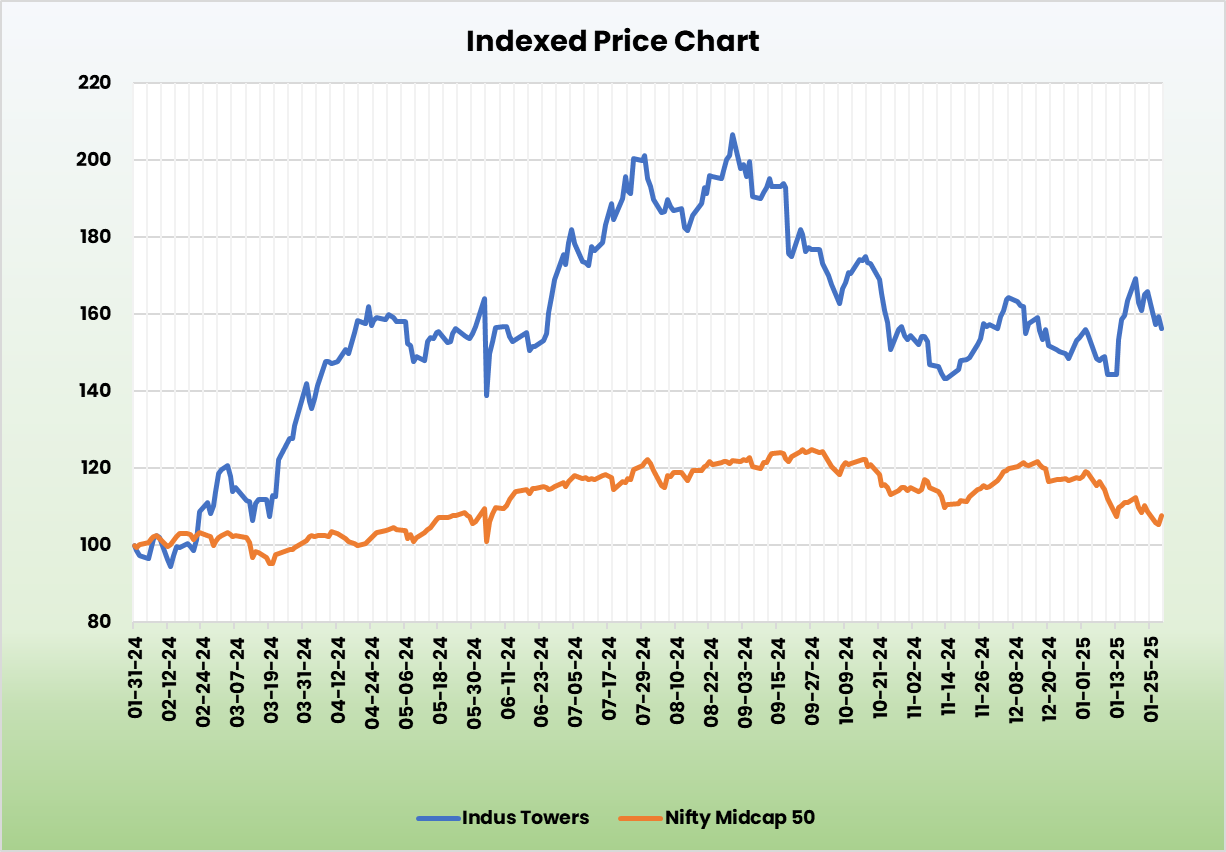

Indus Towers Ltd – Connecting Lives Across the Nation

Indus Towers Ltd., formed through the merger of Indus Towers and Bharti Infratel, is one of the largest telecom tower companies globally. Established in 2006 and headquartered in Gurugram, the company provides tower and related infrastructure-sharing services, managing the deployment, ownership, and operation of passive infrastructure for telecom networks. As of December 31, 2024, Indus Towers operates over 234,643 macro towers and 386,819 macro co-locations, with a presence across all 22 telecom circles in India. Its client base includes industry giants such as Bharti Airtel (along with Bharti Hexacom), Vodafone Idea Limited (VIL), and Reliance Jio Infocomm Limited.

