Brigade Enterprises Ltd – Transforming City Skylines

Established in 1986 and headquartered in Bengaluru, Brigade Enterprises Ltd. is a prominent real estate developer in India with diverse portfolio spanning residential, commercial, hospitality and retail sectors. The company has developed many landmark buildings across Bengaluru, Mysuru, Hyderabad, Chennai and Kochi. As of 31 March 2025, the company has delivered 300+ buildings constructed upon 100+ mn sq. ft area. It is also the licence owner for 6 World Trade Centres in South India. The company is among the top 10 listed real estate developers in the country.

Products and Services

The company functions primarily under 4 business segments:

- Residential – Includes apartments, integrated enclaves, villas and plotted developments.

- Commercial – Commercial and co-working spaces (BuzzWorks).

- Retail – Includes malls (Orion Malls), support retail and arcades that serve the company’s residential and commercial complexes.

- Hospitality – Comprises a portfolio of luxury hotels, convention centres, recreation clubs etc.

Subsidiaries: As of FY24, the company has 22 subsidiaries and 2 limited liability partnerships.

Investment Rationale

- Entry into new geographies – The company is steadily expanding its presence outside of Bengaluru, targeting key markets such as Chennai, Hyderabad, and Mysuru. In Chennai, notable developments include Brigade Icon, a mixed-use project integrating residential, retail, and office spaces, with a Gross Development Value (GDV) of Rs.1,800 crore, and Brigade Altius, a premium residential project with a GDV of Rs.1,700 crore. The company has recently acquired additional 5.41-acre land in Chennai, earmarked for a marquee residential development with a projected revenue potential of Rs.1,600 crore. In Hyderabad, Brigade has a pipeline of projects totalling 3 mn sq. ft., which includes 1 mn sq. ft. ready for launch, another 1 mn sq. ft. already signed, and 1 mn sq. ft. currently under process. In Mysuru, the company has taken a strategic step by acquiring a 51% stake in Mysore Projects Private Ltd, a local real estate developer. It has also entered into a Joint Development Agreement (JDA) for a luxury residential and senior living project with an estimated GDV of Rs.300 crore.

- New projects – The company has acquired a prime land parcel in Bengaluru for the development of a residential project with a projected GDV of Rs.2,700 crore. Additionally, it has secured another site in the city to develop a premium commercial project with an estimated GDV of Rs.2,000 crore. In Hyderabad, the company has launched a large-scale mixed-use development with a revenue potential of Rs.3,300 crore. This project includes upscale residences, a World Trade Centre, a 300+ key international hotel, and an Orion Mall. Furthermore, the company has signed a Memorandum of Understanding (MoU) with Technopark to establish a World Trade Centre in Kerala.

- Q4FY25 – During the quarter, the company reported revenue of Rs.1,532 crore compared to the Rs.1,763 crore of Q4FY24, a decline of 13%. Operating profit was flat at Rs.488 crore. Net profit increased by 18% to Rs.249 crore from Rs.211 crore YoY. Operating profit margin has improved from 28% to 32% and net profit margin has improved from 12% to 16%. Average price realization surged by 47% during the period to Rs.12,082/sq. ft.

- FY25 – The company generated revenue of Rs.5,314 crore, an increase of 5% compared to FY24 revenue. Operating profit is at Rs.1,654 crore, up by 21% YoY. The company posted net profit of Rs.680 crore, a growth of 69% YoY. The company has achieved presales of Rs.7,847 crore, a 31% YoY growth in its real estate business. Revenue from lease rentals stood at Rs.1,165 crore, a 24% growth.

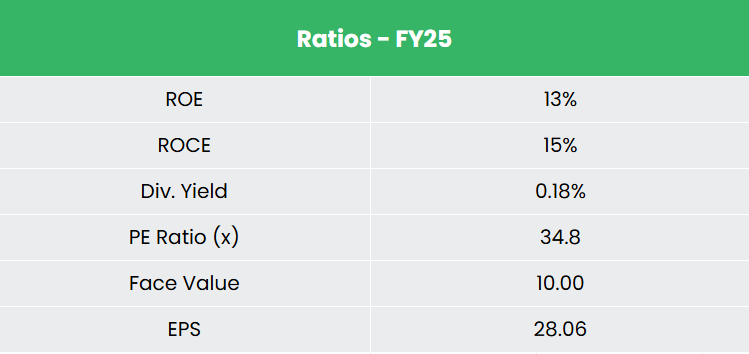

- Financial Performance – The company has generated revenue and net profit CAGR of 19% and 114% over the period of 3 years (FY23-25). The average 3-year ROE & ROCE is at 11% and 12% for FY23-25. The company has a debt-to-equity ratio of 0.97.

