Mazagon Dock Shipbuilders Ltd – Ship & Submarine Builders to the Nation

A Navratna company operating under the aegis of the Ministry of Defence, Mazagon Dock Shipbuilders Ltd (MDL) is one of the leading shipbuilding yards in India. Incorporated in 1934 and headquartered in Mumbai, the company has established itself as a premier war-shipbuilding yard in India, producing warships for the Navy and offshore structures for Bombay High. The company specialises in constructing, repairing, and refurbishing warships and submarines at its facilities in Mumbai and Nhava. Since inception it has built a total 805 vessels, including 30 warships, ranging from advanced destroyers to missiles boats as well as 8 submarines. Currently, its existing yard accommodates 11 submarines and 10 warships simultaneously.

Products and Services

The company’s product portfolio comprises of warships, cargo ships, passenger ships, supply vessels, multipurpose support vessels, water tankers, tugs, dredgers, fishing trawlers, barges, and border outposts, jackets, wellhead platform main decks, process platforms, jack up rigs etc.

Subsidiaries: As of FY24, the company has 1 associate company and no subsidiaries/joint ventures.

Investment Rationale

- Strategic business initiatives – The company has acquired 15 acres of land next to its current shipyard, where it plans to build a new facility. This will include a much larger dry dock, allowing for the construction of bigger warships and enhancing its ship repair and maintenance services. At the same time, the company is constructing the country’s largest floating dry dock at Nhava Island near Mumbai to accommodate large ship orders. Additionally, the company has established a dedicated “Make in India” department, leading to the successful indigenization of 57 key items and systems for ships and submarines. MDL has also contributed 1,017 items to the Ministry of Defence’s Positive Indigenization List (PIL). Collaborations with BEL and other partners are ongoing to further indigenize additional components. Moreover, the company has begun expanding its product portfolio into the aviation sector and has secured an MRO contract for helicopter repairs.

- Major orders in pipeline – MDL is a strong contender for major future projects of Indian Navy, Indian Coast Guard and overseas clients. Some of the identified major business opportunities where the company is a strong contender includes next generation corvettes, 5 next generation destroyers and 6 project P75(I) conventional submarines. The company is also anticipating the follow-on orders on frigates for Project 17 Bravo. Beyond Navy, the company is also accepting orders from Indian Coast Guard and export clients. It has got order worth Rs.2,684 crore from Indian Coast Guard for the construction of advanced patrol vessels. The company is also diversifying into the Maintenance, Repair & Overhaul (MRO) of MI-17 helicopters for the Nepalese Army. On the non-defence front, the company has signed an MoU with State Disaster Management Authority, Goa. The MoU will focus on developing and implementing an “AI-based Wireless Disaster Detection, Rescue & Communication System. It has also won a Rs.1,486 crore contract from ONGC for pipeline replacement related works.

- Q3FY25 – MDL reported a revenue of Rs.3,144 crore marking an increase of 33% compared to the Rs.2,362 crore revenue of Q3FY24. Operating profit stood at Rs.1,104 crore against the Rs.808 crore of Q3FY24, a surge by 37% YOY. The net profit stood at Rs.807 crore which is a growth of 29% as compared to the Rs.627 crores of same period in the previous year. The EBITDA margin was reported to be 35% and net profit margin was reported to be 26%.

