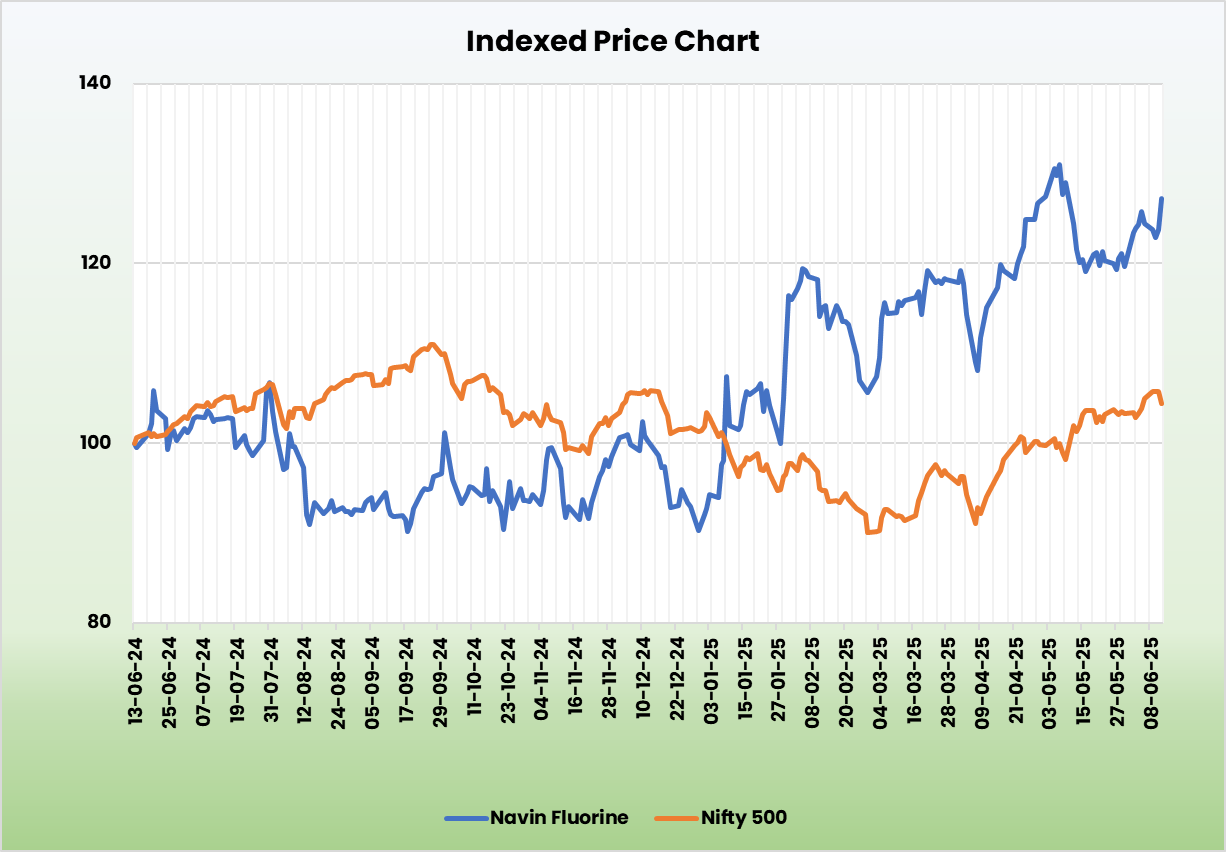

Navin Fluorine International Ltd – Leaders in Fluorine

Navin Fluorine International Ltd. is one of the largest Indian manufacturers of specialty fluorochemicals. The company’s offerings encompass a range of fluorine-based intermediaries, specialty chemicals, inorganic chemicals and contract research services. Established in 1998 and headquartered in Mumbai, the company operates one of the largest integrated fluorochemicals complexes with 3 manufacturing facilities in India and 1 in UK. It produces 60+ fluorinated products for domestic and international customers.

