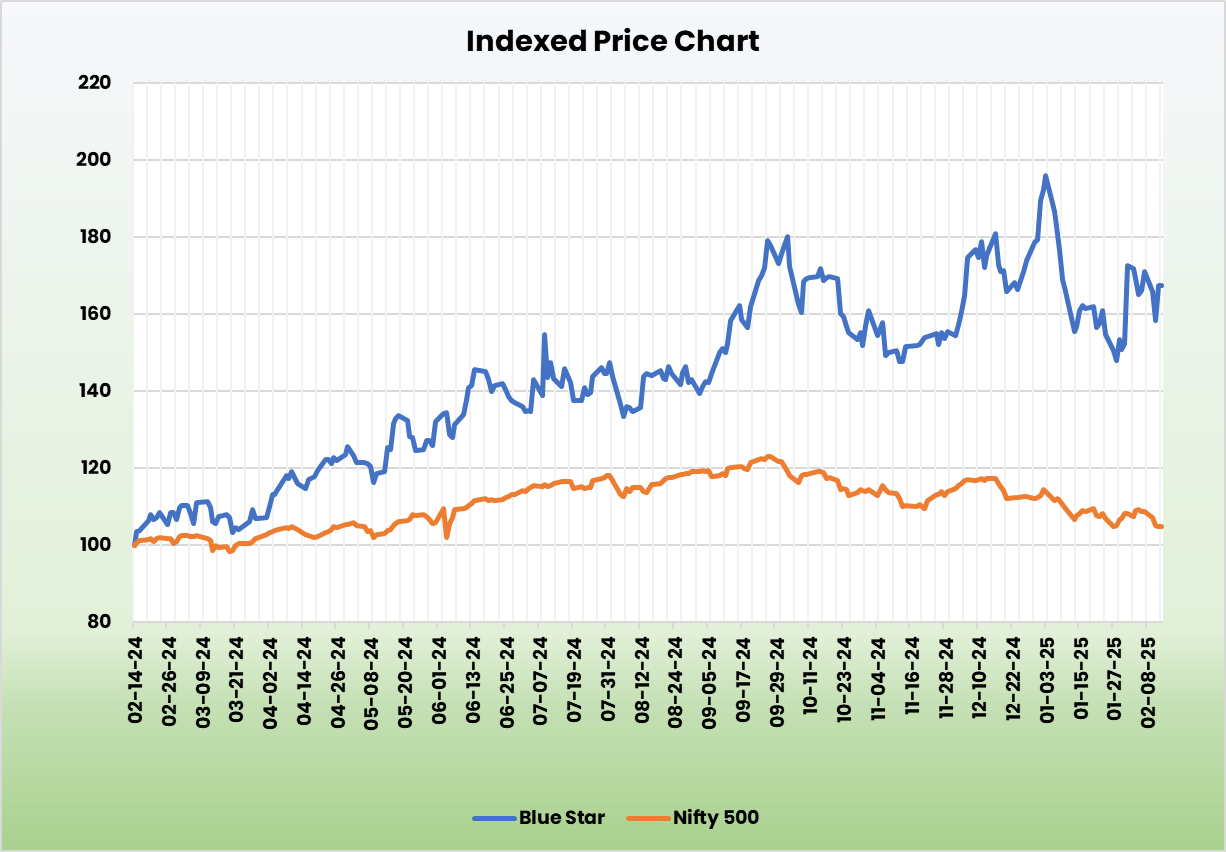

Blue Star Ltd – Built on Trust

Incorporated in 1943 and headquartered in Mumbai, Blue Star Ltd. is India’s leading Heating, Ventilation, Air Conditioning and Commercial Refrigeration (HVAC&R) company. It is also a major player in the Mechanical, Electrical, Plumbing, and Firefighting (MEP) space offering turnkey solutions for buildings, factories, data centers, infrastructure, heavy industry and water distribution projects. Currently Blue Star exports its products to 18 countries in the Middle East, Africa, SAARC, and ASEAN regions. As of 31 March 2024, the company has 7 state-of-the-art manufacturing facilities across Himachal Pradesh, Dadra, Ahmedabad, and Wada, including the company’s 100% subsidiary Blue Star Climatech Limited’s Sri City facility.

