Company Overview:

EMS is in the business of Sewerage solution provider, Water Supply System, Water and Waste Treatment Plants, Electrical Transmission and Distribution, Road and Allied works, operation and maintenance of Wastewater Scheme Projects (WWSPs) and Water Supply Scheme Projects (WSSPs) for government authorities/bodies. WWSPs include Sewage Treatment Plants (STPs) along with Sewage Network Schemes and Common Effluent Treatment Plants (CETPs) and WSSPs include Water Treatment Plants (WTPs) along with pumping stations and laying of pipelines for supply of water (collectively, “Projects”). The treatment process installed at STPs and CETPs is compliant with Ministry of Environment, Forest and Climate Change of India norms and the treated water can be used for horticulture, washing, refrigeration and other process industries.

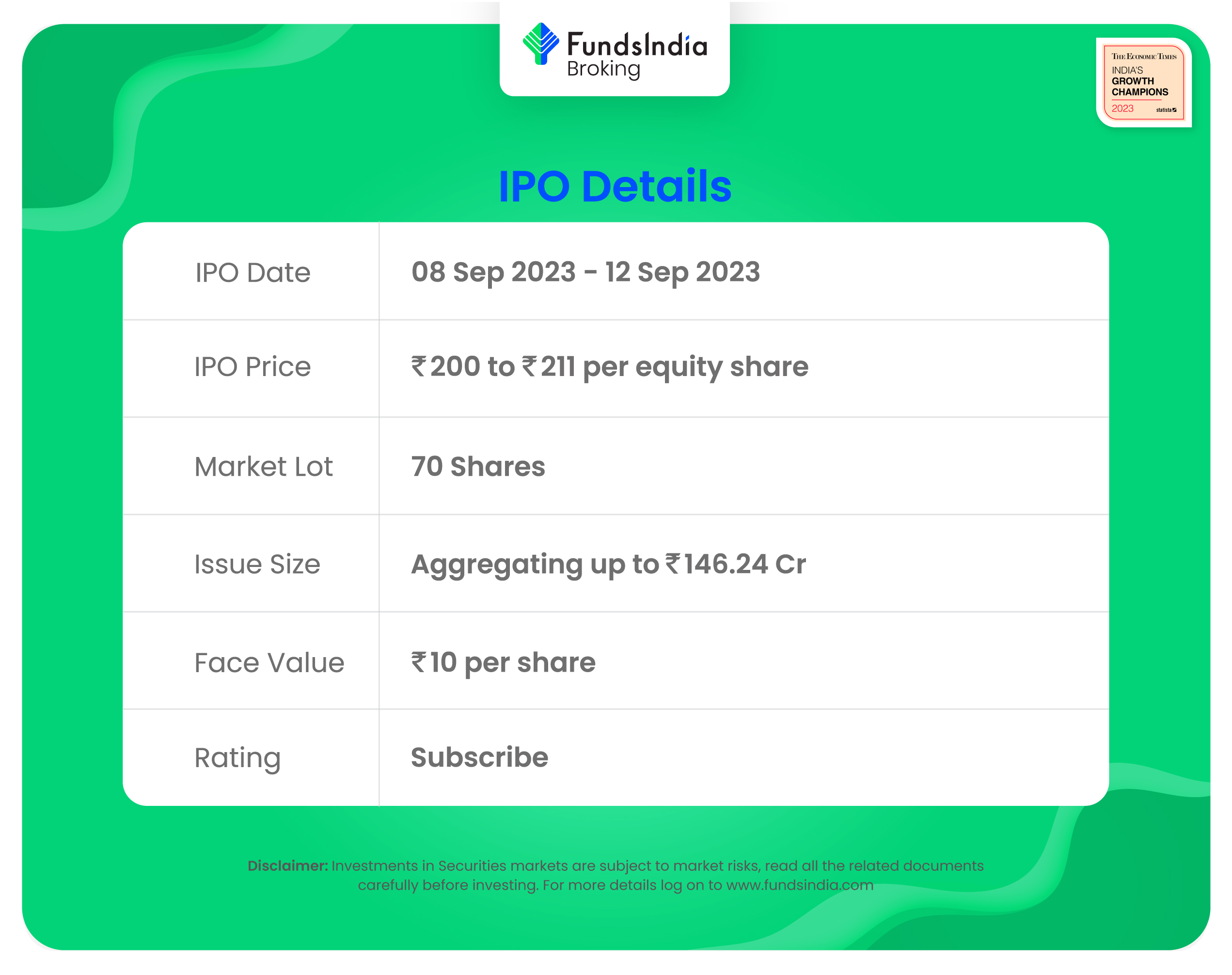

Objects of the Offer:

- Funding the working capital requirements of the Company.

