In the last few weeks, Indian equity markets have recovered (up around 7-8%) and are close to their previous all-time high levels.

When markets reach all-time highs, it’s normal to feel uneasy and think they might drop.

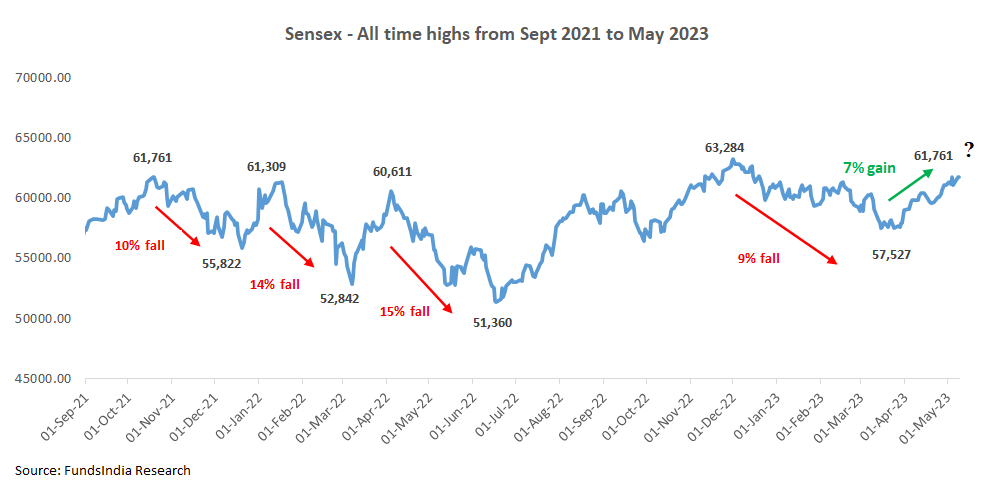

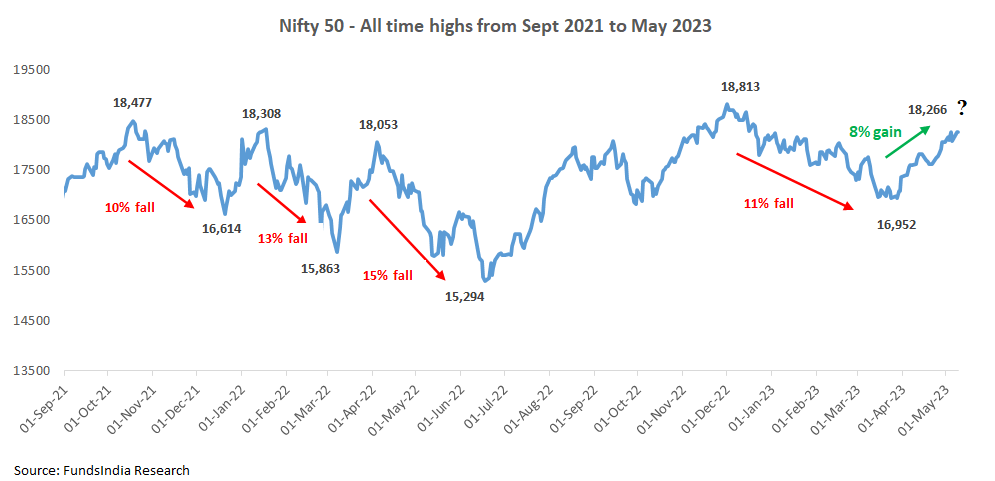

To add to this unease, you may also remember that the last few times Sensex and Nifty breached the 60,000 or 18,000 levels respectively, the markets fell 10-15%.

So it is natural to worry that the same pattern might repeat and markets will fall again.

Here comes the dilemma…

- What if you decide to reduce equities but the market breaks out and rallies to hit a new all time high?

- What if you don’t reduce equities and the market corrects similar to the last five times it fell after coming close to all time high levels?

How do we solve for this?

Insight 1: All-time highs are a normal and inevitable part of long-term equity investing. Without all-time highs, markets cannot grow and generate returns

For any asset class that is expected to grow over the long run, it is inevitable that there will be several all-time highs during the journey as seen below.

