Eicher Motors Ltd. – Made Like A Gun

Incorporated in 1982 and headquartered in Chennai, Eicher Motors Ltd. (EML) is a globally acclaimed automobile company. It is the listed parent company of the iconic Royal Enfield (RE) brand, the oldest motorcycle brand in continuous production. With 3 world-class manufacturing sites in Chennai, India and 2 research and development (R&D) centres in Chennai, India and Bruntingthorpe, UK, EML is a key player in mid-size motorcycle segment, RE being the global leader in the 250cc – 750cc, mid-weight motorcycles segment. The company is also present in commercial vehicles segment through its subsidiary – VE Commercial Vehicles Ltd (VECV). VECV is a joint venture between the Volvo Group and Eicher Motors Ltd. The joint venture of EML (54.4%) and Volvo (45.6%) came into existence with effect from July 1,2008. It manufactures trucks across 4.9-55T and buses with a seating capacity of 12-72 across light, medium and heavy-duty applications.

Products and Services

The company operates under two business segments:

- Motorcycles – Motorcycles includes Royal Enfield’s premium line-up such as Hunter 350, Classic 350, Meteor 350, the 650 parallel twin motorcycles – Interceptor 650 & Continental GT 650, Super Meteor 650, the adventure motorcycles – Himalayan adventure tourer and the cram 411 ADV Crossover, and Bullet 350.

- Commercial vehicles – VECV includes the complete range of Eicher branded trucks and buses, Volvo trucks and buses in India, engine manufacturing and exports for Volvo Group, non-automotive engines, and Eicher component business.

Subsidiaries: As of FY23, the company had 10 subsidiaries and 1 joint venture.

Key Rationale

- New launches – During Q3FY24, the company launched Himalayan 450 featuring EML’s newest engine platform Sherpa 450. The market response to the new model is encouraging and the company is planning to launch it in EU in coming months. The company also launched Shotgun 650 in EU and UK, a custom inspired motorcycle. It was launched in foreign markets and the company has plans to start retails in India also. It also launched Royal Enfield Wingman, a new feature on the pre-existing Royal Enfield app that enables a rider with critical vehicle information such as live tracking, last parked location, trip summary etc.

- Promising VECV – VECV recorded highest ever Q3 sales of 20,706 units in FY24. During the current quarter, the company also began deliveries of India’s first electric 5.5-ton GVW truck, the first Eicher Pro 2055 electric vehicle and continued delivering electric buses. Heavy-duty trucks, combining Volvo and Eicher achieved their best-ever Q3FY24 sales with 6,210 units as against last year in Q3FY23 of 5,241 units with a market share of 9.6%. Light and medium-duty trucks also hit a Q3FY24 record with 9,800 units as against 9,239 units in Q3FY23, capturing 34.5% market share. The bus division, parts business for both Eicher and Volvo and VE Power units also reached an all-time high during Q3FY24.

- Q3FY24 – During the quarter, EML sold 229,214 motorcycles which is an increase of 4% compared to Q3FY23. It also recorded highest ever domestic retail for Royal Enfield so far with the international sales improving by 11% YoY during the period. EML (excluding revenue from VECV) generated highest ever revenue of Rs.4,179 crores, which is an increase of 12% compared to Q3FY23. EBITDA grew by 27% YoY to Rs.1,090 crores. The company reported net profit of Rs.996 crores which is an upsurge of 34% compared to the corresponding quarter of the previous year. VECV revenues rose to Rs.5,483 crores, up 19% from Rs.4,604 crores in Q3FY23. EBITDA for the quarter is Rs.437 crores, up 44% from Rs.304 crores in Q3FY23 and EBITDA margin is 8% as against 6.6% in Q3FY23. Profit after tax is Rs.210 crores, up from Rs.117 crores in Q3FY23.