Industry

The Indian real estate sector is poised for strong growth, with a projected CAGR of 9.2% from 2023 to 2028, driven by rapid urbanization, rising demand for housing, and increasing property values. Comprising residential, commercial, retail, and industrial segments, the sector plays a vital role in infrastructure development and has strong linkages with allied industries like cement and steel. Urban migration – expected to reach 590 million people by 2036 – is accelerating demand for affordable housing, while India’s position as a global IT hub continues to boost commercial real estate needs. The market is projected to reach $1 trillion by 2030, supported by corporate expansion and the growing need for office and retail spaces.

Growth Drivers

- The Government has allowed FDI of up to 100% for townships and settlements development projects.

- The Union Budget 2025–26 boosts housing demand by exempting tax on two self-occupied properties (up from one) and raising the TDS threshold on rent from Rs.2.4 lakh to Rs.6 lakh

- Schemes such as the revolutionary Smart City Mission (target 100 cities) are expected to improve quality of life through modernized/ technology driven urban planning.

Peer Analysis

Competitors: Godrej Properties Ltd, Prestige Estates Projects Ltd, etc.

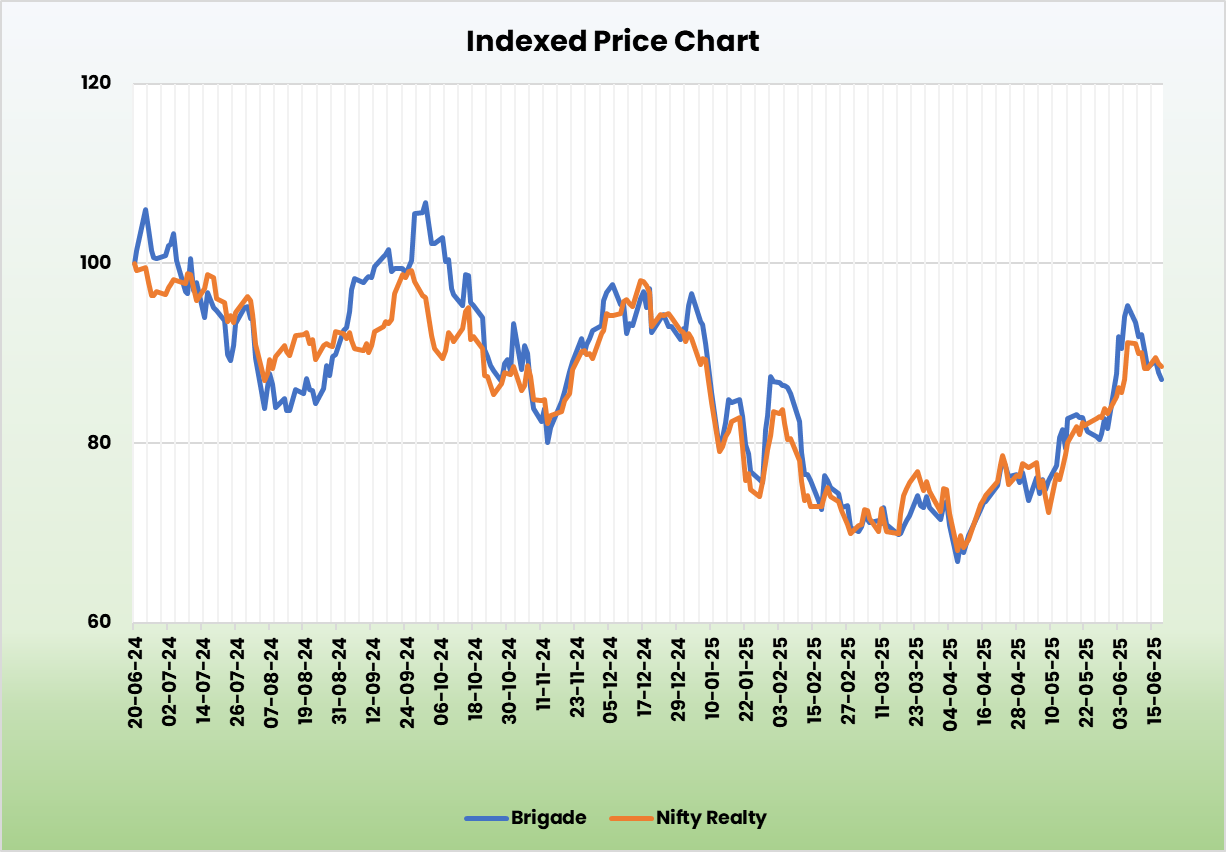

Compared to its peers, Brigade appears undervalued, with consistent returns on invested capital supported by stable revenue growth.

