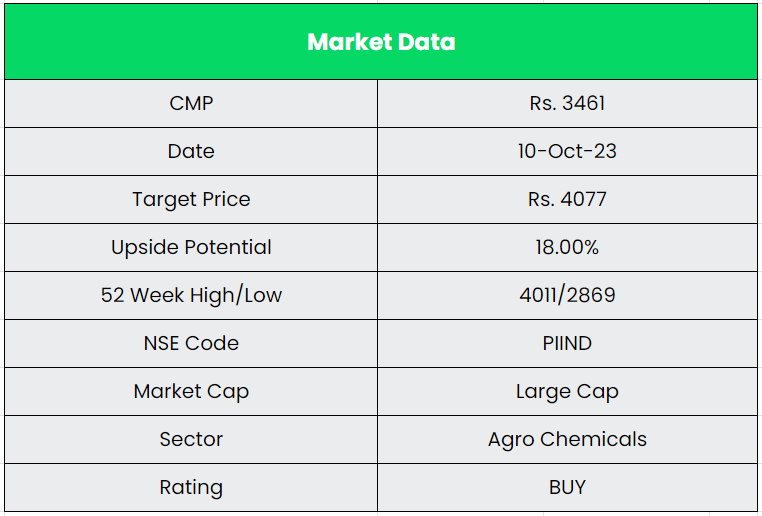

PI Industries Ltd. – Strong player in Agro-Chemicals space

PI was set up in 1946 as an edible oil refinery by the late Mr. P P Singhal. The company later entered the agrochemical formulations business. In the mid-1990s, PI diversified into Custom Synthesis and Manufacturing (CSM) exports for global agrochemical innovator companies. PI currently operates in the domestic agricultural inputs and CSM exports segments. It is a leading player in the domestic agricultural inputs sector, primarily dealing in agrochemicals and plant nutrients. In the CSM exports segment, its business interests include dealing in custom synthesis and contract manufacturing of chemicals, which constitutes techno commercial evaluation of chemical processes, process development, lab and pilot scale-up, as well as commercial production. The PI group has four integrated manufacturing facilities spread across 100+ acre land.

Products & Services:

The company has a wide range of chemical products in categories like Insecticides, Herbicides and Fungicides. It also has some products on speciality division. Apart from those, the company provides CSM (Custom Synthesis and Manufacturing Solutions) which involves from research to production.

Subsidiaries: As on FY23, the Company has 7 Wholly-owned Subsidiaries and 2 Joint Ventures.

Key Rationale:

- Established position – A presence of over five decades in the domestic agricultural inputs business, a healthy product mix, leadership in several generic product segments, and increasing number of launches through the ILCM (in-licensing and co-marketing) route have helped the group establish itself as one of the top 10 players in this space. Apart from fiscal 2020, where delayed monsoon and erratic rainfall during the year impacted sales, domestic business has witnessed steady growth over the last 5-6 fiscals led by introduction of new molecules and increased market penetration. With a solid product line up, supportive policy environment, and normal monsoon, the domestic business is expected to register healthy revenue growth over the medium term.

- Acquisition – PI Health Sciences Ltd. (PIHS) acquired Archimica S.p.A., Italy on 27th April 2023. Archimica is an Italy based, highly reputable small molecule API manufacturer and CDMO operating for last 75 years in Europe. PIHS also completed the acquisition of Therachem Research Medilab (India & US) and Solis Pharmachem (India) on 2nd June 2023. TRM (Therachem Research Medilab) is an innovative, chemistry driven solution provider in medicinal chemistry research, process research and development, specialising in the Rare Disease area. All the above acquisitions amount to Rs.856 crore.

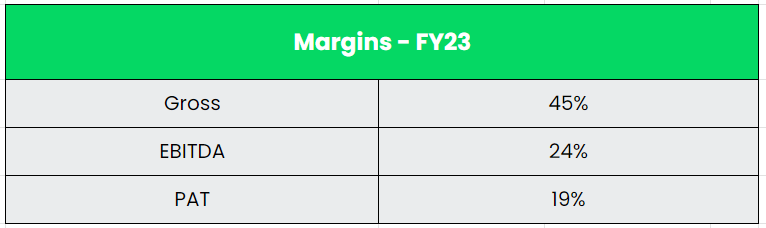

- Q1FY24 – PI Industries reported a Overall revenue growth of 24% YoY in Q1FY24 to Rs.1910 crore, supported majorly by the export revenue of Rs.1563 crore, an increase of 37% YoY. Domestic revenues were subdued due to delayed monsoon leading to volume degrowth of ~13% as focused efforts were made to achieve revenue quality and efficient working capital levels than the volumes. Gross Margin improved to 47%, an improvement of ~267 bps YoY mainly because of a better product mix and Pharma business. EBITDA reported a growth of 35% YoY to Rs.468 crore, with EBITDA margin improving by ~209 bps to 24% on account of favourable product mix and operating leverage.