If you expect Indian equities to grow at say 12% per annum (in line with your earnings growth expectation), then mathematically it means the index will roughly double in the next 6 years, become 4X in the next 12 years, and 10X in the next 20 years.

In other words, the index will inevitably have to hit and surpass several all-time highs over time if it has to grow as per your expectation.

So there’s nothing special or frightening about all-time highs.

Insight 2: Equity Markets tend to break out and rally sharply after a few repeated patterns of “all-time highs followed by a fall” to reach higher all-time highs.

Similar to today, there have been frequent phases in the past where the Indian stock market gets stuck in a range for a while and tends to fall every time it hits an all-time high.

During such phases a lot of investors get frustrated and start to assume that every all-time high will lead to a market decline. But that’s not always the case.

Over time, however, after a period of stagnation the market eventually breaks out, surpasses the previous levels, continues to grow, and reaches a new all-time high.

Let us see how this works…

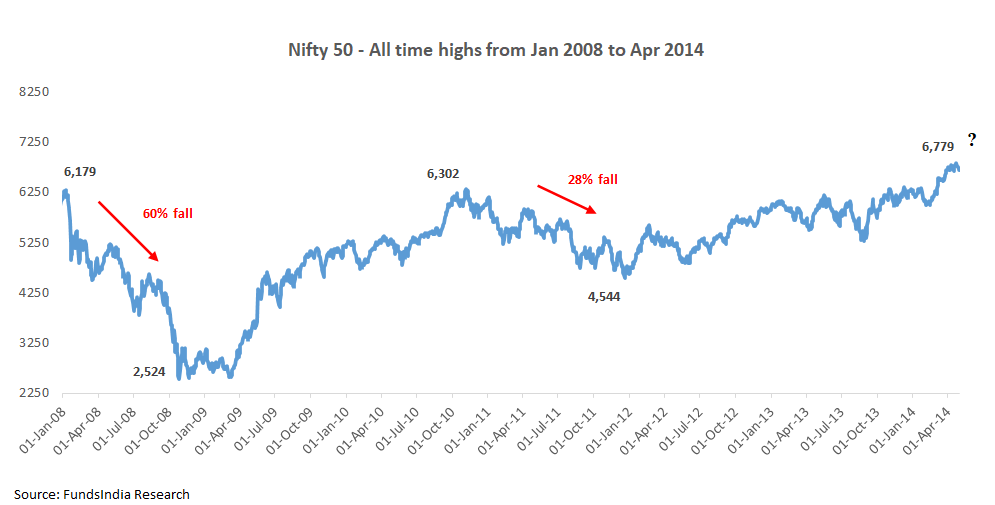

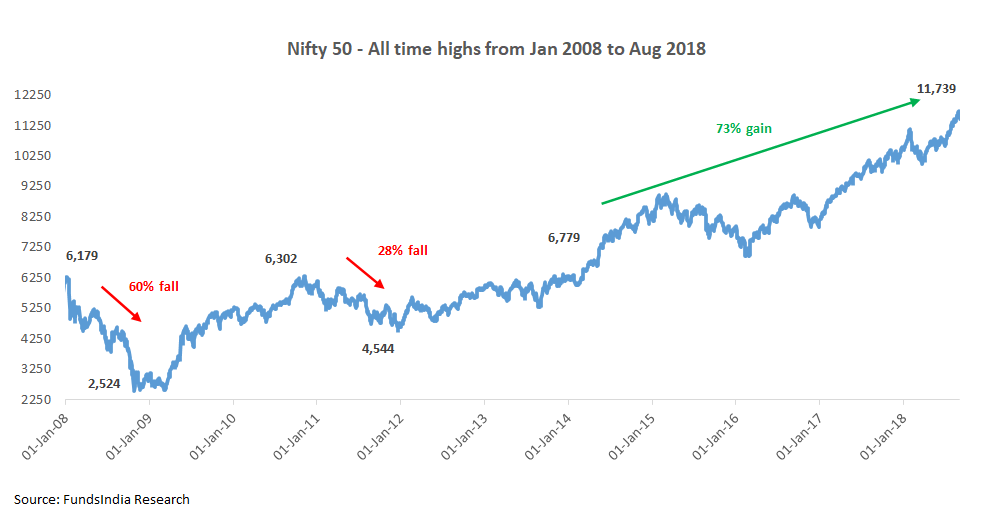

Flashback 1: Between 2008 and 2011, Nifty 50 was stuck at 6,000 levels for some time…

As seen above, the Nifty 50 between 2008 and 2010 hit all-time high levels around 6,000 levels two times in Jan-08 and Nov-10.

