Britannia Industries Ltd. – Eat Healthy; Invest Better!

Established in Kolkata, Britannia is a household name in India, and one of the country’s leading food products companies. Britannia Industries ltd. (BIL) belongs to the Wadia Group, a reputed Indian Business house who has presence in wide range of business segments like Airlines (Go Air), Realty (Bombay Realty), Textiles (Bombay Dyeing) and Plantations and other business (Bombay Burmah trading Corporation). With a 120-year legacy, it started its operations in 1892 when a group of businessmen in Kolkata, formed a company to manufacture biscuits.

Over the years, the company has diversified into other segments like bread, dairy products, cakes, snacks, milk shakes, etc. BIL has 10 manufacturing plants across the country. In addition to manufacturing at its own plants, the company has established relationships with several contract manufacturers across the country. It also supplies its products to various export markets and has a manufacturing footprint in Oman, Dubai, and Nepal outside India.

Products & Services:

Britannia’s product portfolio includes Biscuits, Bread, Cakes, Rusk, and Dairy products including Cheese, Beverages, Milk and Yoghurt.

Biscuits – Country’s famous brands like Good day, Tiger, Jim-Jam, 50-50, Marie-Gold, Nutri Choice, Milk Bikis, Bourbon, etc.

Dairy – Come Alive Paneer and curd, Cheese, ghee, Winkin’ cow, etc.

Others – Wafers, salted snacks, and Croissant under snacking category; Layerz, Roll yo, Gobbles, etc. under cakes category; Tostea under rusk; Gourmet, white and wheat breads under bread category.

Subsidiaries: As on FY22, the company has 25 Subsidiaries and 2 Associate companies.

Key Rationale:

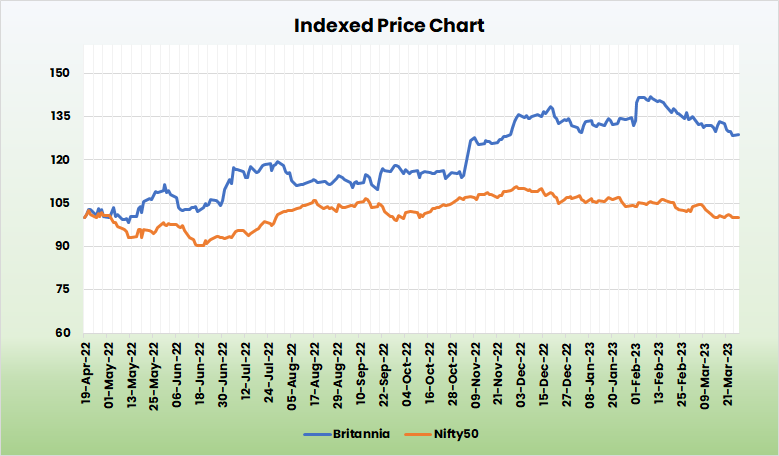

- Leading Market position – BIL has an established market position in the Indian biscuits industry with a market-leading presence across categories like cookies, Marie and milk biscuits supported by strong brands such as Good Day, Marie Gold, Tiger, Milk Bikis and NutriChoice. This has helped the company to improve its market share steadily over the last few years. In addition to biscuits, BIL has a healthy market position in the cake, rusk, bread, and cream wafers segments, further supporting its business prospects. The direct reach of the company has improved from 24.9 lakh outlets at the end of Mar’22 to 26.4 lakh outlets at the end of Dec’22 by adding ~1.5 lakh outlets in the 9MFY23. The rural distribution stands at 28K dealers as of Dec’22. The rural division is important for BIL as the market share gained in the rural India is 1.5x of the market share gained in overall India.

- New Launches – BIL launched Biscafe and Nutri Choice – seeds, herbs, and protein in Q1FY23, which have grown 5x and 4x in Q3FY23. Moreover, 50-50 Golmaal has been extended to Bihar, Jharkhand, and Orissa, registering a growth of 2x. Croissants (up 150%) and Marble Cake (up 130%) as the company scaled them up in other markets and channels. The newly launched products in Q3FY23 are Plum Cake (East and South); Tic Tac Toe snacking (South) and Paneer (West).

