“Don’t try to buy at the bottom and sell at the top. It can’t be done except by liars”

– Bernard Baruch

Attempts at timing the market can make investors worse off in the long run than riding out the inherent volatility. This is simply because it’s hard to precisely forecast how the market will move in the future. Here is some data to show how market timing is highly unlikely to work.

Our analysis of stock market data shows that a significant chunk of investor gains over a long period of time is actually the result of only a handful of highest-return days or as we call them, the best days. Miss a few of these and your long-term investment returns can take a big hit. Conversely, if you stay out of the market on a few lowest-return or worst days, that can bump up your returns substantially.

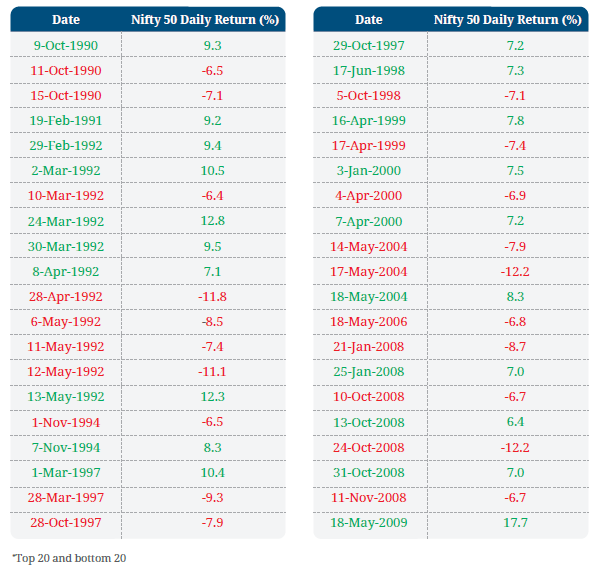

But these good and bad days are very hard to guess in advance. With these days (5 best and 5 worst) accounting for just 0.14% of the 7120 trading days over a 30-year period, it’s very easy to miss them in your effort to time your entries and exits to and from the market.

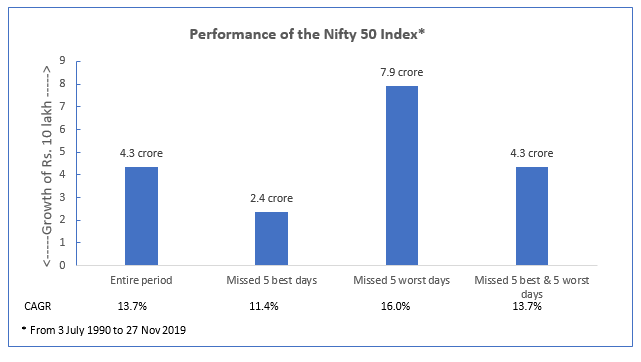

All it takes is a few days

We looked at the Nifty 50 daily returns from the start, July 1990 till November 2019. Assuming that someone invested ₹10 lakhs in the market at the start of this period (30-years approx.) and stayed put all through, then he would end up with ₹4.3 crores today.

Now, if we assume hypothetically that this person stayed out of the market on the 5 best days then his final investment value would be significantly lower at ₹2.4 crores at the end of the period. The cost of missing the best 5 days is a whopping ₹1.9 crores!

These calculations assume that an investor exits the market the day before the highest-return day and enters again the day after. So, his investment value remains unchanged on the highest-return day.

On the other hand, if an investor had kept away from the market on the 5 worst days (while staying invested during the best days) of the last 30 years, his investment would have multiplied to ₹7.9 crores today. Let’s take one final case. Assume an investor skips not only the 5 best days but also the 5 worst days then he would end up with ₹4.3 crores – a return similar to what someone who did not time and stayed through the entire period.

Trying to time the market

The examples taken above are unrealistic – no one is unlucky enough to skip all the best days or lucky enough to miss all the worse days. But they illustrate a point. Given that most big market gains and losses happen over a few days (concentrated in short periods) spread over decade-long periods, a few badly timed entries and exits are all it takes to ruin your long-term returns. And while a timely exit/s may help you pocket good gains in the short-run unless you re-enter at the right time, you can lose out in the long run.

What makes timing the market particularly difficult or rather impossible is that several of the high-return and low-return days are clustered within certain periods of high market volatility. Take, for instance, 29 Feb to 13 May 1992, when the Nifty 50 fluctuated from (-) 11.8% to 12.8%. Any attempt at timing the market (entering on the low days and exiting on the high days) through this period would have been futile and emotionally nerve-racking.

Clustering of best and worst days*

Possible way out

How must investors respond to periods of market volatility?

Investors can start by having an asset allocation that is aligned with their risk appetite. So, if you are risk-averse and can’t stomach large fluctuations in your equity portfolio, then consider allocating less than 30% of your investible funds into equity (stocks and mutual funds). Then even in a volatile market, a chunk of your portfolio in debt will remain unaffected and you are (hopefully) able to resist the temptation to make an impulsive exit from the market.

Those with moderate risk appetite can consider an equity allocation of 30-70% and those with a high-risk appetite can consider equity allocation upwards of 70%.

A simple strategy of rebalancing once a year or whenever the equity allocation deviates by more than 5% works great over the long run. However, given our inherent behavioural quirks, most investors may not be able to sit back and watch the entire equity portfolio fluctuate sharply over say a few months or so.

In this case, it is OK to sin a little if it helps you stick to your plan.

Investors can divide their portfolio into two portions, one of which they leave untouched and stay invested in for the long run. They can modify (read as try to reduce/increase equity allocation) the other portion based on certain factors such as valuations, fundamentals and sentiments to name a few. We will cover this in more detail in a future article.

This portion can act as a risk-reduction tool during times of significant overvaluation while at the same time humbly acknowledging the possibility of getting the timing wrong via the first buy-and-hold portion.

This article was originally published on MoneyControl. Click here to read it.