APL Apollo Tubes Ltd. – Largest ERW Pipe Manufacturer

APL Apollo Tubes Limited (AATL) was incorporated in February 1986 as Bihar Tubes Private Limited with its headquarters in Delhi-NCR. AATL is among the largest ERW pipe/structural steel tube manufacturer in India. The company operates 11 manufacturing facilities across India with a total installed capacity of 3.6 million tons. The Group’s product offerings include 1,500+ varieties for structural steel applications. These tubes have a wide spectrum of usages in urban infrastructure and real estate, rural housing, commercial construction, greenhouse structures and engineering applications. The Group has also established a large pan-India distribution network of more than 800 distributors and over 50,000 retailers over the years.

Products & Services:

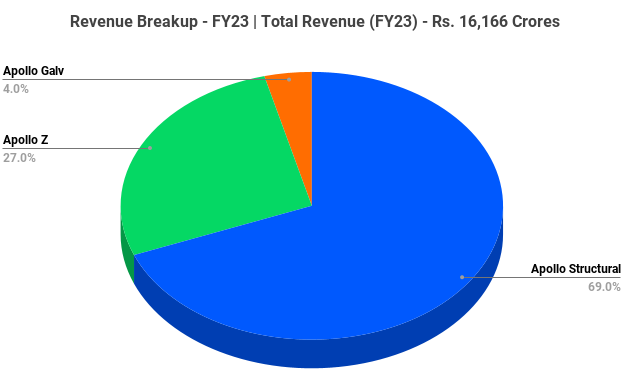

The company has various brands under various product segments namely Apollo Structural, Apollo Z, Apollo Galv and Apollo tricoat.

- Apollo Structural – Fabritech, Build, DFT, Column, FireReady and Agri are the brands under Apollo structural which is used as Structural, Piling, sheds, Gates, fencing, etc. in Residential building and Independent Homes.

- Apollo Z – CoastGuard in the only brand under Apollo Z used as Galvanised Structural Steel tubes for coastal markets.

- Apollo Galv – Plank, Signature, Elegant and Chaukhant are the brands under Apollo Galv which is used as Galvanizes Structural, Greenhouse structures, Plumbing, Firefighting, etc. in Commercial Building, Industrial and Agriculture.

- Apollo Tricoat – Green, Bheem and Z+ are the brands under Apollo Tricoat which is used as Door Frame, Staircase Steps, Furniture, Plank, Designer Tubes, etc. in Residential building, Commercial Building and Independent Homes.

Subsidiaries: As on FY23, the company has a total of 6 subsidiaries.

Key Rationale:

- Established Position – The company has a well-established position in the domestic ERW (Electric Resistance Welded) pipes segment and controls a 55% market share in the structural steel tubing/ERW Pipes Industry. The player 2 and 3 are having a market share of 10% and below. APL Apollo has been able to consistently expand its manufacturing capacities over the years to keep pace with the market growth. Additionally, over three decades of its existence, the company has established a large network of more than 800 distributors and over 50,000 retailers across the country. APL Apollo procures 2% of the India steel consumption and 10% of Indian Hot Rolled (HR) coil consumption. This enables it to obtain a 2% discount on its purchase, which many of its peers fail to take advantage of.

- Government Orders – The company has received approval for its tubular design for a railway station in South India and is in touch with at least 20 contractors for orders. The opportunity in railway station redevelopment in India is mammoth in size, with 1,500 new stations expected to be built over five years. Another important application of structural tubes is building water tanks under the “Jal Jeevan Mission”. Conventionally it takes around four to five months for creating a water tank using reinforced cement concrete (RCC), while APL Apollo in a demonstration using structural tubes installed a tank (200,000 liter capacity) near Lucknow with a height of 16 mtrs in three days. The Uttar Pradesh government has floated a tender to install 60,000 such overhead water tanks by CY24 and each water tank requires ~16 metric tons (MT) of structural tubes, thereby translating into an opportunity of over ~1 million MT.

- Q4FY23 – The Company reported its highest ever quarterly sales volume, EBITDA and PAT in Q4FY23. The company crossed Rs.300+ crs of EBITDA and Rs.200+ crs of PAT for the first time in a quarter in Q4FY23. Sales volume up by 18% YoY to 650k tons. Revenue expanded by 5% YoY to Rs.4431 crs. In Q4FY23 and EBITDA increased by 21% to Rs.323 crs for the same period. EBITDA per ton was Rs.4,970 (+3% YoY). Net Profit increased by 24% to Rs.202 crs.

