KPIT Technologies Ltd – Shaping the future of mobility

Founded in 2018 and based in Pune, KPIT Technologies Ltd. is a leading software and system integration partner for the global mobility ecosystem. The company is a trusted collaborator for major automotive industry leaders, having established over 25 strategic partnerships with Original Equipment Manufacturers (OEMs) and Tier 1 suppliers to drive mobility transformation. KPIT’s strategy focuses on building deep, long-term relationships with select mobility OEMs. It has established enduring partnerships with key players like Honda, Renault, BMW, PACCAR, Navistar, Stellantis, Jaguar, Volkswagen, and Mercedes-Benz. As of FY24, the company boasts a network of 30 centres of excellence, 700+ production programs, 75+ platforms and tools that caters to 25+ OEMs/ Tier1 strategic partners.

Products and Services

The products services offered by the company finds domain application in vehicle engineering and design, E/E architecture, network and middleware, software and system integration, virtual engineering, autonomous driving and Advanced Driver Assistance System (ADAS), body electronics, chassis, cockpit, propulsion etc.

Subsidiaries: As of FY24, the company has 22 subsidiaries and one associate company.

Investment Rationale

- Expanding order book – The company secured several notable new deals in Q2FY25. A prominent European car manufacturer has chosen KPIT for multiple strategic projects in autonomous, middleware, and diagnostics areas. Additionally, another European car manufacturer has entered strategic engagements with the company in the body electronics, connected, and electric powertrain domains. In the United States, the company has won two new deals – one with a leading car manufacturer in the electric powertrain and connected domains, and another with a commercial vehicle manufacturer in the connected, middleware, and powertrain sectors. Furthermore, the company has secured a major deal with a leading Asian car manufacturer in the autonomous and powertrain domains.

- Growth strategies – Diversifying from its traditional passenger cars segment, KPIT is aiming to expand its offerings capitalising on the software integration opportunities in off-highway and commercial vehicles (CV) segment. The company is committed to double its CV client base. It also has plans to develop capabilities to apply its expertise in other segments such as marine, railways, aviation and space. KPIT partnered with ZF Group, a global technology company supplying advanced mobility products and systems, to promote QORIX (a subsidiary of KPIT) as an independent company with a focus on developing world class automotive middleware stack. Building on its value-added services, the company has acquired 26% stake (with an option to further increase the stake) in Swiss based N-Dream AG, an early mover in cloud-based gaming aggregation platform.

- Q2FY25 – During the quarter, the company generated a revenue of Rs.1,471 crore, an increase of 23% compared to the Rs.1,199 crore of Q2FY24. This growth was driven by the Asia region and the middleware and powertrain segments. EBITDA improved by 28% from Rs.240 crore of Q2FY24 to Rs.306 crore of Q2FY25. Net profit stood at Rs.204 crore, which is an increase of 45% from Rs.141 crore of the corresponding period in previous year. Total contract value of new deals won in Q2FY25 stood at $ 207 million, with new deals coming from Europe, USA and Asia. The company has one of the lowest levels of attrition in the industry.