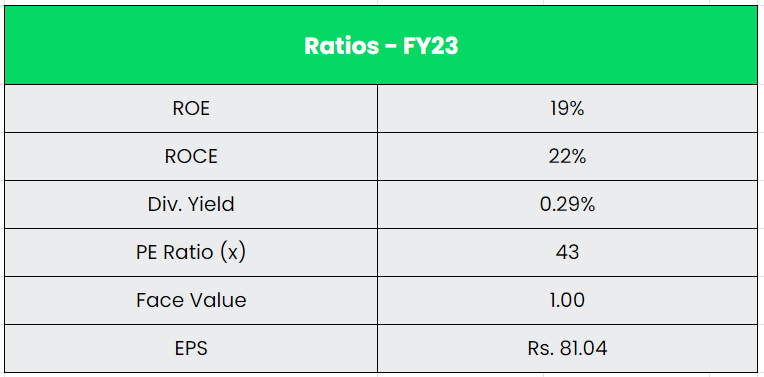

- Financial Performance – The company generated a Revenue and PAT CAGR of 23% and 28% over the period of 5 years (FY18-23). The company maintained an average EBITDA Margin of 20%+ for the past 9 years. The company’s balance sheet is strong with zero debt in its balance sheet. Average 5-year ROE and ROCE is around 17% and 22% for FY18-22 period.

Industry:

India is one of the major players in the agriculture sector worldwide and it is the primary source of livelihood for ~55% of India’s population. India has the world’s largest cattle herd (buffaloes), the largest area planted for wheat, rice, and cotton, and is the largest producer of milk, pulses, and spices in the world. According to Inc42, the Indian agricultural sector is predicted to increase to US$ 24 billion by 2025. Indian food and grocery market is the world’s sixth largest, with retail contributing 70% of the sales. India’s agricultural and processed food products exports stood at US$ 43.37 billion in FY23 (April 2022-January 2023). As per Second Advance Estimates for 2022-23 (Kharif only), total foodgrain production in the country is estimated at 153.43 million tonnes. India is one of the largest agricultural product exporters in the world. In April-December 2022, the overall value of export of agricultural products increased to US$ 19.7 billion from US$ 17.5 billion over the same period of the last fiscal.

Growth Drivers:

- The agriculture services sector has also recorded a sharp increase in investments with cumulative FDI inflow of US$ 3.02 Billion between April 2000 – March 2023.

- Initiatives like Kisan Rath (mobile app for farmers, FPOs, and traders), 200+ Kisan Rails, and Krishi Udaan Scheme for produce transportation, Perishable Cargo Centres, cold storage facilities at Airports and Inland Container Depots as well as cargo terminals and warehouses.

- Union budget 2023-24 focuses on reviving rural demand by boosting disposable income, allocation to farms and higher fund allocation on rural infrastructure, connectivity, and mobility to create long-term jobs.

Competitors: BASF India, Bayer Crop Science, etc.

Peer Analysis:

Though PI Industries P/E is higher than its peers, the level of business growth in terms of CAGR shows the potential of PI industries. BASF on the other hand generated loss in past and the Bottomline is highly volatile historically which results in an irregular growth.

Outlook:

The CSM export segment is marked by a significantly de-risked business model, which provides healthy revenue visibility and stable profitability. The PI group is one of the pioneers of CSM in the agrochemical space in India. The CSM export orderbook of the company as on Q1FY24 is around USD 1.8 bn. PI Industries remains cautiously optimistic about achieving its 18% to 20% revenue growth target for the current fiscal year. The Management is confident of getting back on the growth path in the domestic business with the normalization of rainfall during the second half of the kharif season. They also maintain the momentum of new product launches. Five innovative products are planned for this fiscal year. In Q1, the company has launched EKETSU. EKETSU is India’s first three-way herbicide mixture to provide maximum weed control and efficacy for total control in rice herbicides.

Valuation:

We believe PIIND is well-placed for future growth given the revival of domestic business and strong performing export business. Also, the recent acquisitions by the company will pave way for additional growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.4077, 37x FY25E EPS.

Risks:

- Demand related Risk – Any slowdown in crop protection chemical demand likely to impact execution of CSM business and thereby revenues.

- Monsoon Risk – The failure of the monsoon (and/or adverse climatic conditions) coming on top of the COVID-19 related setback could put pressure on demand for farm inputs for the forthcoming Kharif season.

- Working Capital Risk – The agrochemical industry is characterised by working capital-intensive operations, due to large inventory requirement, seasonality in demand, and extended credit to dealers and distributors.