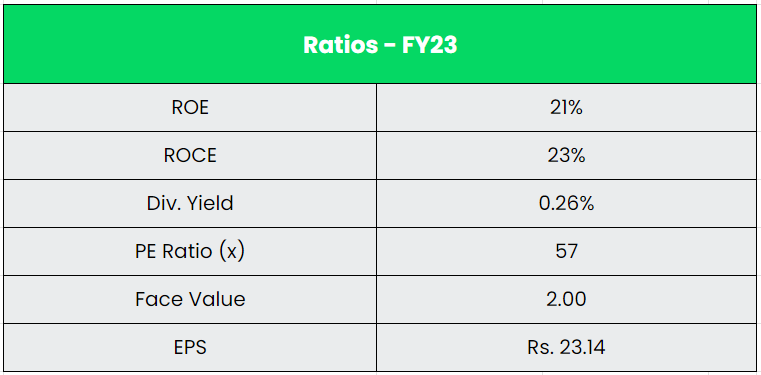

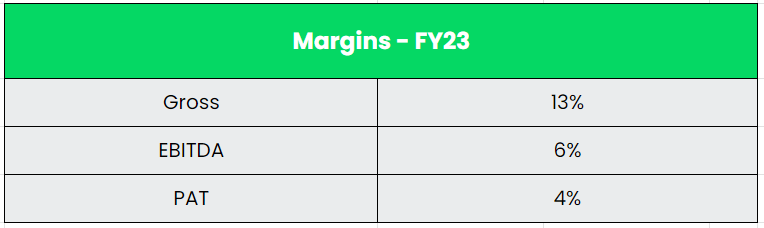

- Financial Performance – The company’s revenue and PAT CAGR stands at 25% and 32% between FY18-23. The Reserves in the balance sheet has grown at a CAGR of 29% for the same period. The company has a positive operating cashflow historically and a total of ~Rs.3185 crs for the last five years. The company has a strong balance sheet with a less debt/equity ratio of 0.3x. The company’s recent change in its business model to cash and carry has lowered its receivables and reduced its working capital days. The Net working capital days has been reduced from 29 in FY20 to 5 in FY23.

Industry:

The Real Estate sector is an essential segment of the Indian economy which has linkages with more than 250 ancillary industries and employs more than 10% of India’s workforce. The growth of the real estate sector in the last two decades has had a multiplier impact on the Indian economy. After agriculture, real estate is the second highest employment-generating sector. Steel and its allied products are important aspect of the real estate industry and the growth in the real estate market will directly impact the steel and other building products positively. Currently, the structural tube market in India is ~8 million MT (including ~4 million MT of tubes made from secondary steel). Numerous applications of structural tubes are gradually gaining momentum, such as public infrastructures (railways, airports), steel building solutions (highrise buildings, hospitals, schools, etc.), warehouses, cold storage, factory building and data centers, among others. It is expected to reach ~30 million MT in the longer run, led by growing applications of structural tubes.

Growth Drivers:

- Under Budget 2023-24, capital investment outlay for infrastructure is being increased by 33% to Rs.10 lakh crore (US$ 122 billion), which would be 3.3% of GDP and almost three times the outlay in 2019-20.

- Demand for residential properties has surged due to increased urbanization and rising household income. India is among the top 10 price appreciating housing markets internationally.

- The growing commercial building sector combined with the government’s initiatives towards green buildings, smart cities, make in India scheme, warehouses, airports and metros are expected to boost the structural steel fabrication market in India.