Products and Services

The company’s products and services are centered around 3 core elements:

- Tower – For mounting the operator antennae at an appropriate height, encompassing a wide range of designs from ground-based towers and rooftop towers to hybrid poles and monopoles.

- Power – For providing uninterrupted energy supply to telecom equipment including greener energy solutions.

- Space – Collaboration with residential and commercial property owners for housing telecom and power equipment.

Subsidiaries: As of FY24, the company has 1 subsidiary and no associates/joint ventures.

Investment Rationale

- Market leader – Indus Towers is the leading provider of tower infrastructure in the country, serving top Telecom Services Providers (TSPs). It primarily offers shared access to its towers for wireless telecommunications providers through long-term contracts. The company is steadily increasing its market share, fuelled by the rapid rollout of 5G services by TSPs, which has significantly boosted its revenue. Additionally, the continued expansion into rural areas by major clients is expected to create further growth opportunities. The company currently serves all telecom providers across India and has a presence in all 22 telecom circles nationwide. With an industry-leading tenancy ratio of 1.65x, Indus remains a dominant force in the sector. The company is also consistently achieving stable financial performance underpinned by robust tower and co-location additions. During Q3FY25, it added 4,985 macro towers and 7,583 macro co-locations.

- Growth strategies – The company has collected significant overdue from VIL. It has also secured a significant share of the roll out by VIL. The company is also focusing on optimising its power and fuel cost (which is a major contributor of the company’s operating expense) through lowering diesel cost and increasing the use of solar energy. The company’s solar sites currently stand at 28,000 which was 25,000 during the previous quarter. It has also entered into a power purchase agreement with a strategic partner for procurement of renewable energy of 130 MW solar plant via a 26% acquisition of stake at a consideration of Rs.38 crore. It is also transitioning its battery portfolio to lithium-ion batteries which has lower charging time and a longer life. The company is pivoting towards an increased share of lighter tower variant. These strategic initiatives are expected to improve operating and cost efficiencies. The company plans to foray into the EV charging infrastructure sector and has launched its pilot services in the business hub of Gurugram and the southern city of Bengaluru.

- Q3FY25 – During the quarter, the company generated revenue of Rs.7,547 crore, an increase of 5% compared to the Rs.7,199 crore of Q3FY24. Operating profit increased from Rs.3,622 crore of Q3FY24 to Rs.6,997 crore of Q3FY25, a growth of 93%. The company reported net profit of Rs.4,003 crore, an increase by 160% YoY. The profits were influenced by the collection of overdues and collection of Rs.19.1 billion from monetization of the secondary pledge on shares by VIL in the company. Adjusting to this, EBITDA and net profit has improved by 8% each during the quarter.