In both instances, Nifty 50 fell 60% and 28% after that.

Again in 2014, the market hit all-time high levels, and a lot of investors were already scarred by what happened in the previous two instances and assumed this would lead to another large fall.

… and then came the surprise – Nifty went up by a whopping 73% and went on to hit new all-time highs!

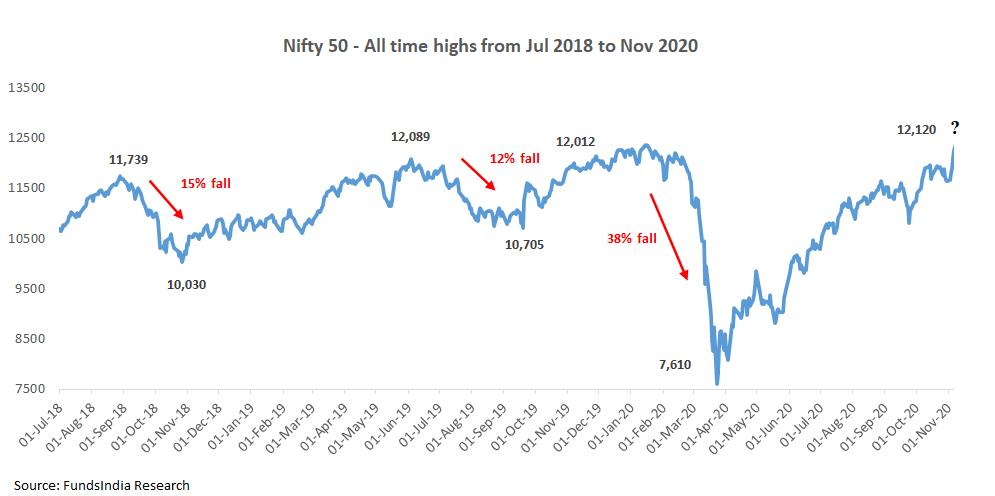

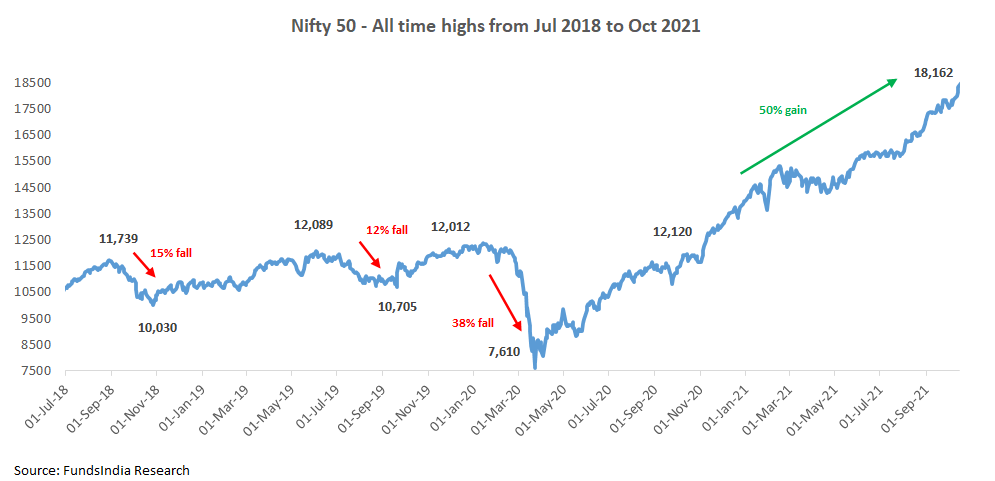

Flashback 2: Between 2018 and 2020, Nifty 50 was stuck at 12,000 levels for some time…

As seen above, the Nifty 50 between 2018 and 2020 hit all-time high levels (around 12,000 levels) three times in Aug-18, Jun-19, and Nov-19. In these instances, Nifty 50 fell 15%, 12% and 38% after that.

