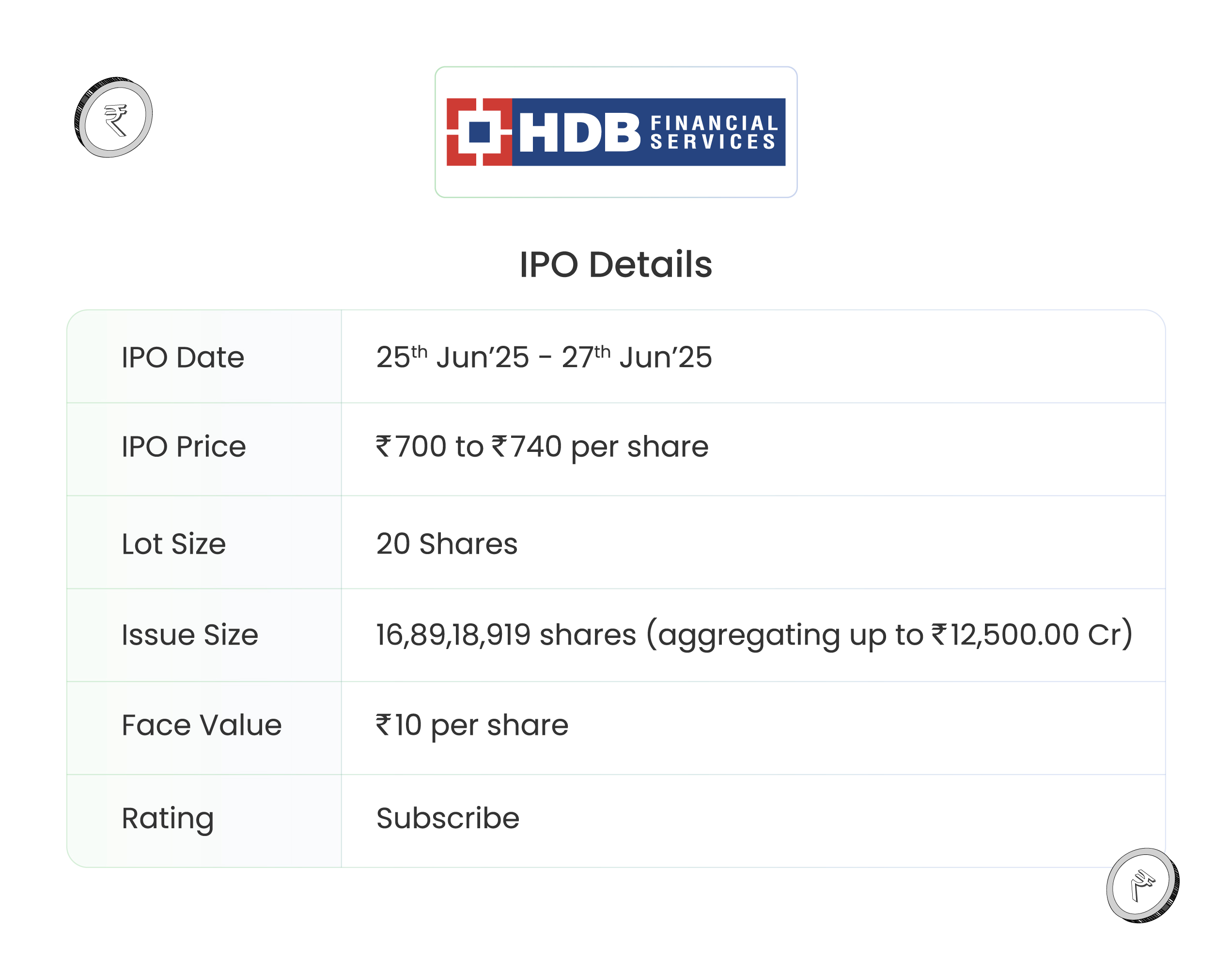

Company overview

HDB Financial Services Ltd is seventh largest leading diversified retail-focused non-banking financial company (NBFC) in India. Categorized by the RBI as an upper layer NBFC (NBFC-UL), the company offers a large portfolio of lending products through three business verticals – Enterprise Lending, Asset Finance and Consumer Finance. The company commenced its operations as a subsidiary of HDFC Bank Ltd, the largest private sector bank in India. With a client base comprised of salaried and self-employed individuals, as well as business owners and entrepreneurs, the company primarily caters to underserved and underbanked customers in low-to middle-income households with minimal or no credit history.