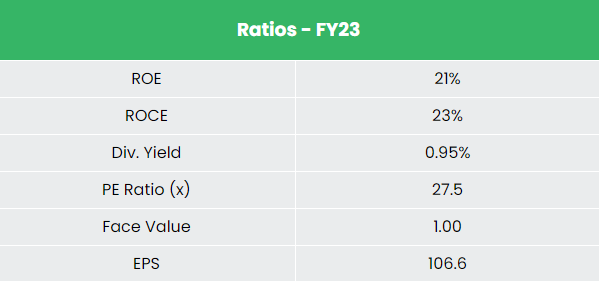

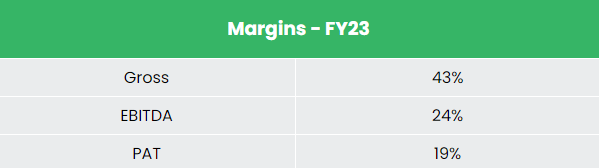

- Financial performance – The company has generated a revenue and PAT CAGR of 16% and 17% over the period of 3 years (FY20-23). Average 3-year ROE & ROCE is around 16% and 21% for FY20-23 period. The company has robust capital structure with a debt-to-equity ratio of 0.03.

Industry

The Indian automobile industry has historically been a good indicator of how well the economy is doing, as the automobile sector plays a key role in both macroeconomic expansion and technological advancement. The two-wheelers segment dominates the market in terms of volume, owing to a growing middle class and a huge percentage of India’s population being young. India is the world’s largest manufacturer of two-wheelers, with over 21 million produced annually. The nation enjoys a strong position in the global heavy vehicles market as it is the largest tractor producer, second-largest bus manufacturer, and third-largest heavy truck manufacturer in the world.

Growth Drivers

- The PLI scheme (outlay of $3.5 Bn) for the automobile sector proposes financial incentives of up to 18% to boost domestic manufacturing of advanced automotive technology products and attract investments in the automotive manufacturing value chain.

- Government of India and Indian automotive industry has come up with Automotive Mission Plan 2016-26 to lay down the roadmap for the development of the industry.

- The automobile sector received a cumulative equity FDI inflow of about US$ 35.40 billion between April 2000 – September 2023.

Competitors: Hero MotoCorp, TVS Motors, etc.