Outlook

Brigade Enterprises is poised for strong growth, driven by the launch of premium projects that have boosted average realizations by 40% to Rs.11,138/sq.ft. As of March 31, 2025, the company has 26 mn sq. ft. of ongoing developments and 16 mn sq. ft. in the pipeline. It is also preparing for the IPO of its hospitality arm, Brigade Hotel Ventures Ltd. The company has strengthened its capital structure, lowering the average cost of debt from 8.82% to 8.67% in FY25. Gross debt stands at Rs.4,444 crore, offset by Rs.3,483 crore in cash and equivalents. Notably, 82% of this debt is tied to its commercial portfolio, backed by rental income, while the residential segment is being maintained debt-free -supported by strong sales and collections. The company is targeting EBITDA margins of 27% – 28% from new launches.

Valuation

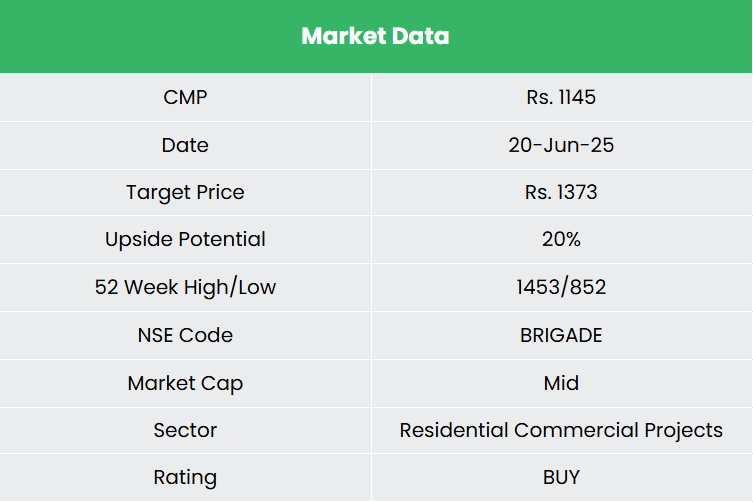

We believe the company will be able to sustain its growth driven by robust launch pipeline and strong execution capabilities. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,373, 39x FY27E EPS.

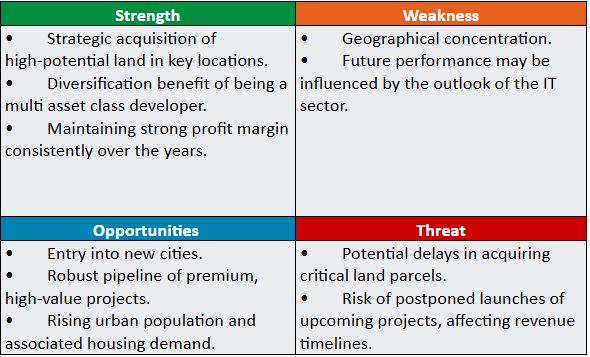

SWOT Analysis

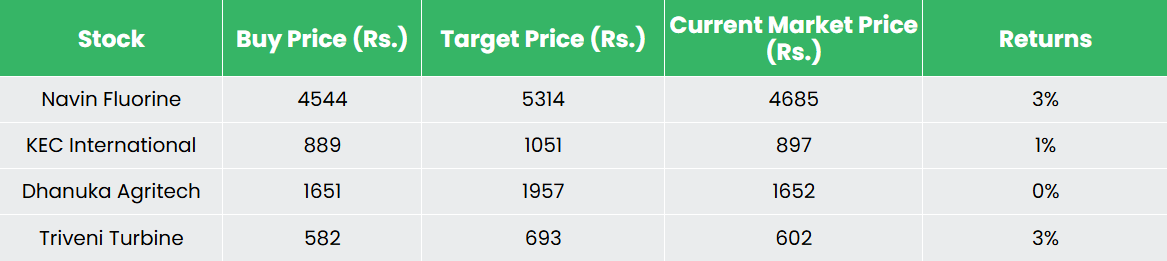

Recap of our previous recommendations (As on 20 June 2025)

Navin Fluorine International Ltd

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.