We have always remained strong proponents of systematic investment plans (SIPs) in equities. The reason it works over the long run is because it helps in averaging out the buying price in equities. Another significant advantage is from a behavioral angle – automation of monthly savings and removing the need to take monthly decisions.

While no doubt SIPs are a great behavioral tool for long term investing, there is also a minor hitch. Once you set an SIP, you end up buying into equity markets each and every month for the same amount irrespective of the market valuation. While the majority of the time, markets revolve around neutral valuations, there are some phases where the markets are extremely cheap or insanely expensive. Buying in expensive markets is obviously not a great thing to do and so is not buying higher amounts in cheap markets.

But even if you want to take advantage of market falls (read as cheaper prices) and invest higher amounts, from where will you get the extra money to invest?

This led us to a simple question…

What if we could solve for this minor challenge and make your SIP experience even more awesome?

That is when we came up with this simple yet super powerful idea of Power SIP.

Power SIP – A Turbo-Charged SIP Strategy for Higher Returns

Do you remember how we all buy our onions. There are few months every one or two years, where the onion prices hit the roof. Now most of us inevitably reduce our onion consumption and again when the prices fall we accumulate more.

What if we had a similar “onion buying” strategy for our equity SIPs where we will buy equities when it is cheap and in months where equities become expensive we will lower our equity allocation and wait for lower prices.

Power SIP is designed to do exactly this!

So, how does it work?

In case of a simple Equity SIP, you will accumulate equities each and every month for the same amount irrespective of the underlying market valuations. This works because over the long run you average out expensive phases, cheap phases and normal phases.

The idea behind Power SIP is to improve on this by taking advantage of the cheap phases and expensive phases and varying the monthly allocation going into equities.

Power SIP is designed to automatically lower your monthly investment into equities when markets become expensive and temporarily park the remaining amount in a debt fund. Whenever the market turns cheap, Power SIP will automatically invest much more than your actual monthly investment into equities.

But where will you get the extra amount from?

Remember the amount you had temporarily parked in debt. The Power SIP will tap into the debt fund to invest higher amounts into equity at lower valuations!

But hey, how do you know when the markets are cheap or expensive?

We have collaborated with ICICI Prudential Mutual fund and built a valuation model based on MCAP to GDP which helps us to decide on the market valuations. The reason why we chose ICICI Prudential Mutual Fund was because of their long term successful track record in managing dynamic asset allocation strategies (10+ year track record in ICICI Balanced Advantage Fund and you can also read more about the fund here) and they were instrumental in popularizing the dynamic asset allocation category. Most of the other fund houses had introduced their dynamic asset allocation products in recent years after seeing the success of ICICI Balanced Advantage Fund.

A basic doubt – How do I know if this valuation model works?

Fair enough! This is why put our model to test over the last 15 years – where the markets saw a range of events from Subprime Crisis, Euro Crisis, Fed Taper, China Crisis, India elections, Demonetization, US Elections, Brexit, NBFC Crisis, Mid & Small cap crash, US China Trade War, Covid Crash etc.