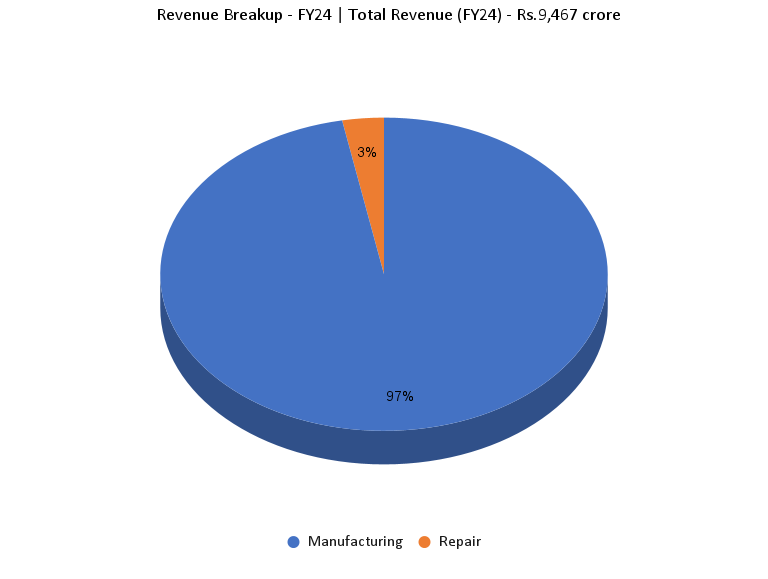

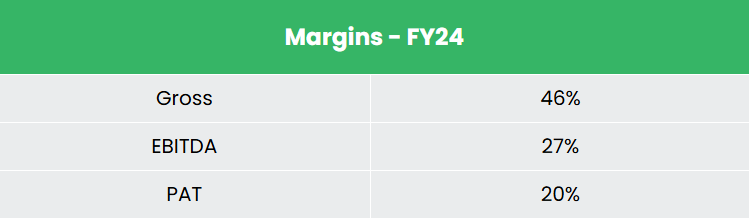

- FY24 – The company generated revenue of Rs.9,467 crore during FY24, an increase of 21% compared to the FY23 revenue. EBITDA was at Rs.2,513 crore, up by 69% YoY. The company reported net profit of Rs.1,937 crore, an increase of 73% YoY.

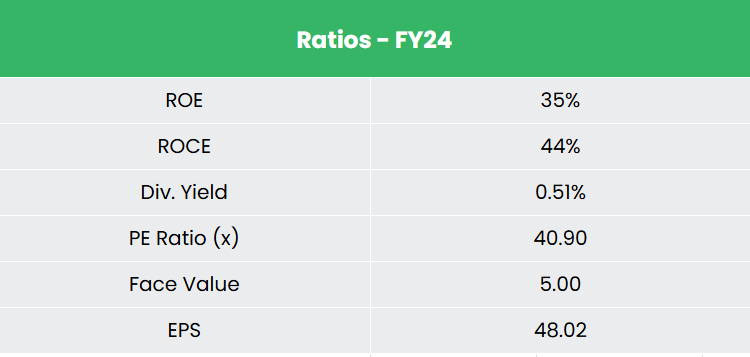

- Financial Performance – The company has generated revenue and net profit CAGR of 33% and 47% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 27% and 33% for FY21-24 period. The company has strong balance sheet with zero debt in its capital structure.

Industry

India is one of the strongest military forces in the world and the industry holds a place of strategic importance for the Indian government. The country’s defence manufacturing industry is rapidly growing, driven by substantial government investments, increasing exports, and policies aimed at fostering self-reliance and technological innovation. As part of the ‘Aatmanirbhar Bharat’ (Self-Reliant India) initiative, the government has prioritized the Defence and Aerospace sectors, focusing on building domestic manufacturing capabilities supported by a strong research and development framework. To modernize its military and decrease dependence on foreign defence imports, the government has introduced several initiatives to promote ‘Make in India’ efforts through policy backing. Additionally, India has set an ambitious goal of achieving US$ 6.02 billion (Rs. 50,000 crore) in annual defence exports by 2028-29. With an aim to provide financial assistance to Shipbuilders and grant infrastructure status for the industry the government has formulated the Shipbuilding Financial Assistance Policy wherein it has set aside Rs.40 billion to implement the scheme.

Growth Drivers

- In 2025-26 the central government has allocated Rs.6,81,210 crore for the Ministry of Defence which is 6% higher than the previous year.

- Growing demand for defence manufacturing given the rising concerns of national security.

- Provision for 100% Foreign Direct Investment (FDI) through Government route and 74% through Automatic route into the defence sector.

Peer Analysis

Competitors: Cochin Shipyard Ltd, Garden Reach Shipbuilders & Engineers Ltd, etc.

Among the above competitors, MDL stands out with steady revenue growth, superior return ratios, and strong earnings potential, reflecting the company’s financial stability and its ability to efficiently generate income and returns on invested capital.