…and then came the surprise – Nifty went up by a whopping 50% and went on to hit new all-time highs!

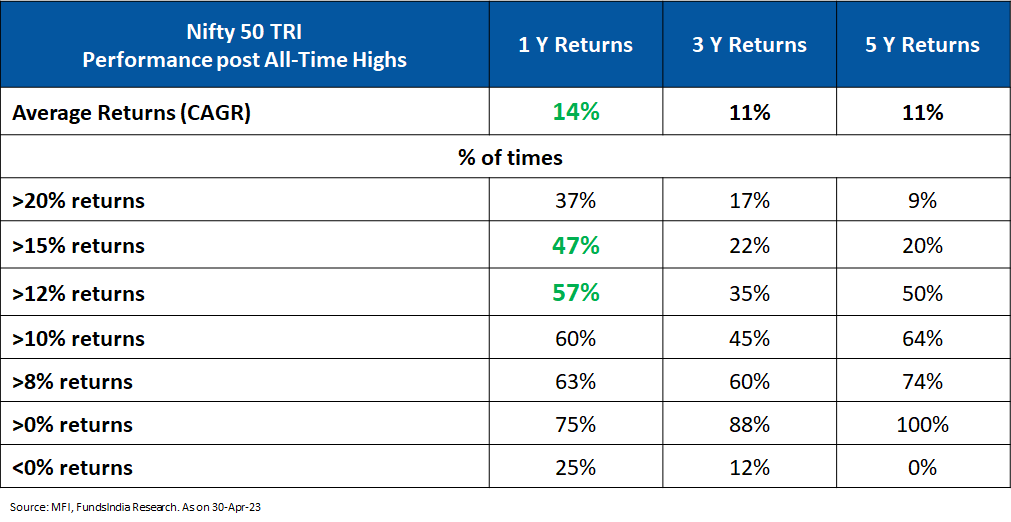

Insight 3: All-time highs have generally been followed by positive 1Y returns

For the last 23+ years, we checked for all the periods where Nifty 50 TRI hit an “all-time high”. We then checked the 1-year, 3-year, and 5-year returns following those “all-time high” levels.

The Nifty 50 TRI gave positive returns 100% of the time on a 5-year basis if we had invested during an all-time high.

The average 1Y returns, when invested in Nifty 50 TRI during an all-time high, is ~14%! (This gets even better for active funds with 20Y+ existence – HDFC Flexi cap fund and Franklin Flexicap fund – the average 1Y returns were much higher at 17% and 21%)

For Nifty 50 TRI,

- 47% of all-time highs were followed by 1-year returns of more than 15%

- 57% of the times – the 1Y returns exceeded 12%

This clearly shows that “all-time highs” automatically don’t imply a market fall and in fact, the majority of times, market returns have been strong post an all-time high.

Putting all this together

All-time highs in isolation do not predict market falls and historically investing at all-time highs has led to good short-term return outcomes the majority of the time!

While there’s no way of knowing what lies ahead in the near term, history shows us that equity markets tend to move higher over the long term. New highs are a normal occurrence and don’t necessarily warn of an impending correction. They may in fact signal that further growth lies ahead.

