I have money but I am scared to invest now in equities…

Most of us during our working careers will have two forms of cash flows

- Regular Cash Inflows from Monthly Salary

- Occasional Cash Inflows – sold a property, performance bonus, sold esops, inheritance etc

When it comes to regular cash inflows, SIP (Systematic Investment Plan) is a simple and proven long-term approach to invest and grow your monthly savings. This works perfectly well for most of us and also automates the entire decision-making process.

However, the decision to invest occasional cash flows into equities is not so straightforward and gets a little daunting, especially, when the amount is large.

The biggest worry point is the inevitable question – “Is now the right time?”

- Should you invest now or wait for a market correction?

- What if you invest now and the market falls?

- What if you don’t invest now and the market continues to rally?

- What if markets correct and you are not able to enter back at the right time?

Now let us be honest. Thinking through these questions is complex, difficult, and takes a lot of mental effort. We often get into the ‘analysis-paralysis’ mode.

In the end, most of us end up picking the easiest choice – ‘I WILL DECIDE LATER’.

What if you had a simple framework that could guide you through this decision, not only now but also in the years to come.

This is exactly what we will be sharing with you in this article.

Have a sip of good chai and let us dive in…

What is the commonly prescribed solution when you have to invest a large sum of money into equities?

The common wisdom goes like this…

“The best time to invest in equities is the time when you have the money”

While there is a natural tendency to dismiss this guidance on the basis of its simplicity, let’s check for actual evidence and find out if this rule stands the test of time.

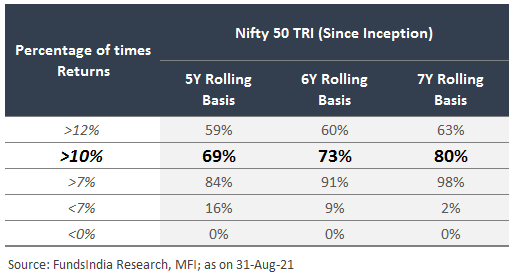

Any investor who invests in Equity markets is generally expected to have at least a 5-7 year time frame. Let us check your odds of making decent returns over a 5Y-7Y period covering each and every possible investment date in the last 22+ years.

GREAT!

Roughly 70% of the time, a simple ‘invest-immediately-when-you-have-the-money’ strategy combined with loads of patience to ignore frequent market tantrums provided you decent return outcomes (greater than 10% CAGR) over 5 years. Further, simply extending time frames by 1-2 years improved the odds to around ~80%.

So, the simple rule – “The best time to invest in equities is the time when you have the money” makes sense and works well 80% of the time.

BUT…

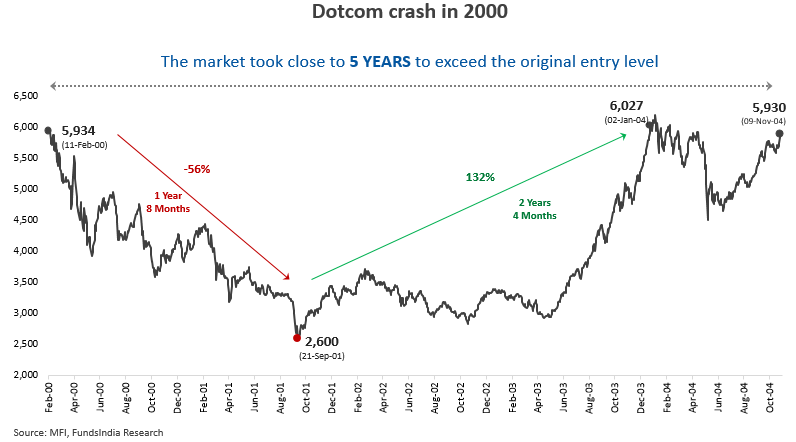

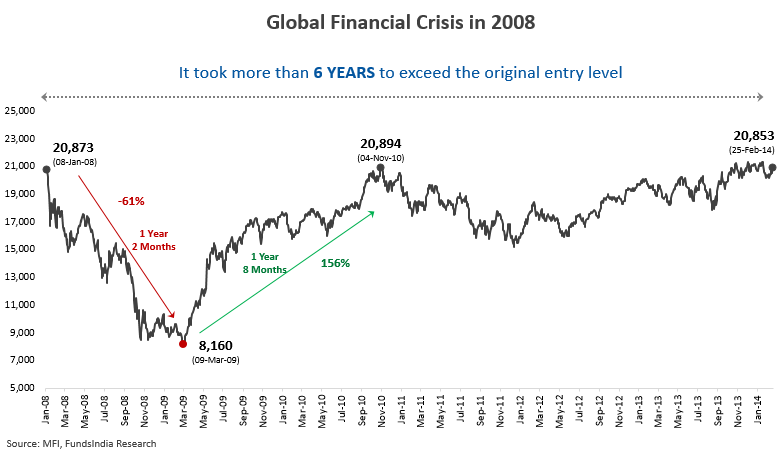

What if we end up in the unlucky 10-20% part of the statistics where even the 5-7 year returns looked dismal?