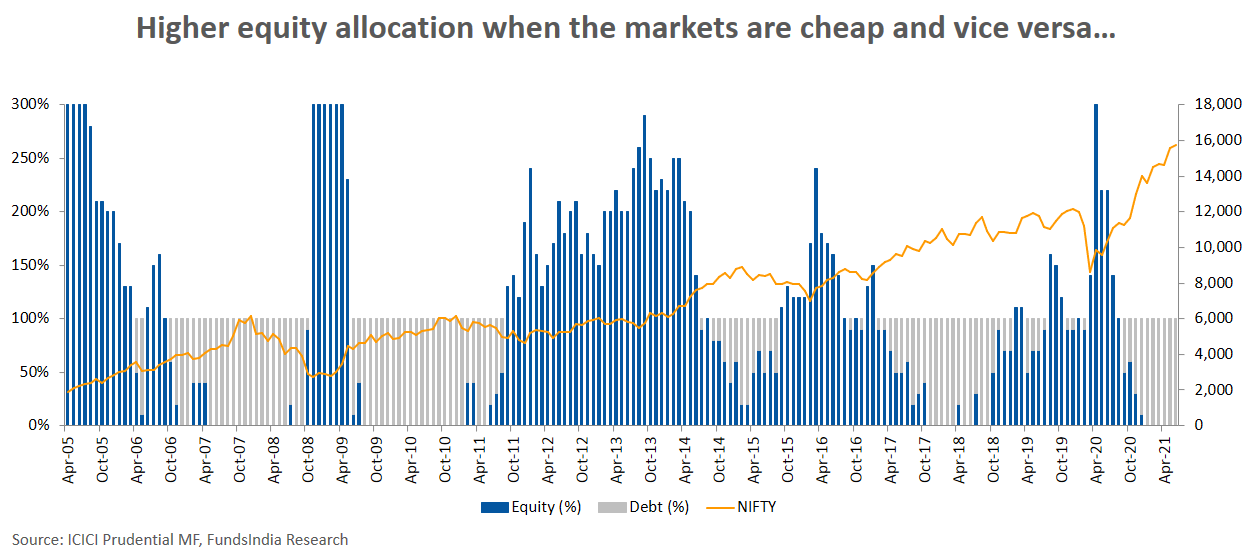

Here is how the allocation to equities varied as per the model for the past 15 years. As seen below the model has been fairly consistent in increasing the SIP allocation into equities when the market fell and the valuations became cheaper and vice versa. Also, this model has helped us improve returns by around 1-3% over a normal SIP over 5 year periods. (will be explained later in detail)

The monthly equity investments can be up to 300% of the SIP value during cheap markets with the excess amount getting shifted from debt schemes to the equity schemes. Similarly, when markets become expensive, the allocation to equities can go as low as 30%* (i.e. the 70% of the SIP amount for that month will be temporarily parked in debt).

*Effective Jul-21, the minimum monthly equity allocation of the Power SIP model has been revised from 0% to 30%

Let’s take a simple example..

Assume, you are investing a monthly SIP of Rs. 10,000 into Power SIP. During every installment, our valuation model will decide on how the money should be allocated between Equity and Debt.

The following are the ways in which the money will be invested

1. Markets are expensive (0-50% of monthly investment into equities): Assume the valuation model indicates 0% allocation to equities. The entire Rs. 10,000 is temporarily invested into debt schemes.

2. Markets are neutral i.e neither expensive nor cheap (50-100% of monthly investment into equities): Assume the valuation model indicates 80% allocation to equities. In this case Rs. 8,000 will be invested into equities and Rs. 2,000 into debt.

3. Markets are cheap (100-300% of monthly investment into equities): Assume the valuation model indicates 300% allocation to equities. In this case Rs. 30,000 will be invested into equities. Rs. 10,000 will come from your actual monthly investment. The remaining 20,000 will be shifted from money that was previously parked into the debt schemes when the markets were expensive.

So the Power SIP over reasonably long periods (of more than 5 years) will act pretty similar to a normal SIP during periods where the valuations are neutral, lower the monthly investment amount into equities when markets are expensive and will go super aggressive during cheap markets by investing higher allocations into equities!

Here is the best part – the whole process is completely automated and you can sit back and relax while the Power SIP does all the hard work!

Now, how to invest?

Power SIP comes in two different options

- Passive Plus

- Active Plus

You can choose to invest in one or both of them as per your preference.

Let us have a look at each of these options..

Option 1: Power your SIPs with ‘Passive Plus’ Strategy

As the name suggests, ‘Passive Plus’ strategy follows the passive investing approach but with a little extra.

In this strategy, the equity investments are allocated equally into 2 large cap indices – ICICI Prudential Nifty Index Fund (representing the Nifty 50 index) and ICICI Prudential Nifty Next 50 Index Fund (representing the Nifty Next 50 index). The debt investments are temporarily parked into ICICI Prudential Money Market Fund (a high credit quality fund – 100% AAA exposure – with low interest rate risk) when the markets are expensive. The amount under the debt scheme is later shifted to the equity schemes (up to 300% of Power SIP value per month) when the market valuations become cheaper.

Consistent Outperformance

Based on the back-tested results, ‘Passive Plus’ Power SIP has given higher returns on 99% of all the 5-year rolling periods over the past 15 years when compared to the normal SIP investing in the Nifty indices.

When measured over all 5 year periods in the last 15 years, 83% of the times the Power SIP strategy has given more than 10% returns.