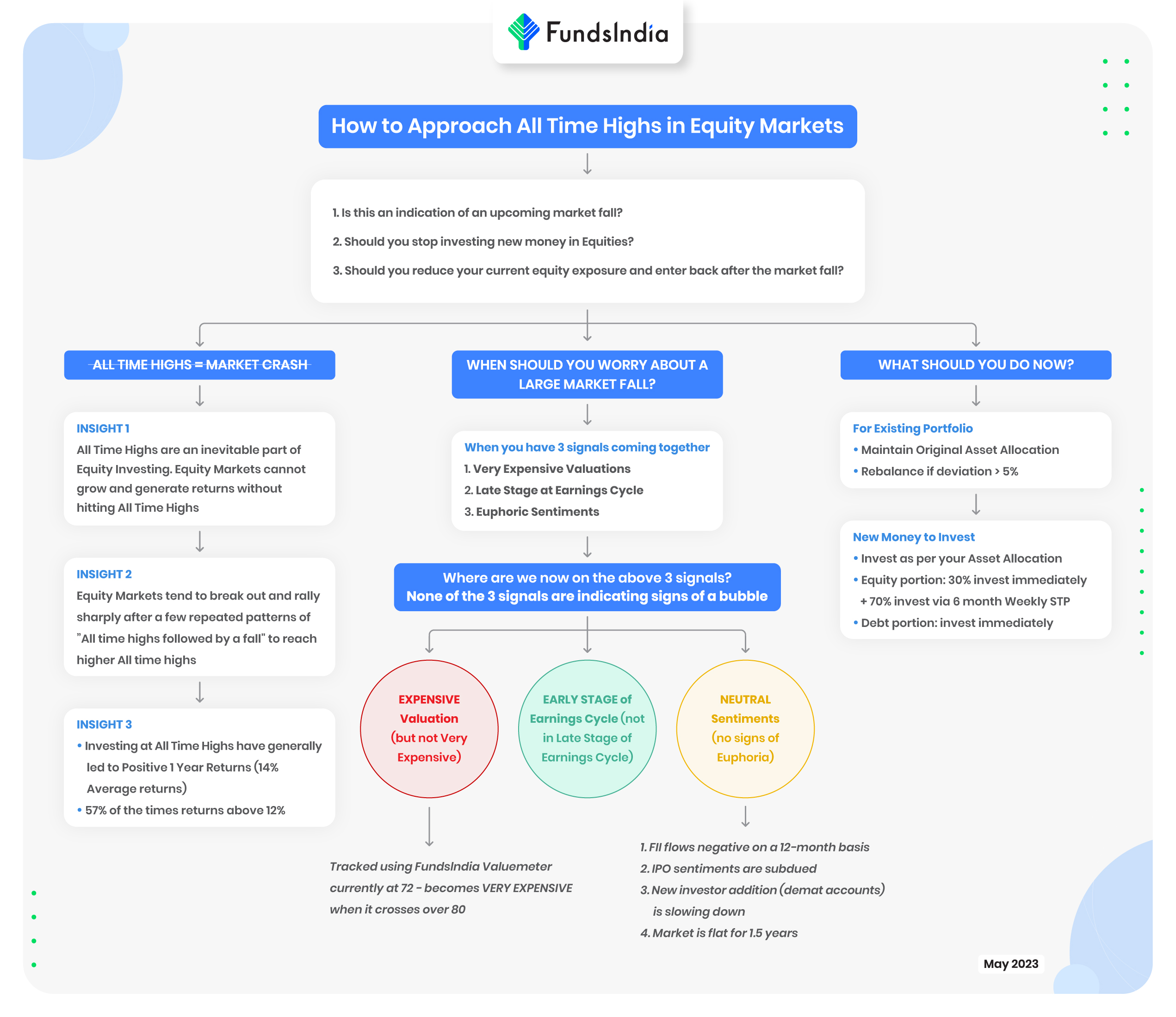

Rather than focusing on “All Time Highs,” what should you pay attention to?

Irrespective of whether the markets are at an all-time high or not, if the following three conditions occur together, then you should worry about a possible bubble (high risk) in the markets and re-evaluate your equity exposure.

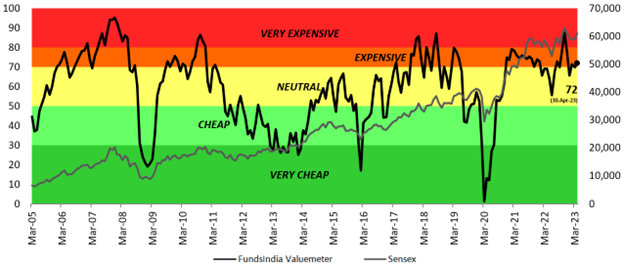

Condition 1: Very Expensive Valuations (tracked via FundsIndia Valuemeter)

Condition 2: Late Phase of the Earnings Cycle

Condition 3: Euphoric Sentiments in the Market

(Strong Inflows from FII & DIIs, large no of IPOs, leverage, new investor participation, very high past returns, new themes collecting large money, momentum, etc)

We continuously track the above via our Three Signal Framework and Bubble Zone Indicator (which tracks 30+ indicators).

