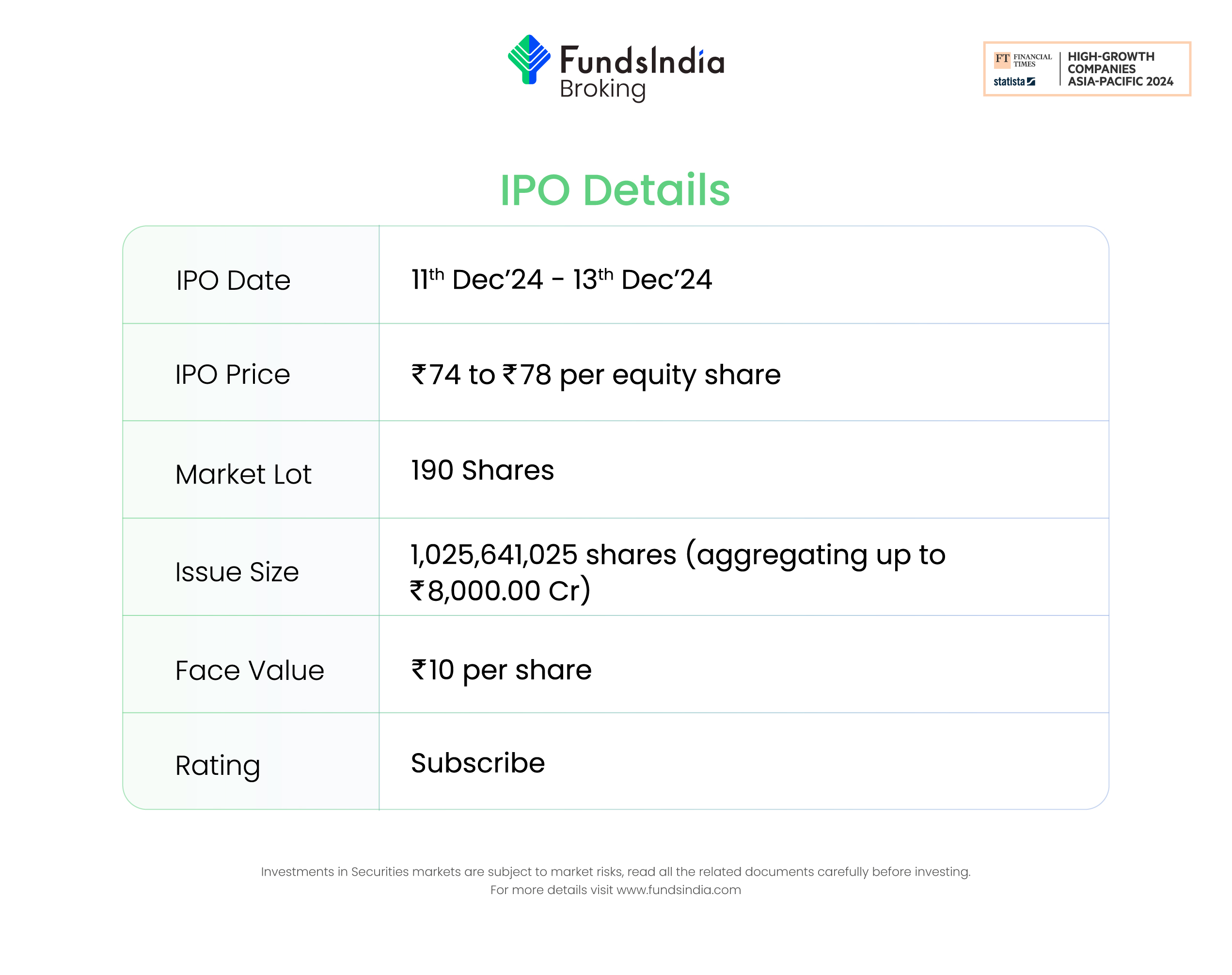

Company overview

Incorporated in 2001 and headquartered in Gurugram, Vishal Mega Mart is a hypermarket chain that sells a wide range of products like apparel, groceries, electronics, and home essentials through its portfolio of own brands and third-party brands. The company sells its products though a pan-India network of 645 Vishal Mega Mart stores (30 September 2024) and Vishal Mega Mart mobile application and website across three major product categories – apparel, general merchandise and FMCG. As of 30 September 2024, it has presence in 414 cities in 28 states and two union territories. The company was ranked as one of the top two offline-first diversified retailers in India.

Objects of the offer

- To achieve the benefits of listing the Equity Shares on Stock Exchanges.

- Carry out the offer for sale of equity shares aggregating Rs.80,000 million by the Promoter Selling Shareholder.

Investment Rationale

- Focus on middle and lower income population – The company primarily caters to the large and growing middle and lower-income segments of the Indian population. It operates an extensive network of stores in Tier 2 cities and beyond. With increasing access to digital channels, consumers in these regions are becoming more exposed to new products and services, which drives demand and opens new retail opportunities as they seek to adopt higher-tier urban lifestyles. The company offers a broad range of products under both its own and third-party brands. It stands out among offline-first diversified retailers by providing a well-rounded mix of merchandise that meets the needs of middle and lower-income consumers. Its product range spans various price points, including apparel and a variety of items such as dresses, jeans, t-shirts, shirts, bedsheets, spin mops, casseroles, pet bottles, butter cookies, savory snacks (like navratan namkeen), sanitary napkins, oats, fruit juice, noodles, and more.

- Diversified portfolio and geographical footprint – The company offers a broad portfolio of its own brands across various categories, including apparel for men, women, children, and infants, as well as household goods, home furnishings, travel accessories, kitchen appliances, utensils, crockery, footwear, and lifestyle products within the general merchandise category. In the fast-moving consumer goods (FMCG) sector, the company provides food products, non-food items, and staples. In FY24, 19 of its own brands achieved sales exceeding Rs.1,000 million each, with six brands surpassing Rs.5,000 million each in sales. The company’s revenue from the sale of its own brands grew at a compound annual growth rate (CAGR) of 27.72% between FY22-24. Over the past three years, the company has significantly enhanced its product offerings in the non-apparel segment, introducing items such as air fryers, garment steamers, egg boilers, beard trimmers, juicers, sound bars, travel speakers, induction cooktops, vegetable choppers, peanut butter, cashew almond cookies, fruit and nut cookies, chips, hair oil, and biscuits, among others. As of March 31, 2024, the company ranks second among the leading offline-first diversified retailers in India, based on the number of cities it operates in.

- Financial track record – The company reported a revenue of Rs.8,954 crore in FY24 against Rs.7,619 crore in FY23, a growth of 18%. The revenue has grown at a CAGR of 26% between FY22-24. The EBITDA of the company in FY24 is at Rs.1,429 crore, a 40% YoY growth compared to Rs.1,021 crore of FY23. The net profit of the company in FY24 is Rs.462 crore. The net profit increased by 44% compared to Rs.321 crore in FY23. The CAGR between FY22-24 of EBITDA is 33% and PAT is 51%.

Key risks

- OFS Risk – The IPO consists of only an Offer for Sale of Equity Shares worth up to Rs.80,000 million by the Selling Shareholders, including the company Promoter. The entire proceeds from the Offer for Sale will be paid to the Selling Shareholders, including Promoter and the Company will not receive any such proceeds. The offer comprises the sale of stake worth Rs.80,000 million by promoter Samayat Services LLP.

- Dependence on third party vendors – The company does not have any in-house manufacturing facilities and depends on third party vendors for the manufacture of all the products under its own brand. Any inability by the third party vendors in meeting the product specifications, quality, and manufacturing standards might impact the operations, cash flow and financial conditions of the business.

- Risk of strategic inertia – If the company fails to identify and effectively respond to changing consumer preferences in a timely manner, the demand for its products might decrease, impacting the market share and results of operations.

Outlook

The company has achieved consistent growth in its financial performance over the reported periods and we expect the company to continue its growth momentum. The aspirational retail market in India, fueled by consumer demand for products that combine high quality and affordability, will continue to be a key driver of the country’s retail sector where the company has suitably placed itself to capture an increasing market share. According to RHP, Avenue Supermarts Limited and Trent Limited are the only listed competitors for Vishal Mega Mart Limited. The peers are trading at an average P/E of 130.91x with the highest P/E of 163.59x and the lowest being 98.23x. At the higher price band, the listing market cap of Vishal Mega Mart will be around ~Rs.35,168 crore and the company is demanding a P/E multiple of 76.13x based on post issue diluted FY24 EPS of Rs.1.02. When compared with its peers, the issue seems to be fully priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.