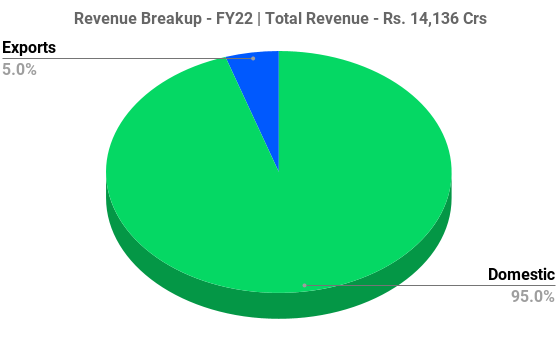

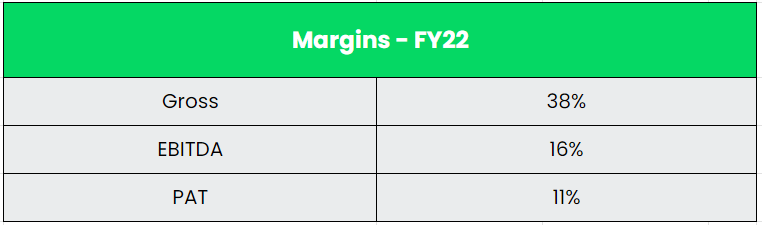

- Q3FY23 – During Q3FY23, the revenue grew 17% YoY to Rs.4197 crs. The EBITDA for Q3FY23 grew by 52% YoY to Rs.818 crs. The company reported a consolidated gross margin of 44% which is the highest ever in the last 13 quarters. The decline in the input prices such as palm oil, etc. and forward wheat contracts are the main reason for the improvement in the Gross margin. The company also normalised its ad spends in Q3FY23 and it is back to pre-covid levels. International business is showing healthy, profitable growth across geographies. The company commercialised own operations in Kenya during the quarter. The share of Biscuits and Non-biscuits portfolio is currently at 77:23. Of the 23% of Non biscuits portfolio, 50% caters to Rusk and Cakes.

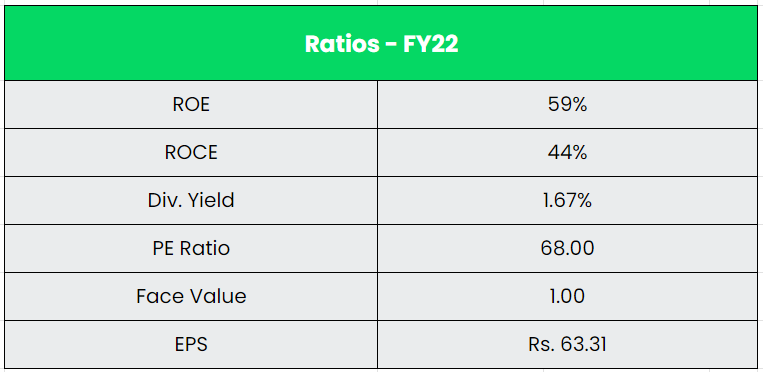

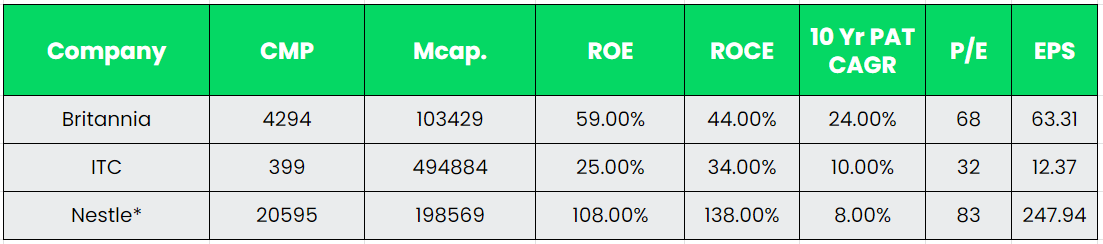

- Financial Performance – The company has a Revenue and PAT CAGR of 10% and 24% for the period of 10 years between FY12-22. The 5Yr average ROE stands at 40% and the 5Yr average ROCE stands at 41%. The company has generated Rs.1000+ crs of Operating cashflow for the consecutive fifth year. The company’s debt stood at Rs.2480 crs as on FY22 with a debt-to-equity ratio of 0.9x.

Industry:

The Indian food processing industry is among the largest in the nation in terms of growth, production, consumption, and exports. Biscuits is the largest category in the food business in India. It is present in the consumption basket of virtually every Indian family as an essential product. It is one of the most deeply penetrated categories in the country, reaching over 90% of the households. Indian food processing market size reached US$ 307.2 trillion in 2022 and is expected to reach US$ 547.3 trillion by 2028, exhibiting a growth rate (CAGR) of 9.5% during 2023-2028. India ranks 1st in Milk production and the total milk production in the country during 2021-22 is 221.06 Mn tonnes. In the year 2021-22, the milk production has registered an annual growth rate of 5.29%.Organized dairy segment, which constitutes about 26%-30% of the Indian dairy industry (by value) has seen faster growth compared to the unorganized segment. The Indian online grocery market size has been projected to grow from US$ 4,540 million in 2022 to US$ 76,761.0 million by 2032, at a CAGR of 32.7% through 2032.