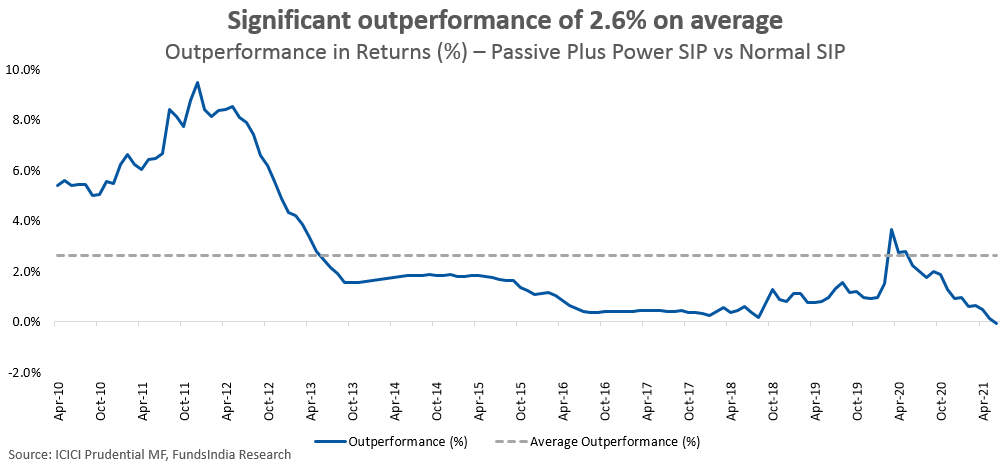

‘Passive Plus’ Power SIP strategy has given a strong outperformance of 2.6% on average versus the normal SIP.

In fact,

- 1 out of 3 times, the Power SIP has outperformed a normal SIP by more than 2%

- 2 out of 3 times, the Power SIP has outperformed a normal SIP by more than 1%

Option 2: Power your SIPs with ‘Active Plus’ Strategy

With ‘Active Plus’ Power SIP strategy, the investments are actively managed i.e. there is a fund manager and team who will build the portfolio for us.

In this strategy, the equity investments instead of passive funds are allocated into ICICI Prudential Value Discovery Fund – a ‘Value’ style oriented equity scheme. Similar to the passive plus strategy, when the markets become expensive, the investments are temporarily parked in the debt scheme, ICICI Prudential Money Market Fund – with the view of transferring the same to the equity scheme at a later point. The amount under the debt scheme is shifted to the equity schemes (up to 300% of monthly Power SIP value) when the market valuations become cheaper.

Consistent outperformance

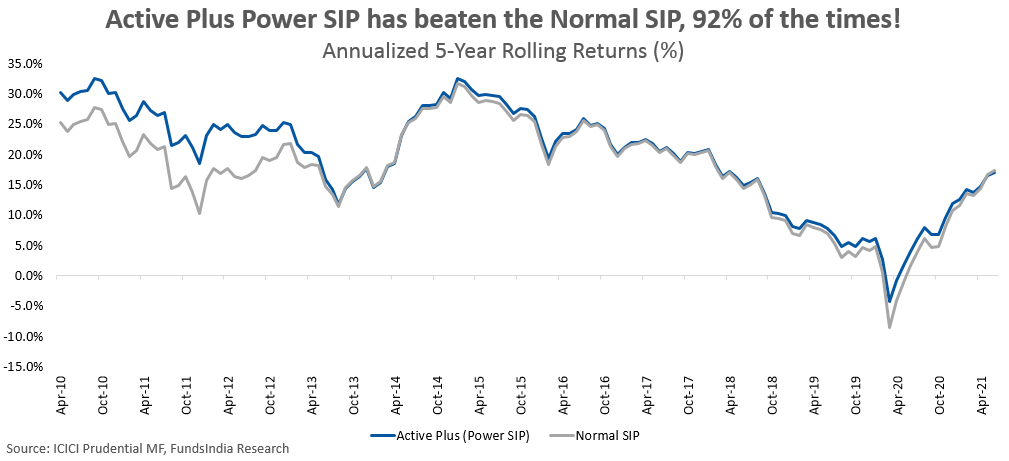

‘Active Plus’ Power SIP has beaten the returns of the normal SIP investment made into ICICI Prudential Value Discovery Fund 92% of the times on a 5-year rolling basis in the last 15 years.