Objects of the offer

- Augmenting company’s Tier – I capital base to meet future capital requirements including onward lending, arising out business growth.

- Carry out an offer for sale of equity shares aggregating Rs.10,000 crore by the selling shareholders.

- To receive the benefit of listing of equity shares on stock exchanges.

Investment Rationale

- Business segments – The company operates through three primary business verticals: enterprise lending, asset finance, and consumer finance. Enterprise lending, which accounts for 39.3% of total gross loans, offers secured and unsecured credit to micro, small, and medium enterprises (MSMEs) to support their diverse and evolving business needs. Asset finance contributes 38.03% of gross loans and provides secured loans for income-generating assets such as new and used commercial vehicles, construction equipment, and tractors. Consumer finance, making up 22.66% of gross loans, includes both secured and unsecured loans for the purchase of consumer durables, digital and lifestyle products, two-wheelers, automobiles, and other personal loans.

- Rapidly growing customer base – The company boasts a rapidly expanding customer base, ranking as the second largest and third fastest-growing customer franchise among its NBFC peers, according to a CRISIL report. As of FY25, it has served 19.2 million customers, reflecting a robust CAGR of 25.45% over FY23–25. Customer concentration risk remains low, with the top 20 customers accounting for just 0.34% of the total gross loan book. The company’s target customers are the underbanked yet bankable population of India.

- Wide distribution network – The company has built a robust nationwide footprint, operating 1,771 physical branches across more than 1,170 towns and cities in 31 States and Union Territories. The branch network is geographically balanced, with no single region comprising more than 35% of the total branches. Notably, over 80% of branches are located outside India’s 20 most populous cities (as per the 2011 census), and more than 70% are situated in Tier 4 and smaller towns. This underscores the company’s strong focus on reaching underserved and underbanked customer segments across India.

- Financial Performance – The company reported a total income of Rs.87 billion in FY25 as against Rs.63 billion in FY23, a growth of 18%. The net interest income of the company in FY25 was Rs.74 billion. The PAT of the company in FY25 is Rs.20 billion. The CAGR between FY23-25 of net interest income is 17% and PAT is 5%. Between FY23-25, GNPA improved from 2.73% to 2.26%. However, NNPA declined from 0.95% for FY23 to 0.99% for FY25. Total gross loans is at Rs.1,069 billion, a CAGR of 23.54% between FY23-25. During the same period, AUM grew at a CAGR of 23.71% to Rs.1.073 billion. The ROA and ROE of the company stand at 2.16% and 14.72% respectively in FY25.

Key risks

- OFS risk – In addition to a fresh issue, the IPO will see the sale of shares worth up to Rs.10,000 crore by Promoter Selling Shareholder HDFC Bank Ltd.

- Default risk – The risk of non-payment or default by customers (heightened by the fact that banks cater majorly to economically weaker and low to middle-income segments) may adversely affect the company’s business, results of operations and financial conditions.

- Regulatory risk – Any inability to comply with the requirements stipulated by RBI could have a material adverse effect on the company’s business.

Outlook

The company maintains a stable presence in the low-income financing segment, with consistent growth in its customer base over the reported periods. Its established brand and strong parent backing are expected to support continued growth momentum. According to RHP, Bajaj Finance Limited, Sundaram Finance Limited, Shriram Finance Limited are few of the listed competitors for HDB Financial Services Ltd. The peers are trading at an average P/E of 23.20x with the highest P/E of 34.30x and the lowest being 13.00x. At the higher price band, the listing market cap of HDB Financial Services will be around ~Rs.61,388 crore and the company is demanding a P/E multiple of 28.21x based on post issue diluted FY25 EPS of Rs.26.23. When compared with its peers, the issue seems to be reasonably priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.