Products and Services

The company has 3 main strategic business units – High Performance Products (HPP), specialty fluorides, and Contract Development and Manufacturing Organization (CDMO). The products offered by the company majorly comprises of synthetic cryolite, fluorocarbon gases, hydrofluoric acid and other chemicals.

Subsidiaries: As of FY24, the company has 6 subsidiaries and 1 joint venture.

Investment Rationale

- Growth strategies – The company has signed a strategic agreement with The Chemours Company to manufacture Opteon, a proprietary two-phase immersion cooling fluid designed to meet the rising demand from advanced data centers and AI hardware for high-performance, sustainable, and cost-effective cooling solutions. To support this initiative, the company is establishing a manufacturing facility at its Surat plant, with operations expected to begin in Q1FY27. This marks the company’s first foray into the advanced materials sector. Additionally, the company has partnered with Buss ChemTech AG of Switzerland as its technology collaborator for the commercialization of Solar and Electronic Grade HF. It also plans to launch two new fluoro intermediates for its global agrochemical partners in FY26.

- Expansion plans – In FY25, the company successfully commercialized the Surat R32(II) project, adding 45,000 TPA of production capacity. It also commenced operations at its new fluoro specialty chemical facility in Dahej, which has an estimated peak revenue potential of Rs.600 crore per annum. Meanwhile, construction is underway for a new cGMP4 facility in Dewas, with commercialization targeted for Q3FY26. This facility will enhance the company’s CDMO capabilities to better serve global pharmaceutical clients. Additionally, the company is investing Rs.450 crore in a new AHF plant, expected to be completed by Q2FY26.