To put that in perspective, this is how bad it gets when you get the entry wrong…

While this may look scary, even investing at the worst entry point worked out well if given more time and patience (but a lot higher than what is usually required).

So does it mean the solution is – to invest when you have the money?

While this solution works perfectly well over long periods of time, there is a small nuance that it ignores – the simple fact that – You and I are HUMAN!

It is a lot easier to analyze these long-term returns in hindsight. But unfortunately, this analysis ignores the most important factor which cannot be backtested – YOUR EMOTIONS.

The feeling of regret and sleepless nights, when you invest your money and it starts to go down immediately, cannot be fully understood until you have experienced it.

Imagine living with the frustration of ‘If only I had waited for some more time’, for several years.

- The more this painful period prolongs, higher the odds of you and I giving up on our investments (read as selling and taking out our money at a loss).

- Larger the sum of money, the greater the emotional pain and higher the chances of giving up.

So while theoretically, buying whenever you have the money is a decent approach, in reality, the simple fact that we are emotional and human, means that this is far easier said than done.

Now how do we solve this?

The starting point is to accept that the BEST strategy to deploy your money will only be known 5 years later. Right now, we are dealing with several versions of the future that can possibly play out.

Obviously, in hindsight, it will be crystal clear on which strategy was the best as only one version of the future would have played out.

Since we can’t predict which version of the future will play out, the basic idea is to optimize for a strategy that will help you minimize regret across different versions of the future which can play out.

But what does this really mean?

Let us start from the basics.

In the near term (say next 1 year), markets can have three different versions of the future

Version 1: Market moves up

Version 2: Market goes down

Version 3: Market remains flat

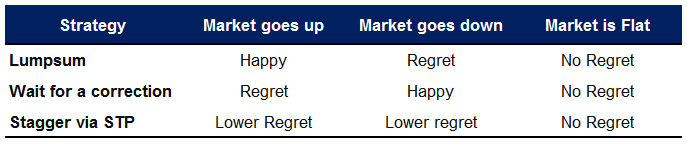

Let us start with the simplest two options to deploy our money:

- Do a lump sum (i.e invest the entire money at one go)

- Wait for a correction to invest

Now since we don’t know whether markets will go up or down in the near term, both choices have one scenario where we will regret.

While it’s not possible to eliminate regret completely, what if we combine both strategies to try and minimize the regret.

In other words, instead of putting the entire money at one go, we spread it across a longer time frame. This can be done via the STP (Systematic Transfer Plan) option where we first park the entire money in a safe debt fund and transfer it to the intended equity fund at predefined intervals (say weekly or monthly) over a specified time frame.

In this case,

- If markets go up…

Had you waited for a market correction you would have regretted missing the entire rally. Now your regret is lower as you are already partially invested and continue to invest. - If markets go down…

Had you invested everything at one go you would have regretted your decision as your entire money is down. Now your regret is lower as you didn’t invest everything at one go and only some amount is invested. Further you also get to invest the rest of the money at lower prices.

But now comes the next logical question…

How long do you stagger?

Scenario 1: If you stagger over a long time frame and the market immediately moves up you still have a large part of your money not participating in the equity rally.

Scenario 2: If you stagger over a short time frame and the market goes down you still have a large part of your money taking a hit in the equity fall.

So we need a framework to reduce our regret even while we stagger our money

Here is how we are thinking through this dilemma…

Rule 1: Larger the Amount, Longer the Deployment Time

The larger the amount of money the more we worry about the downside compared to the upside. Your ability to handle the same 20% fall might be very different depending on whether you have Rs 10 lakhs or Rs 10 crores to invest.

Behavioral Science also supports this view and has found that the pain of losing is more acute than the pleasure of gain – we feel almost twice the emotion over a loss as opposed to a gain. This is referred to as Loss Aversion.

One way to solve this is using a simple rule – Larger the Amount, Longer the Deployment Time

But what is a large amount for me might be a small amount for someone else. How do we contextualize this?

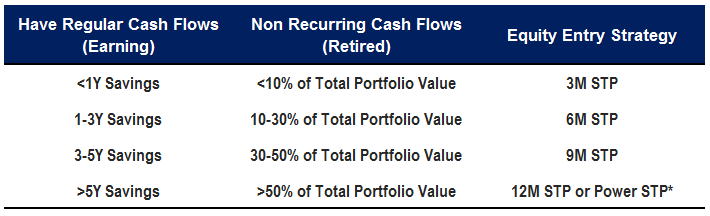

Here is how you can do this for the two broad categories of investors

- Retired with no future cash flows

- In this case, the new amount as a % of the existing portfolio can help you contextualize the relative value

- In this case, the new amount as a % of the existing portfolio can help you contextualize the relative value

- Earning with regular cash flows

- In this case, the new amount represented as ‘no of years it takes to save this amount’ can help contextualize the relative value

- In this case, the new amount represented as ‘no of years it takes to save this amount’ can help contextualize the relative value

Based on the above thought process, let us build our entry strategy:

While this is a good enough approach, how can we improve this further?