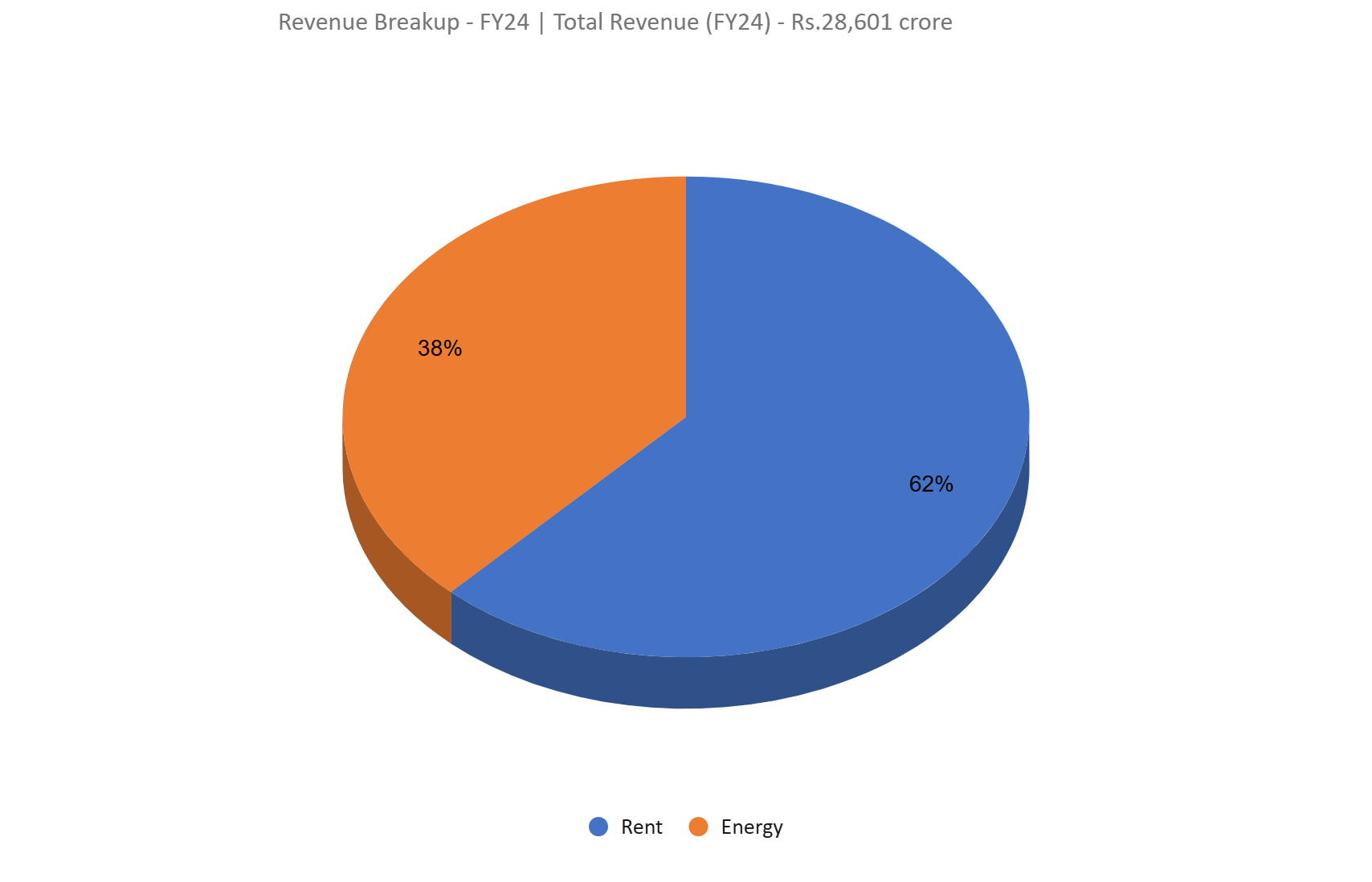

- FY24 – During the FY, the company’s revenue was flat at Rs.28,601 crore. Operating profit was at Rs.14,694 crore, up by 50% YoY. The company reported net profit of Rs.6,036 crore, an increase of 196% YoY. During the financial year, the company crossed 2 lakh towers in its portfolio.

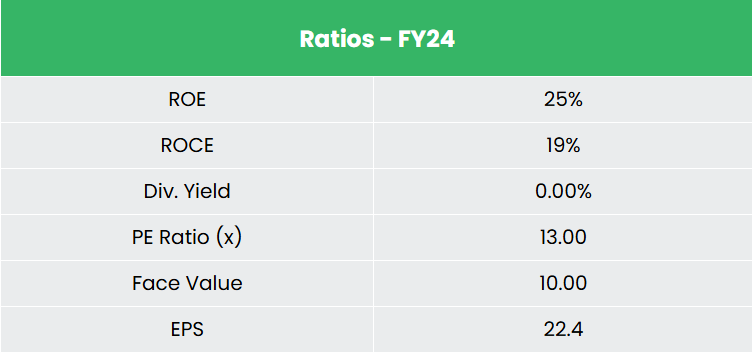

- Financial performance – The company has generated revenue and net profit CAGR of 27% and 17% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 22% and 19% for FY21-24 period. The company has a robust capital structure with a debt-to-equity ratio of 0.75.