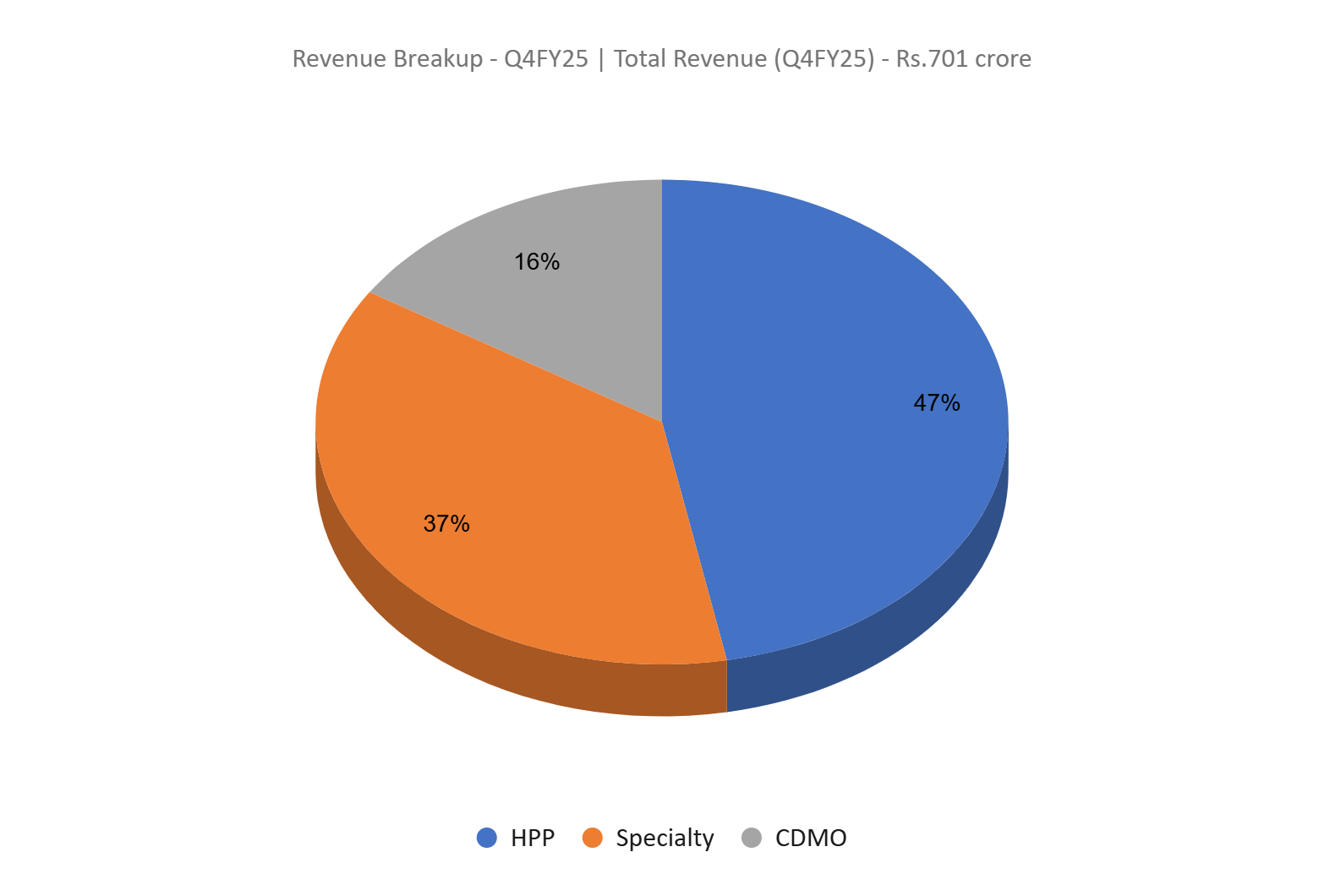

- Q4FY25 – During Q4FY25, the company generated a revenue of Rs.701 crore, achieving an increase of 16% as compared to the Rs.602 crore of Q4FY24. This growth was driven by strong performances in the HPP and CDMO segments, which grew by 10% and 141% respectively. EBITDA improved by 63% YoY, from Rs.110 crore to Rs.179 crore. Net profit stood at Rs.95 crore, an increase of 36% from Rs.70 crore of Q4FY24. Margins expanded YoY, EBITDA margin from 18% to 26% and net profit margin from 12% to 14%. Repeated and new order wins and strong execution capabilities across all verticals was instrumental in this performance.

- FY25 – During the financial year, company’s revenue increased by 14% to Rs.2,349 crore, operating profit increased by 34% to Rs.534 crore and net profit increased by 7% to Rs.289 crore.

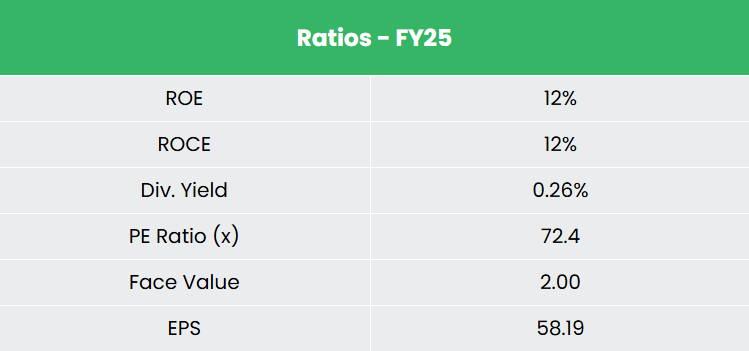

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 17% and 3% between FY23-FY25. TTM sales and net profit growth is at 14% and 25% respectively. The 3-year average ROE and ROCE for the company is around 13% and 14% during FY23-25. The company has a healthy capital structure with a debt-to-equity ratio of 0.56.

Industry

India’s chemical industry is highly diversified, producing over 80,000 products. It ranks 6th globally and 3rd in Asia, contributing 7% to the country’s GDP. Valued at US$ 220 billion, the industry is expected to grow to US$ 300 billion by 2030 and US$ 1 trillion by 2040, driven by strong manufacturing capabilities and rising domestic and global demand. Specialty chemical companies in India are expanding capacity to capitalize on this growth. The global fluorochemicals market, valued at US$ 28.7 billion in 2023, is projected to reach US$ 41.35 billion by 2030, growing at a CAGR of 5.35%. Fluorochemicals have wide-ranging applications across refrigeration, automotive, electronics, textiles, agriculture, and pharmaceuticals.