Outlook

We believe MDL has strong growth potential due to its operational ties with the Government of India (GoI) and its role as a key defence public sector undertaking that manufactures warships and submarines for the Ministry of Defence (MoD). With increasing concerns about national security, the Indian defence manufacturing industry is expected to grow. Management has projected a revenue growth of 10% to 12% for FY25 and plans a capital expenditure of Rs.5,000 crore over the next few years. These planned expansions are set to nearly double the company’s capacity, allowing it to build larger vessels and take on multiple large-scale projects simultaneously. As of December 31, 2024, MDL’s order book stands at Rs.34,787 crore. Additionally, the company’s focus on indigenization has led to reduced construction costs, a trend expected to continue, resulting in stable profit margins and earnings.

Valuation

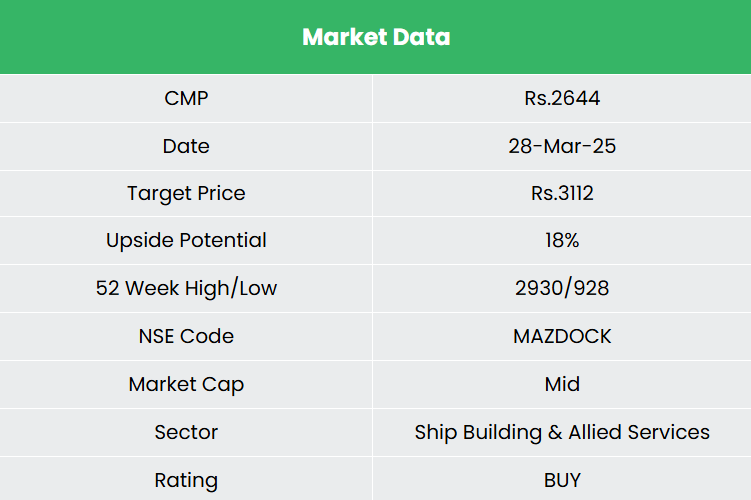

As a leading shipyard in the construction of frontline warships and submarines, we believe that the company will continue to be a key player in fulfilling the nation’s defence infrastructure needs. We recommend a BUY rating in the stock with the target price (TP) of Rs.3,112, 33x FY26E EPS.

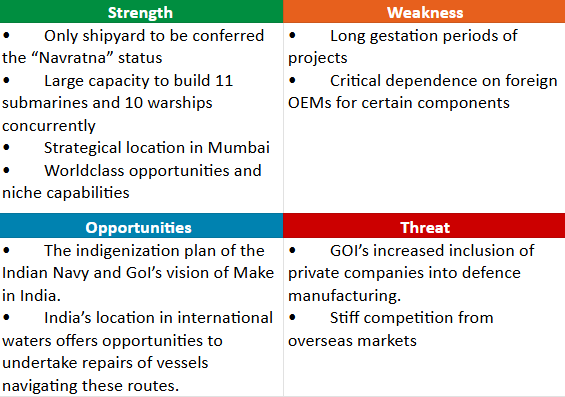

SWOT Analysis

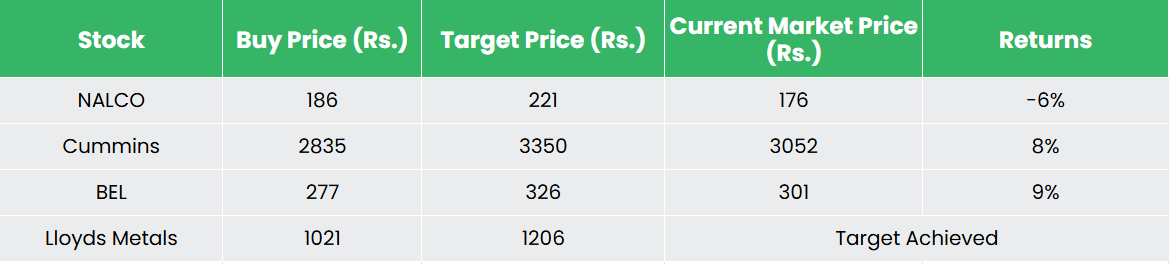

Recap of our previous recommendations (As on 28 March 2025)

National Aluminium Company Ltd

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.