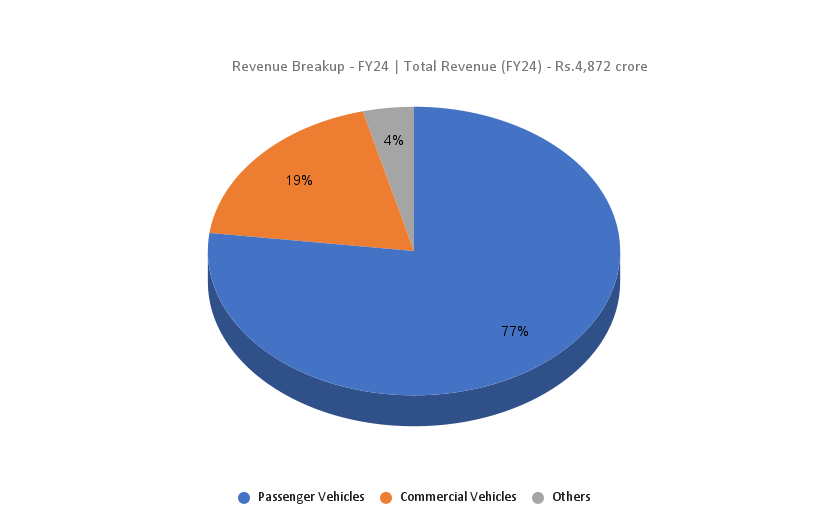

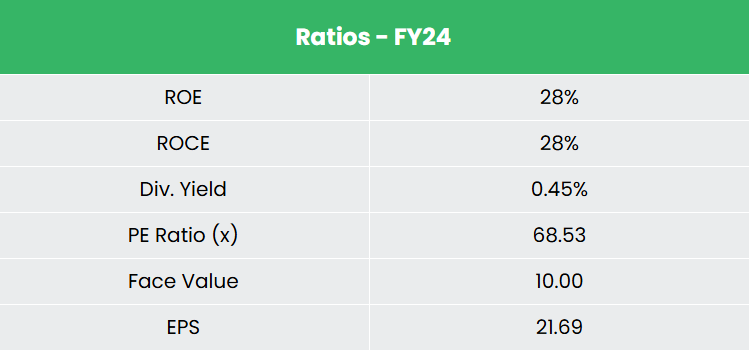

- FY24 – KPIT generated revenue of Rs.4,872 crore, an increase of 45% compared to FY23 revenue. Operating profit is at Rs.991 crore, up by 56% YoY. The company posted net profit of Rs.595 crore, an increase of 56% YoY.

- Financial performance – The company has generated revenue and PAT CAGR of 34% and 61% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 27% and 31% for FY 21-24 period. The company has a robust capital structure with a debt-to-equity ratio of 0.14.

Industry

The Indian automobile industry has long been a reliable gauge of the economy’s health, given its significant role in both macroeconomic growth and technological progress. The sector is expanding, fuelled by strong foreign direct investment (FDI), rising exports, and eco-friendly initiatives, making it an attractive investment opportunity for global stakeholders. The growing middle-class income and a large youth population are driving demand for greater sophistication in the automotive market. This has resulted in the industry undergoing a transition from traditional hardware to software-defined vehicle (SDV) architectures, which is opening new revenue streams for mobility OEMs and is expected to enhance cost-efficiency, speed up feature deployment, and improve consumer experiences. Additionally, investments in AI are transforming various facets of vehicle production, performance, and user interaction.

Growth Drivers

- Government initiatives Automotive Mission Plan 2026, scrappage policy, production-linked incentive scheme are expected to drive the market.

- 100% FDI allowed under automatic route in the automobile sector.

- In March 2024, The Cabinet approved an allocation of over Rs. 10,300 crore (US$ 1.2 billion) for the IndiaAI Mission, marking a significant step towards bolstering India’s AI ecosystem.

Peer Analysis

Competitors: Tata Technologies Ltd, Coforge Ltd etc.

When compared to its peers, KPIT offers a reasonable price relative to its sales growth and margin expansion potential. It is also generating better returns from the invested capital, indicating optimum utilisation of funds.

Outlook

The company has provided a cautious revenue forecast, projecting a growth range of 18-20% on the lower end, due to possible delays in project commencements by clients. However, it has increased its profit growth forecast, now anticipating a rise of 0.2 to 0.3 percentage points above the previous estimate of 20.5%. The company plans to boost profitability by securing more fixed-price projects. Management is also focusing on strategic partnerships and potential acquisitions to strengthen its market position. Leveraging its expertise in emerging technologies, along with deep client relationships and trusted partnerships, has led to significant deal wins. In addition to acquiring new deals from the existing clients, the company is in discussions with new clients from Europe and America to build long-term large engagements.