Enter Valuations!

Rule 2: More Expensive the Valuation, Longer the Deployment Time

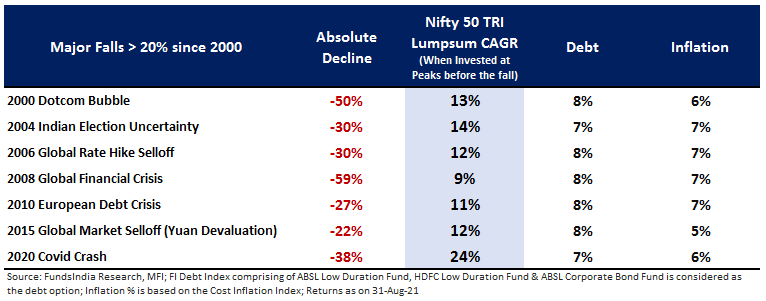

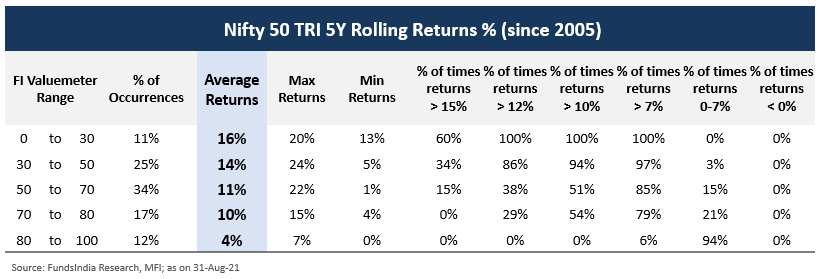

When we studied past Indian market history, we found that valuations are usually inversely correlated to long term equity returns (i.e higher starting valuations indicate higher odds of lower long term equity returns and vice versa)

We went back 16+ years and checked for future 5-year equity returns for Nifty 50 TRI at different starting valuations (proxied by our internal valuation indicator – FundsIndia Valuemeter – based on 4 valuation parameters – MCAP/GDP, PE Ratio, PB Ratio and Earnings Yield/GSec Yield).

Here is what we found…

Takeaway:

- More expensive the starting valuation, higher the odds of dismal future returns – better to deploy slowly over a longer period of time

- Lower the starting valuation, higher the odds of good future returns – better to deploy immediately over shorter time frames

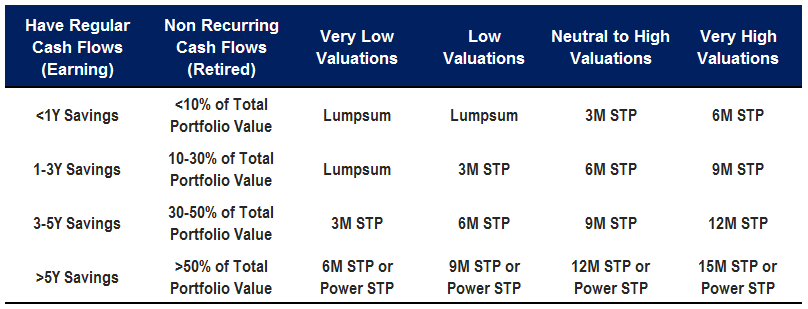

Adding Valuations to our initial framework, and combining both Rule 1 and Rule 2

Framework for Deploying New Money into Equities

Very Low valuations: 0-30, Low Valuations: 30-50, Neutral to High Valuations: 50-80, Very High Valuations: >80

As we emphasized earlier, please remember that this framework does not guarantee you the best possible entry point (as this will only be known in hindsight depending on whether the market moves up or down and for how long).

This framework’s primary intent is to help you address the issue of decision paralysis, especially when dealing with large amounts and an uncertain near term (which is nearly always the case).

Its main job is to help you minimize your future regret across different possible near-term outcomes (market going up or down) and give you peace of mind without too many “what ifs” to worry about.

Summing it up

- I have money but I am scared to invest now in equities?

- Should you invest now or wait for a market correction?

- What if you invest now and the market falls?

- What if you don’t invest now and the market continues to rally?

- What if markets correct and you are not able to enter back at the right time?

- Analysis Paralysis leading to common response – ‘I will decide later’

- Invest when you have the money – Right approach but behaviorally very difficult to implement

- While REGRET cannot be eliminated completely, it can minimized

- Rule 1: Larger the Amount, Longer the Deployment Time

- How to decide what is a ‘large’ amount?

- Retired with no future cash flows – New amount as a % of the existing portfolio

- Earning with regular cash flows – New amount represented as ‘no of years it takes to save this amount’

- Retired with no future cash flows – New amount as a % of the existing portfolio

- How to decide what is a ‘large’ amount?

- Rule 2: More Expensive the Valuation, Longer the Deployment Time

- Build an Entry Framework combining Rule 1 and Rule 2 to minimize regret and avoid decision paralysis