Evaluating the three above conditions, where do we stand now?

No usual signs of a market bubble as we are in

- Expensive Valuations (but not in ‘very expensive’ valuations phase)

- Early Phase of Earnings Cycle (and not ‘late phase’)

- Neutral Sentiments (no signs of ‘euphoria’)

This implies the odds of the current all time high leading to a large market fall is very low and we don’t need to worry.

So, what should you do now in your portfolio?

- Maintain your original split between Equity and Debt exposure

- If your Original Long Term Asset Allocation split is for eg 70% Equity & 30% Debt, continue with the same (do not increase or reduce equity allocation)

- Rebalance Equity allocation if it deviates by more than 5% from the original allocation, i.e. move some money from equity to debt (or vice versa) and bring it back to the original asset allocation split

- Continue with your existing SIPs

- If you are waiting to invest new money

- Debt Allocation: Invest now

- Equity Allocation: Invest 30% now and Stagger the remaining 70% via 6 Months Weekly STP

An overview of how to deal with such all time highs can be found in the flowchart below

Annexure:

You can find a quick rationale for our Equity view base on our Three Signal Framework below:

- Valuation: ‘EXPENSIVE’ Valuations

Our in-house valuation indicator FI Valuemeter based on MCAP/GDP, Price to Earnings Ratio, Price To Book ratio, and Bond Yield to Earnings Yield indicates the value of 72 i.e. Expensive Zone (as of 30-Apr-2023).

- Earnings Growth Cycle: Early Phase of Earnings Cycle – Expect Strong Earnings Growth over the next 3-5 years

This expectation is led by Manufacturing Revival, Banks – Improving Asset Quality & pickup in loan growth, Revival in Real Estate, Government’s focus on Infra spending (which continues in FY24), Early signs of Corporate Capex, Structural Demand for Tech services, Structural Domestic Consumption Story, Consolidation of Market Share for Market Leaders, Strong Corporate Balance Sheets (led by Deleveraging) and Govt Reforms (Lower corporate tax, Labour Reforms, PLI) etc.

Early signs of a sharp pick-up in earnings growth are already visible since FY20.

- Sentiment: ‘NEUTRAL’

This is a contrarian indicator and we become positive when sentiments are pessimistic and vice versa.

Early signs of FIIs coming back to Indian Equities after a prolonged period of selling. Between Mar-23 & Apr-23, foreign investors invested over Rs 19,000 crs in Indian Equities.

DII flows continue to be strong. DII Flows have a structural tailwind in the form of – Savings moving from Physical to Financial assets, Emerging SIP investment culture and EPFO equity investments.

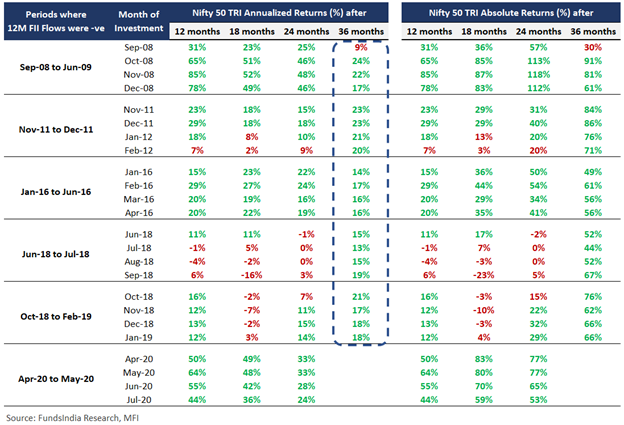

Both FII & DII flows being very high would be a concern. Despite the FII inflows in recent months, the 12M FII flows are still negative as on 30-Apr-2023 (nowhere close to being very high).

Negative FII 12M flows have historically been followed by strong equity returns over the next 2-3 years (as FII flows eventually come back in the subsequent periods). In the table below we can see the Nifty 50 TRI annualised returns for 2-3 years period after every period of FII negative flow.

To read in detail about how we derive our equity view, please refer to our monthly reports – FundsIndia Viewpoint and Bubble Zone Indicator.