When measured over all 5 year periods in the last 15 years, almost 80% of the times the Power SIP strategy has given more than 12% returns.

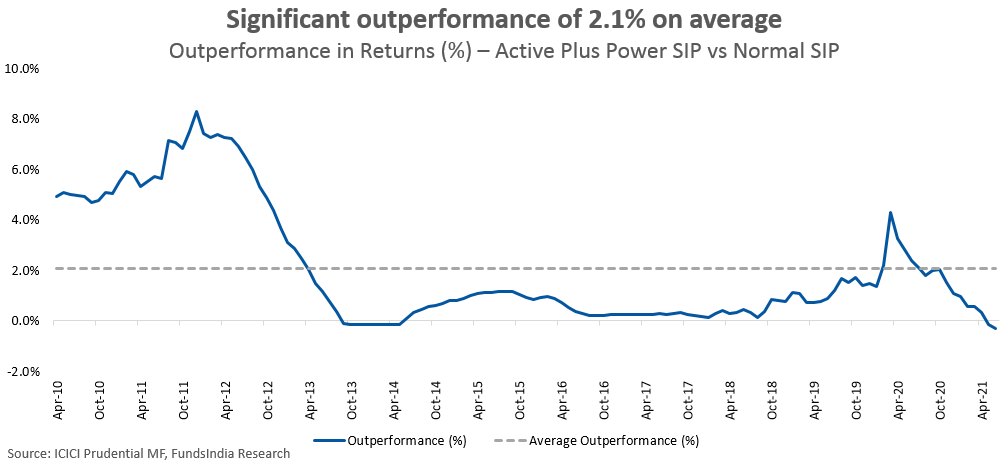

On a 5-year rolling basis, this strategy has beaten the normal SIP by 2.1% on average over the back-tested period.

ICICI Prudential Value Discovery Fund is a fund with ‘value’ bias. The ‘value’ style has not been in favour over the past five years. This is not just true to India, even globally value funds have had a tough phase over the last few years. As a result, all funds following the ‘value’ investment style have underperformed relatively when compared to the funds following the ‘quality’ style. Quality oriented funds did really well as valuations for quality stocks continued to increase despite higher starting levels – due to the fact that growth was scarce and concentrated in few quality stocks.

Going by the long proven history of ‘value’ style doing well over the long run, we expect mean reversion to play out in the coming years with the possibility of significant recovery in performance for ‘value’ funds. The base thesis is that as the economy recovers and growth becomes more widespread across companies, this can be a favorable environment for ‘value’ investing. This is why we have chosen this particular active fund despite its near term underperformance, taking into account our positive outlook for ‘value’ style, the fund’s strong vintage and robust long term track record.

When will the Power SIP not work?

As with all strategies, this definitely is not a magical solution which will always work in the short run.

In bubble phases where the markets continue to rally despite higher valuations, the Power SIP may underperform in the short run as it will continue to allocate lower amounts into equities. The Power SIP will patiently wait for a market correction or cheap valuations to buy aggressively into equities.

Over a complete market cycle (around 5-7 years) we expect the Power SIP to take advantage of both the bubble and cheap valuation phases and deliver outperformance.

Suitability

If you are looking to enhance your long term Equity SIP (5+ years) returns versus a normal SIP with lower volatility the Power SIP strategy can be a great choice to consider.

‘Passive Plus’ Power SIP is suitable for investors who prefer passive investing and would like to reap the diversification benefit of investing in the largest 100 companies (in terms of market cap).

‘Active Plus’ Power SIP is suitable for investors who would like to play the ‘value’ style with the advantages of active management.

Summing it up

- Power SIP is a turbo-charged SIP strategy designed to deliver higher returns versus a normal SIP by investing higher allocation into equities at lower valuations and vice versa

- Valuation model developed in collaboration with ICICI Prudential Mutual Fund which is based on MCAP to GDP indicator

- Power SIP has two options – ‘Passive Plus’ and ‘Active Plus’

- Both the strategies have consistently outperformed their normal SIP version on a 5 year basis based on the back-tested returns for the past 15 years.

- ‘Passive Plus’ is suitable for investors preferring passive investing and ‘Active Plus’ is suitable for investors preferring value style of investing

- Invest with a minimum time horizon of 5+ years

(The blog has been updated with latest data on 20-Jul-21)