Growth Drivers:

- The per capita consumption of biscuits in India is relatively low at 2 kgs versus 10 kgs in certain developed countries. The low per capita consumption and high levels of penetration continue to provide excellent opportunities to increase consumption through proactive interventions and strategies.

- The Total FDI received in the food processing sector from April 2000 till December 2022 was $11.79 Bn. The FDI equity inflow in the Food Processing Sector for the period of April 2021- March 2022 was US$ 709.72 Million.

- The Union Government approved PLI scheme worth Rs.10,900 crs for food processing sector. Britannia, Parle, ITC, Haldiram foods, HUL, etc. are the companies that have been approved by the Government under ready to eat and ready to cook segment.

Competitors: Nestle India & ITC Ltd.

Peer Analysis:

No listed company is a direct full-fledged competitor for Britannia Industries. ITC is generating only ~23% of their overall revenues from FMCG sector which includes packaged foods, personal care, stationary, apparels and agarbattis. Nestle being a complete FMCG company is generating half of their overall revenue from milk and nutrition products. The rest of revenue is more into chocolates, cooking aids and confectionery and not in bakery or biscuit products.

*For Nestle, we took CY22 data for comparison.

Outlook:

The Retail inflation metric, CPI (Consumer Price Index) of India fall drastically to 5.66% in March 2023 from 6.44% in February 2023. The main cause of the fall in the CPI is due to the fall in food inflation from 5.95% in February 2023 to 4.79% in March 2023. The fall in the prices will result in a positive impact in the near-term margins of the company. Despite taking prices hikes, the company continued to gain market share for the 39th consecutive quarter. In Q3FY23, the company entered a Joint venture with a French company named Bel to develop the fast-growing cheese category in India. The JV will be produced in the new facility at Ranjangaon. Britannia holds 51% stake while Bel holds 49% stake in the JV. Bel is a world leader in the branded cheese category with international brands named Laughing cow, baybel, etc. The JV now has a co-branded product named “Britannia the laughing cow.” The cheddar cheese lines at Ranjangaon will commercialize in Q1FY24E and the processed cheese lines in H2FY24E. BIL will continue to import the Rs.10 sachet of cheese that Bel sells currently from Vietnam as India has a no import duty treaty with Vietnam. At the Ranjangaon Dairy facility, BIL is currently collecting 70,000 litres of milk per day from 2,850 farmers. The target is to take it up to 150,000 litres per day from 4,000+ farmers. PET dairy products, Dahi, Yogurts, and Powder Dairy products for retail and captive consumption all these products will be commissioned in a staggered manner. The Management also highlighted that it expects the non-Biscuits portfolio will be generating around ~45% of the overall revenue in the next 5 years.

Valuation:

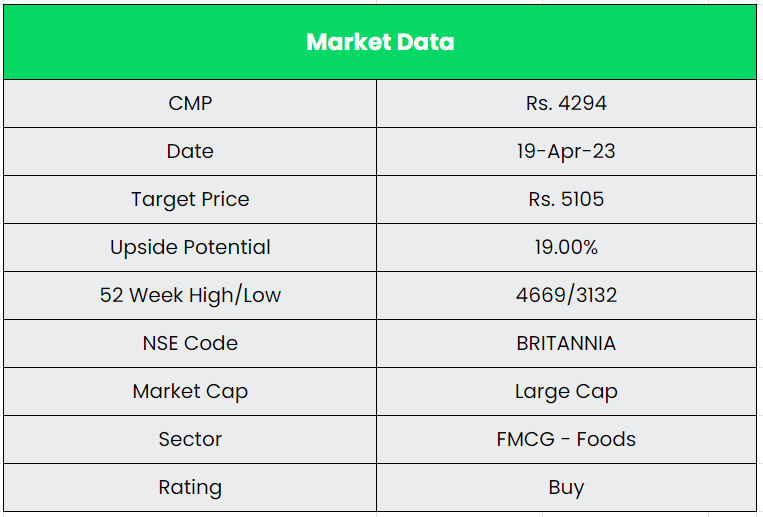

Britannia continues to gain market share and remains a leading brand in the biscuit portfolio. With further expansion into dairy products, the company is diversifying its dependency from the biscuits. We expect the company’s focus on capacity expansion, brand investment, direct reach expansion and product launches to spur profitable growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.5105, 46x FY25E EPS.

Risks:

- Competitive Risk – Even though BIL is the industry leader in the domestic biscuits segment, it faces intense competition from both large organised players and the fragmented unorganised market.

- Execution Risk – Any delay or failure in the execution of expanding new products or facility will impact the revenue growth of the company.

- Raw Material Risk – Prices of key raw materials such as wheat, sugar, milk, and refined palm oil depend on geo-climatic conditions, international prices, and the domestic demand-supply situation. Any increase in the material costs will impact the margins of the company.