Growth Drivers

- Under the Union Budget 2025-26, the government allocated Rs.1,61,965 crore (US$ 18.7 billion) to the Ministry of Chemicals and Fertilizers.

- 100% FDI is allowed under the automatic route in the chemicals sector with a few exceptions that include hazardous chemicals.

- Ministry of Chemicals and Fertilisers is working towards implementing the Production Linked Incentive (PLI) for the specialty chemicals sector.

Peer Analysis

Competitors: Gujarat Fluorochemicals Ltd, Anupam Rasayan India Ltd, etc.

Compared to its competitors, the company has generated stable returns on invested capital, reflecting prudent capital allocation. Its consistent sales growth suggests increasing market penetration.

Outlook

Navin Fluorine is well-positioned for growth, supported by strong order book visibility anchored by multi-year contracts. As market adoption accelerates, the strategic partnership with Chemours is expected to evolve further, with both companies likely to explore opportunities to meet rising demand. The collaboration with Chemours marks the company’s entry into a new business vertical, reinforcing its long-term growth strategy. The CDMO business continues to demonstrate robust momentum with a healthy order pipeline. The company remains focused on advancing a portfolio of 10 – 15 commercial or late-stage products with significant scale-up potential. For FY26, the company is maintaining an EBITDA margin guidance of 25%.

Valuation

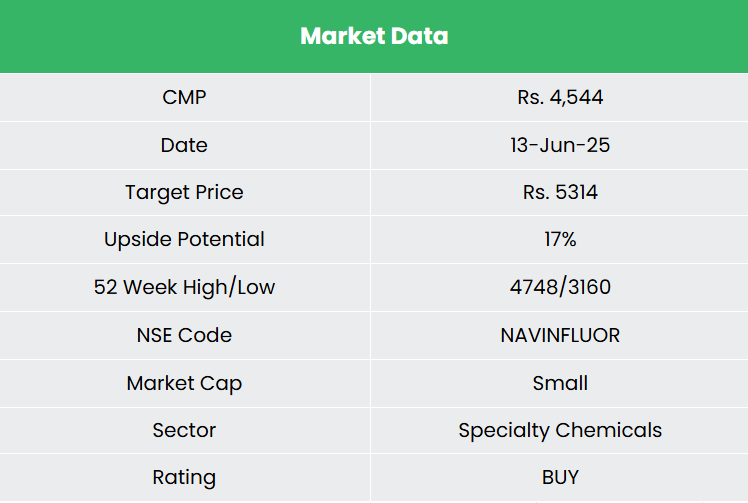

We believe the company is poised to sustain its growth momentum, given its entry into niche markets backed by strong capacity expansion plans. We recommend a BUY rating in the stock with the target price (TP) of Rs.5,314, 51x FY27E EPS.

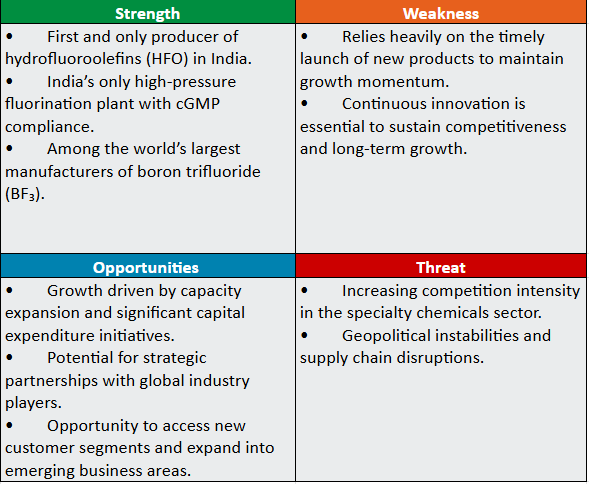

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.