Rs.183 crore. Net profit stood at Rs.104 crore, an upsurge of 112% from Rs.49 crore of Q3FY24. Margins expanded YoY, EBITDA margin from 26% to 28% and net profit margin from 10% to 16%.

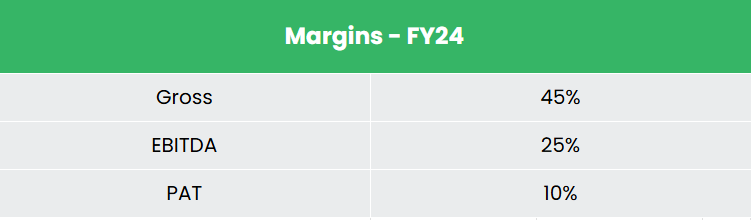

- FY24 – Epigral achieved a volume growth of 15% in FY24. Product mix diversification into derivatives and specialty business, entry into import-substitute products, catering to diverse industries and contribution from new projects commissioned in FY23 aided in the volume growth. However, revenue was reduced on account of decrease in realization across all the divisions. Company’s revenue declined by 12% to Rs.1,929 crore, operating profit declined by 30% to Rs.481 crore and net profit declined by 44% to Rs.196 crore. It is to be noted that during FY24, the entire industry was impacted due to subdued demand, over supply & realizations touching all-time low.

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 33% and 25% between FY21-FY24. The 3-year average ROE and ROCE for the company is around 30% and 26% for the past 3 years. The company has a healthy capital structure with a debt-to-equity ratio of 0.65.

Industry

India’s chemical industry, encompassing over 80,000 commercial products, is highly diverse and broadly categorized into bulk chemicals, specialty chemicals, agrochemicals, petrochemicals, polymers, and fertilizers. Globally, India ranks as the 6th largest chemical producer and holds the 3rd spot in Asia, contributing around 7% to the nation’s GDP. Growth in sectors such as food processing, personal care, and home care is feeling expansion across various segments of the specialty chemicals market. Currently valued at US$ 220 billion, the Indian chemical industry is projected to grow to US$ 300 billion by 2030 and reach US$ 1 trillion by 2040.

Growth Drivers

- An allocation of Rs.1,61,965 crore (US$ 18.7 billion) to the Ministry of Chemicals and Fertilizers under the Union Budget 2025-26.

- 100% FDI is allowed under the automatic route in the chemicals sector with a few exceptions that include hazardous chemicals.

- The Government of India is considering launching a Production Linked Incentive (PLI) scheme in the chemical sector to boost domestic manufacturing and exports.

Peer Analysis

Competitors: Grasim Industries Ltd, DCM Shriram Ltd, etc.

Epigral demonstrates stronger sales growth and more robust investment returns than its competitors, reflecting effective capital allocation and expanding market penetration.

Outlook

The company has demonstrated consistent growth, driven by the launch of new products and a diversified product portfolio. As of the 9MFY25, the company has invested Rs.127 crore in CAPEX. During FY24, it inaugurated a state-of-the-art Research and Development (R&D) Centre in Ahmedabad, thereby enhancing its innovation capabilities and accelerating its strategic shift towards the development of specialty products. The company aims to transition its product mix from the current 45:55 ratio of derivatives and specialty chemicals to chlor-alkali, to a more favourable 70:30 ratio. This strategic realignment focusing on the development of specialized products, many of which are being introduced for the first time in India is expected to position the company as a market leader in the segment. For FY25, the company has maintained a conservative EBITDA margin guidance of 25%, having already achieved 28% in 1HFY25. The expansion in EBITDA has been supported by increased production volumes, resulting in better overhead absorption along with improved realizations and a higher contribution from the derivatives and specialty chemicals business.

Valuation

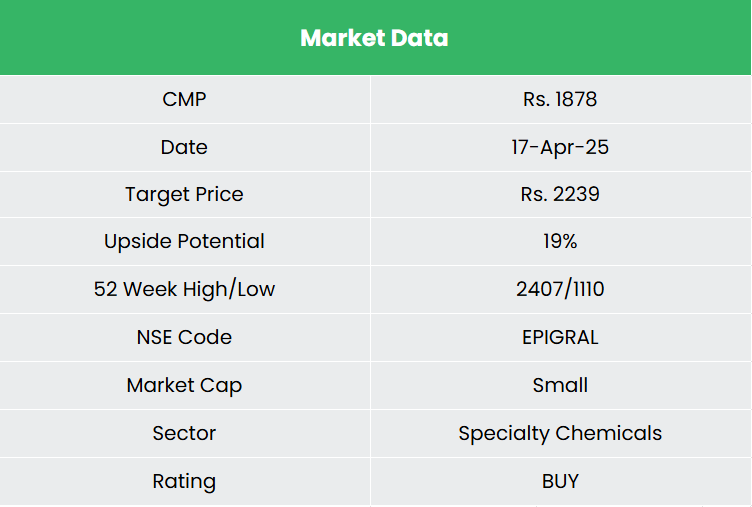

Epigral’s strategy to increase the share of Derivatives in its product mix, coupled with import substitution opportunities, is expected to drive growth in the coming years. Furthermore, its focus on launching ‘India’s first’ products is likely to enhance its market positioning. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,239, 26x FY26E EPS.

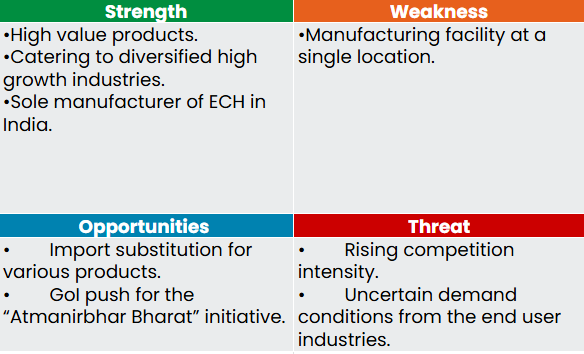

SWOT Analysis

Recap of our previous recommendations (As on 17 April 2025)

Krishna Institute of Medical Sciences Ltd

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.