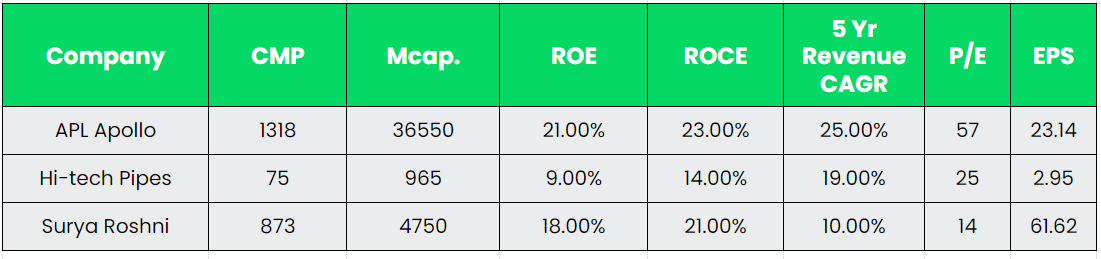

Competitors: Hi-Tech Pipes, Surya Roshni, etc.

Peer Analysis:

APL Apollo has many competitive advantages like premium pricing (brand power), low-cost producer (largest consumer of steel and HR coil), Technological advantage and strong distribution reach. APL Apollo also has backward integration which is lacked by its peers due to an average balance sheet.

Outlook:

APL Apollo tubes will be ramping up its capacity from the existing 3.6 MT to 5 MT by FY25 with a Capex of ~Rs.600 crs over the next 18 months, which is funded fully by internal accruals. The company plans to set up a 300,000-tonne plant in Dubai, which will start by Q4 of FY24, and target 200,000 tons over the next 3-4 years. Sales volume guidance for FY24 is at 2.8-3 MT and 3.8-4 MT by FY25 and 4.5-5 MT for FY26. (2.28 MT in FY23). Value Added Products contribution to rise to 60%+ in FY24 (from 56% in FY23) and to reach 75% once the Raipur plant ramp up stabilizes. Full potential from Raipur will be achieved in FY25 which will eventually improve the EBITDA/t. The company’s target is to operate the plant at Rs.7,000/t as it stabilizes going forward. It also expects to become debt-free by the end of FY24 or early FY25, funded by operating cash flows and residual capex.

Valuation:

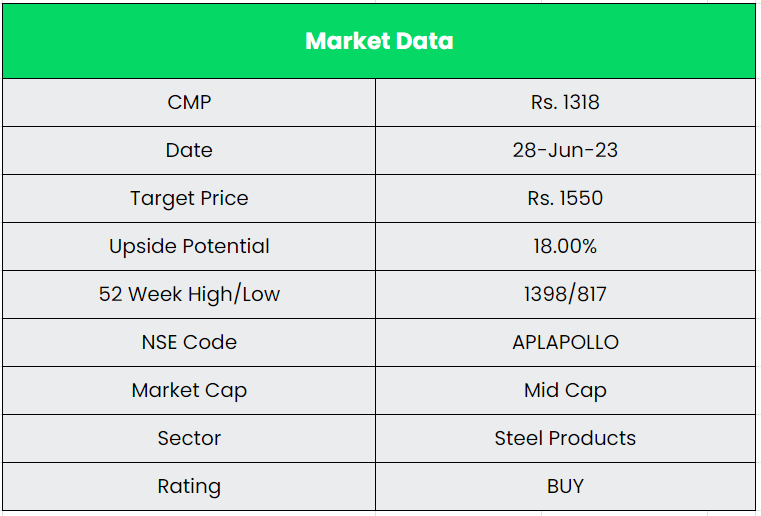

APL Apollo Tubes is the best play in the structural steel tube manufacturing given its leadership position in the industry, which is witnessing growing applications, increasing adoption for government projects, rising consumption of structural steel tubes in public infrastructure, residential and commercial buildings, warehouses, factories, agriculture and other construction works. We recommend a BUY rating in the stock with the target price (TP) of Rs.1550, 35x FY25E EPS.

Risks:

- Competitive Risk – The ERW pipes market is inherently competitive with the presence of several established players like Surya Roshni, Tata Steel, Jindal Pipes, Welspun Corp. etc. Further, as ERW pipe manufacturing is not a capital-intensive process, the entry barriers are low and hence, the industry has many unorganised players.

- Demand related Risk – Slowdown in steel demand, especially across building and construction segment, could impact the structural steel penetration within the steel sector. This would impact the company’s volume growth and, thus, margins.

- Raw Material Risk – The major raw materials for APL’s products are HR coils, galvanized coils and zinc, the prices of which are volatile. The prices of the HR coils are market linked and determined on a periodic basis, thus exposing the company to the volatility in the prices of raw materials which has a bearing on its profitability margins.