Peer Analysis

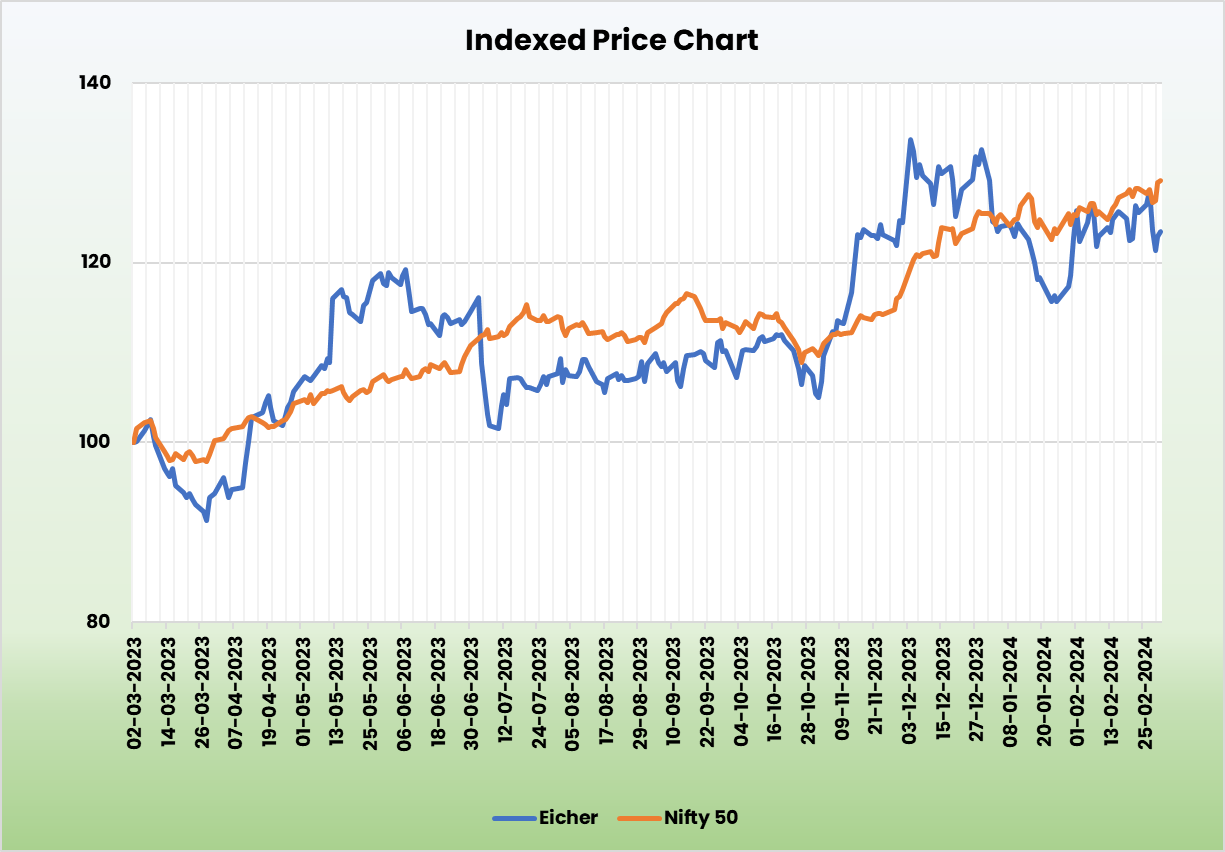

Among the above competitors, EML has higher return ratios in line with the growth in the sales. This indicates the company’s ability to generate better profits for the capital invested. EML has better debt-to-equity ratio compared to Hero and TVS. This robust capital structure of EML provides it an additional buffer against the company’s financial risk to raise additional capital.

Outlook

The RE & VECV segment is actively working on new product launches. The newly launched Himalayan 450 and Sherpa 450 is receiving encouraging response from the market and the company has plans to introduce it in newer markets. VECE is planning for the launch of new small commercial vehicles starting from Q1CY25. The company has also come up with industry first buyback and reown programs. VECE is introducing new range which span the GVW of 2-3.5 ton and addresses a market segment of over 300,000 units per annum. This segment is expected to grow with urbanization, growth of e-commerce and last-mile delivery.

Valuation

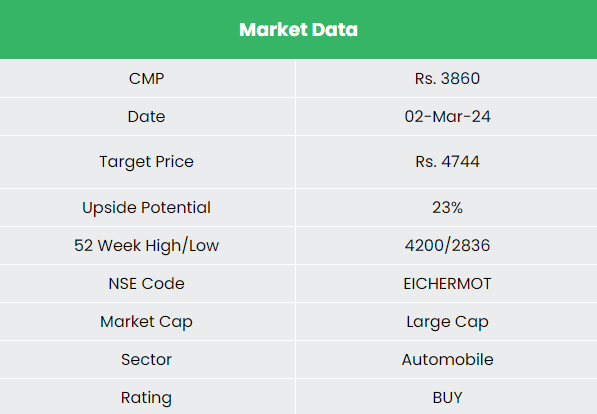

The company is focusing on further penetration in the existing markets through its existing line-up of products in addition to timely launch of new products. We expect strong growth potential in RE given its continued volume outperformance and its increasing acceptability among the rider communities. We recommend a BUY rating in the stock with the target price (TP) of Rs. 4,744, 32x FY25E EPS.

Risks

- Risk from competitors: Increasing competitive intensity poses a risk to the company in the >250cc segment where the company has the highest market share.

- Macro-Economic factors: Macro-economic headwinds driving lower exports for longer could pose a downside risk.

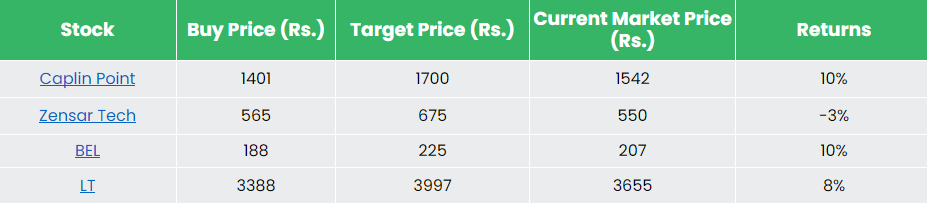

Recap of our previous recommendations (As on 02 Mar 2024)

Please click on the below links to read our previous reports: