Company overview

Bharti Hexacom Ltd. is a communications solutions provider offering consumer mobile services, fixed-line telephone and broadband services to customers in Rajasthan and the Northeast telecommunications circles, which comprises the states of Arunachal Pradesh, Manipur, Meghalaya, Mizoram, Nagaland and Tripura. The company is offering services under the brand “Airtel”. It was originally incorporated in 1995 as ‘Hexacom India Limited’. In 2004, the name was changed to ‘Bharti Hexacom Limited’ when Airtel acquired a majority equity interest in the company. As of December 31, 2023, the company has its presence in 486 census towns and has an aggregate of 27.1 million customers across both the circles. As of the same date, customer base included 19,144 thousand data customers, of which 18,839 thousand were 4G and 5G customers, and data consumption per customer per month stood at approximately 23.1 GB during the nine months ended December 31, 2023.

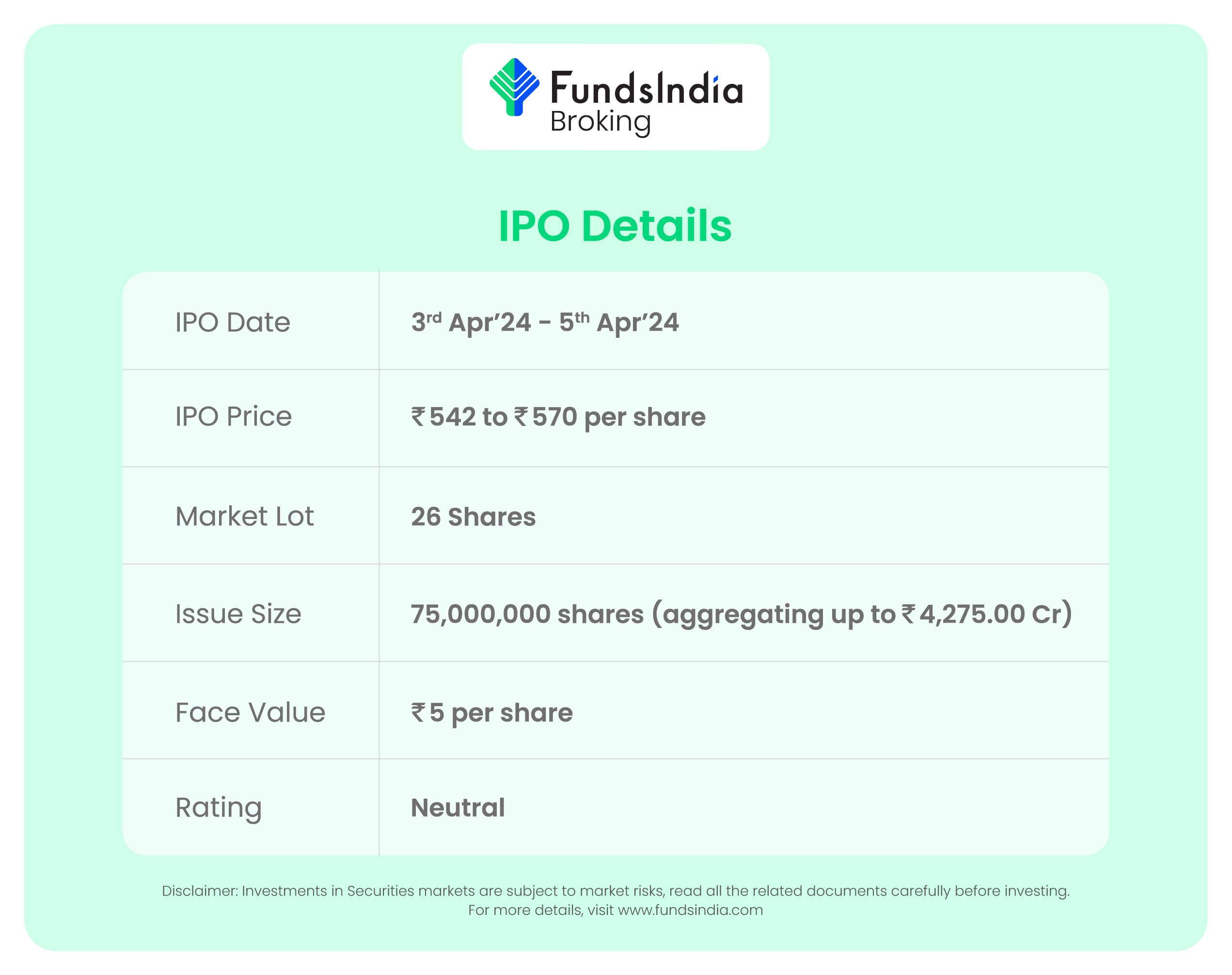

Objects of the offer

- Carry out the Offer for Sale of up to 75,000,000 Equity Shares by the Selling Shareholder.