Valuation

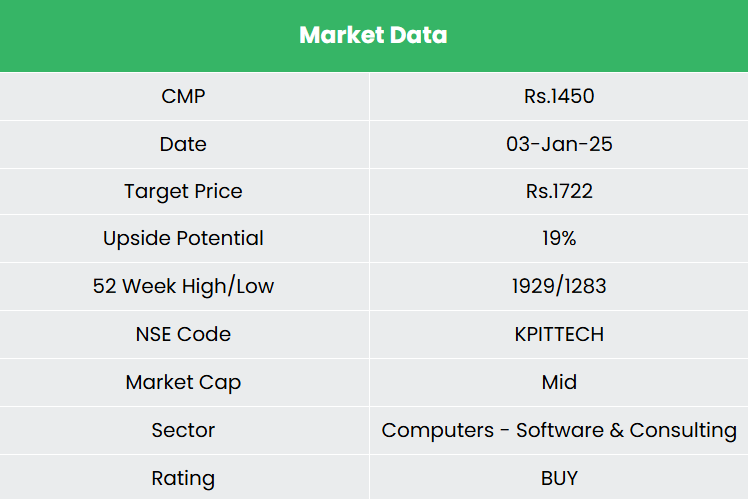

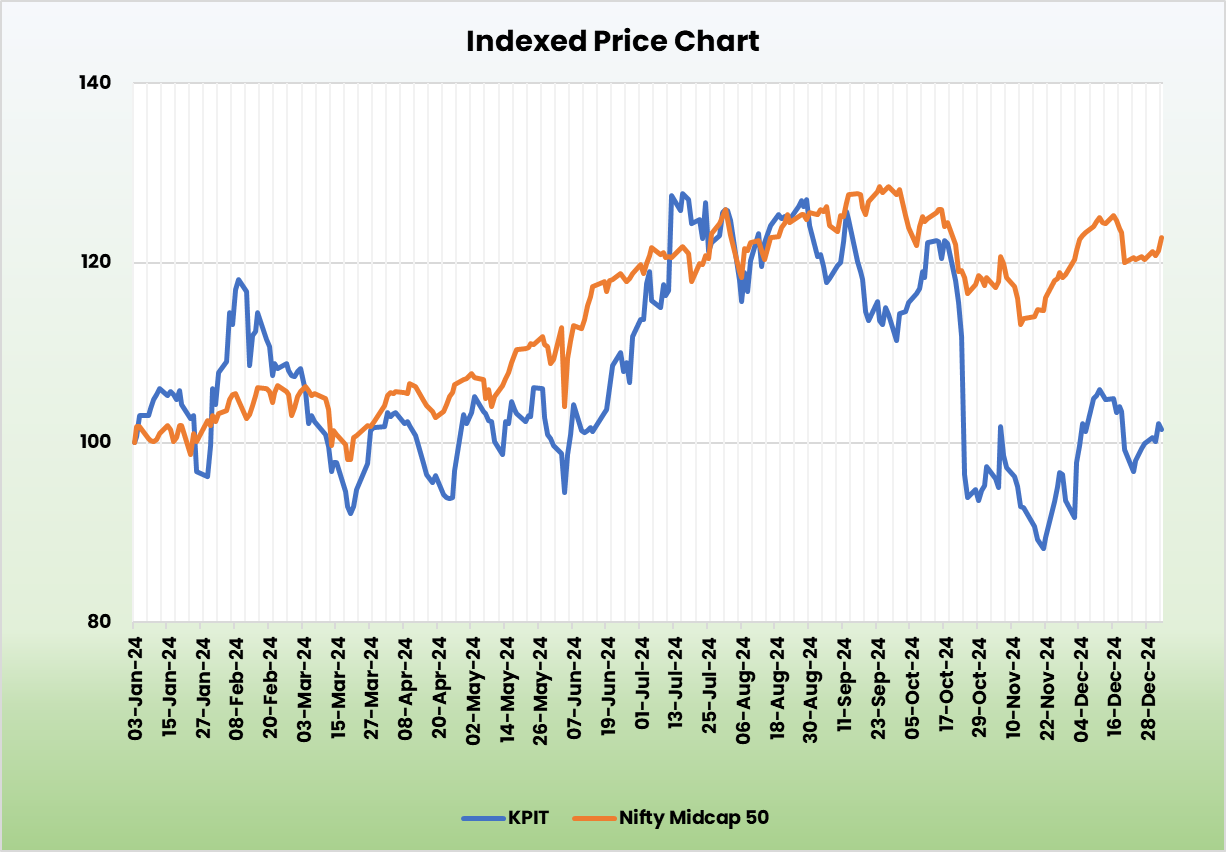

We expect the company to sustain its growth momentum backed by large deal wins and its proven execution capabilities. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,722, 51x FY26E EPS.

Risk

- Deal delays – The company’s turnover might get impacted when there is any delay in new project launch by clients.

- Forex risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

Note: Please note that this is not a recommendation and is intended only for educational purposes. So, kindly consult your financial advisor before investing.

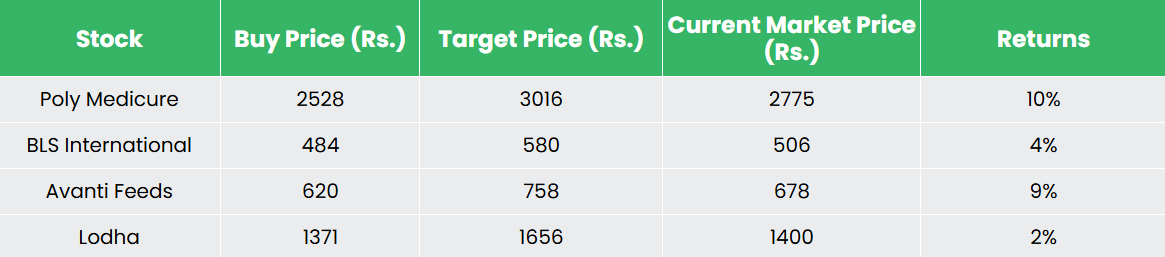

Recap of our previous recommendations (As on 03 January 2024)

BLS International Services Ltd