Industry

The telecommunications industry in India is one of the fastest-growing sectors and a major contributor to employment, ranking among the top five job generators in the country. Affordable tariffs, roll-out of Mobile Number Portability (MNP), evolving consumption patterns of subscribers, government’s initiatives towards digitization are bolstering India’s domestic telecom manufacturing capacity, and a conducive regulatory environment lays strong foundation for exponential growth in the industry. As of May 2024, India is the second-largest telecommunications market globally, with a total of 1,203.69 million telephone subscribers. However, rural tele-density stands at just 59.59%, presenting a significant growth opportunity in this underserved area. Furthermore, India is already laying the groundwork for 6G by investing in the technology’s development.

Growth Drivers

- In Union Budget 2024-25, the Department of Telecommunications and IT was allocated Rs.116,342 crore (US$ 13.98 billion).

- Government initiatives such as 100% FDI allowed under the automatic route, PLI for Telecom and Networking equipment, Digital Bharat Nidhi Fund, reduced license fees, and spectrum liberalization.

- Growing population and a rapidly increasing internet penetration rate with is expected to drive the demand for telecom services.

Peer Analysis

Competitors: Suyog Telematics Ltd, Sar Televenture Ltd etc.

Compared to the above competitors, Indus Towers stands out as the most undervalued stock in this segment. The company is consistently translating its steady growth in sales into expanding margins and earnings.

Outlook

The company’s four strategic priorities are: a) increasing market share, b) improving cost efficiency by optimizing diesel usage, c) ensuring network uptime, and d) promoting sustainability. During the past year, the widespread rollout of 5G services by operators has driven higher revenue streams and fuelled strong growth for the company. Factors that could drive growth include large-scale nationwide operations in an industry with significant entry barriers, the increasing potential for data consumption and the rise in data users/devices, a strong presence across all telecommunications circles, and long-term contracts with clients.

Valuation

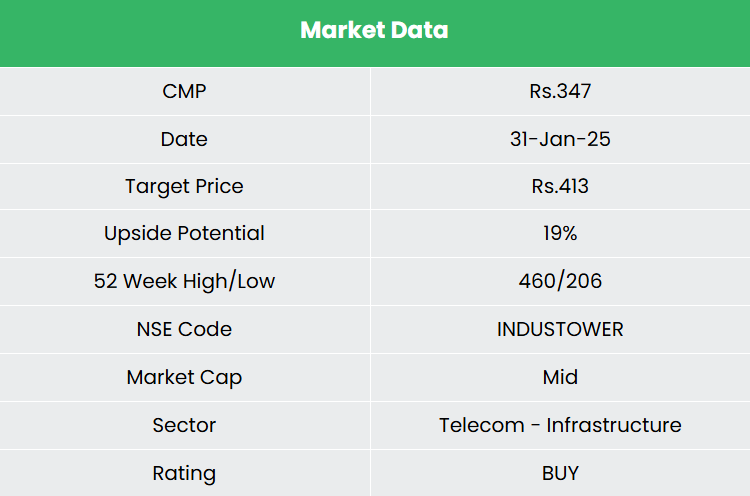

The demand for telecom infrastructure is expected to stay strong, driven by high data consumption, rapid 5G rollouts, and the existing network gap in 4G services. We believe Indus Towers Ltd. is well-positioned to take advantage of these trends. We recommend a BUY rating in the stock with the target price (TP) of Rs. 413, 16x FY26E EPS.

Risk

- Financial stability of TSPs – The rising investments in 5G rollout, along with other services and spectrum acquisitions, are putting pressure on TSPs’ financials. This could potentially affect their ability to make payments to Indus Towers, which might, in turn, impact the company’s financial performance.

- Unfavourable terms for contract renewal – Any unfavourable changes to the contract terms with the client, such as lower pricing or annual price escalations when renewing leasing agreements, pose a risk to the company.

Recap of our previous recommendations (As on 31 January 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.