- Achieve the benefits of listing Equity Shares on the Stock Exchanges.

Investment Rationale

- Strong parentage – The company is offering its services under the widely recognized brand “Airtel”, which owns 70% stake in the company. Airtel is a global communications solutions provider with over 500 million customers in 17 countries across South Asia and Africa. The company is deriving significant synergies from its relationship with Airtel and its affiliates, including through Indus Tower’s infrastructure, inter circle roaming arrangements, its national long-distance network and corporate functional support.

- Established position –Bharti Hexacom’s revenue market share for Rajasthan and Northeast circle was 40.4% and 52.7% respectively during nine months ended December 31, 2023, securing number one position in Northeast circle during the period. The company is consistently improving its average revenue per user (“ARPU”) for mobile services from Rs.135 for FY21 to Rs.155 for FY22 to Rs.185 for FY23 to Rs.197 for the nine months ended December 31, 2023. The company has the highest number of Visitor Location Register – VLR (used to determine the number of active users on a mobile network) customers (6.4 million) and a VLR market share of 52.3% in the Northeast circle and the second highest in the Rajasthan circle with 23.2 million customers and a VLR market share of 38.7%, as of December 31, 2023.

- Presence in markets with high growth potential – The company operates in Rajasthan and Northeast circles in India which has high potential for increasing the customer base. Rajasthan’s customer base is expected to grow at 1.4% to 1.5% between FY23-28 reaching 69.0 million to 69.5 million with a teledensity of 82% to 83% following pan-India trends with rising rural teledensity. The customer base in the Northeast is expected to grow at 1% to 1.5% between FY23-28 reaching 13.2 to 13.5 million with a teledensity of 81 to 82%. Northeast circle telecom industry is expected to grow at 6% to 7% between FY23-28 to reach Rs.39 to 41 billion, supported by rising teledensity, higher internet penetration and a potential increase in ARPU in the region.

- Financial track record – The company reported a revenue of Rs.6,579 crore in FY23 as against Rs.5,405 crore in FY22, an increase of 22% YoY. The revenue has grown at a CAGR of 20% between FY2021-23. The EBITDA of the company in FY23 is at Rs.2,888 crore and EBITDA margin is at 44%. The CAGR between FY2021-23 of EBITDA is 59%. The PAT of the company in FY23 is at Rs. 549 crore and PAT margin is at 8%. The net profit declined by 67% compared to the Rs.1,675 crore of FY22. The ROCE of the company stands at 10.72% in FY23.

Key risks

- OFS risk – The IPO consists of only an Offer for Sale of up to 75,000,000 Equity Shares by the Selling Shareholders. The entire proceeds from the Offer for Sale will be paid to the Selling Shareholders and the company will not receive any such proceeds. The offer comprises the sale of 75,000,000 shares by Telecommunications Consultants India Limited.

- Geographical concentration – The company derives its revenue from providing mobile telephone services in Rajasthan and Northeast circle. The scope for growth and customer additions may be restricted by limited areas of operations. Any adverse developments in these circles might impact the company disproportionately compared to any of its competitors with pan-India presence. Challenges in setting up infrastructure facilities in these difficult terrains (especially in Northeast) and rural regions might affect the turnover.

- Regulatory risk – Reduction in revenue due to regulatory ceilings on pricing by TRAI, or owing to pricing pressure, reduction in ARPU, may have an adverse effect on the business, financial condition, results of operations and prospects.

Outlook

The services Bharti Hexacom Ltd. provides along with Airtel and its affiliates have aided the company in catering to the needs of customers and enabled the growth in market share. Compared to competitors, who may have operations across multiple circles, the company’s scope for growth and customer addition may be restricted owing to limited areas of operations in Rajasthan and Northeast. According to RHP, Bharti Airtel Limited and Vodafone Idea Limited are the only listed competitors for Bharti Hexacom Ltd. The peers are trading at an average P/E of 40.27x with the highest P/E of 82.16. Vodafone is a loss-making company and hence it is futile to compute its P/E. At the higher price band, the listing market cap of Bharti Hexacom Limited will be around Rs.28,500 crore and the company is demanding a P/E multiple of 51.89x based on post issue diluted FY23 EPS of Rs.10.98. When compared with its peers, the issue seems to be overvalued. Based on the above views, we provide a ‘Neutral’ rating for this IPO for a medium to long-term holding.