- General corporate purposes.

Investment Rationale:

- Orderbook Position: Since incorporation, the Company has completed 67 projects. As on July 31, 2023, the company is operating and maintaining 18 projects including WWSPs, WSSPs, STPs & HAM aggregating of Rs.1,745 crore & 5 O&M (Operations and Maintenance) projects aggregating to Rs.99 crore. The company believe that consistent growth in their order book has materialized due to continued focus on Projects and the ability to successfully bid and win new Projects. The company also believes that the experience in designing, engineering, construction, operations and maintenance of Projects, technical capabilities, timely performance, reputation for quality and timely delivery, financial strength as well as the price competitiveness has enabled them to successfully bid and win projects. They also have a team of 61 engineers who are supported by third-party consultants and industry experts to ensure compliance and quality standards laid down by the industry and Government agencies & departments.

- Asset Light Model: The company’s business model relies on the strength of their brand, project execution and management capabilities as well as their well-established relationships with clients, architects and contractors. The company believe their asset light business model result in efficient utilisation of capital resulting in lower debt and regular income, allowing them to have higher return on capital employed. The company has a strong balance sheet which is reflecting in the debt-to-equity ratio of around 0.09x with a debt value of just Rs.45 crore for HAM Project of Mirzapur Ghazipur. The cash and cash equivalents stand at Rs.122 crore, ~3x of its outstanding debt, which allows them to seek further debt financing easily as and when required.

- Financial Track Record: The company’s revenue has grown at a CAGR of 18% from Rs.326 crore in FY20 to Rs.538 crore in FY23. EBITDA has grown at a decent rate of 13% CAGR from Rs.103 crore in FY20 to Rs.149 crore in FY23. The PAT of the company has grown at a CAGR of 14% for the same period. State wise, Uttar Pradesh contributed 49% of the overall revenue in FY23, followed by Rajasthan with 23%, Bihar with 17.5%, Uttarakhand with 10% and other with 0.5%. The RoE (Return on Equity) of the company is 22% in FY23 and it is maintained at 20%+ levels consistently for the past 4 years. Likewise, the RoCE (Return on Capital Employed) of the company is 28% in FY23 and it is maintained at 25%+ levels consistently for the past 4 years.

Key Risks:

- Dependency Risk – The company is heavily dependent on the Government projects and changes in Government policies related to the environment and water treatment may adversely affect the business, financial condition and results of operations.

- Blacklisted – The company has faced blacklisting in the past by two Government bodies for the reason of the death of five labourers due to lack of safety. This may raise concerns about its reputation and ability to secure future projects.

- OFS – The IPO is a mix of offer for sale (OFS) and Fresh issue with OFS being 54% of the overall issue size. In the offer for sale (OFS), Mr. Ramveer Singh is the only selling shareholder, also the promoter who will offload up to 82,94,118 equity shares.

Outlook:

The company’s majority promoter Mr. Ramveer Singh has more than 3 decades of experience in the water & waste-water treatment industry. According to RHP, the company has only one listed peer named VA Tech Wabag which is trading at a TTM P/E of 93x (High P/E due to low EPS on account of one-off expense in Q4FY23). If we adjust the one-off expense, the P/E is around 15x based on FY23 EPS. At the higher price band, the listing market cap of EMS will be around ~Rs.1172 crore and the company is demanding a P/E multiple of 11x based on post issue diluted FY23 EPS. Though it is not appropriate to compare the company with just one competitor, the issue with a P/E of just 11x seems to be undervalued in general. Based on the above views, we provide a ‘Subscribe’ rating for this IPO.

If you are new to FundsIndia, open your FREE investment account with us and enjoy lifelong research-backed investment guidance.