Products and Services

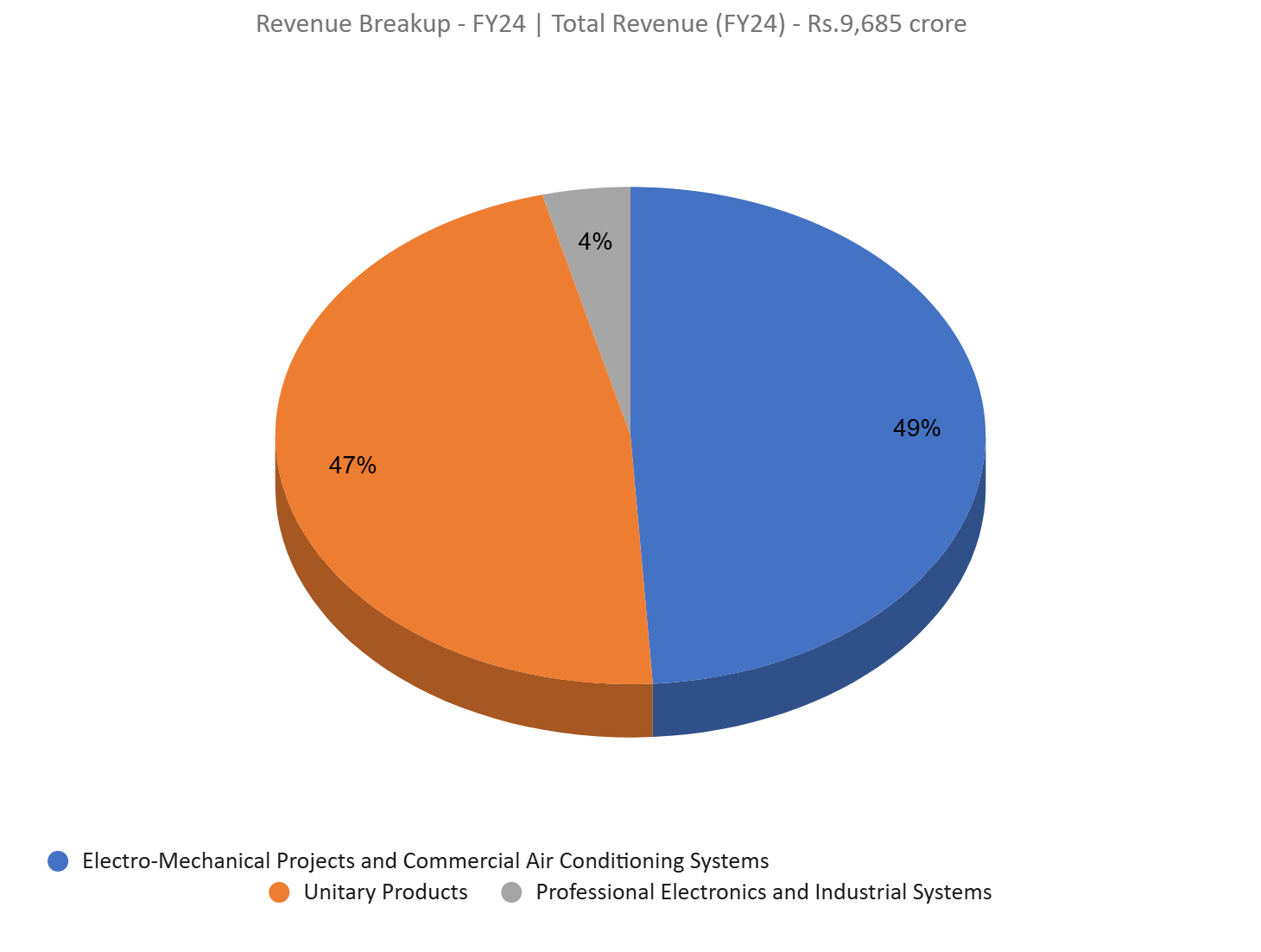

The company offers wide range of products such as inverter split AC, window AC, air and water coolers, air purifiers, portable AC, water purifiers, VRF V plus system, heat pumps, commercial refrigeration, cold storage, screw & scroll chiller, bottled water dispenser, ice lined refrigerator, freezers, cold rooms etc. The company operates majorly in 3 business segments – Electro-Mechanical Projects and Commercial Air Conditioning Systems (Segment 1), Unitary Products (Segment 2) & Professional Electronics and Industrial Systems (Segment 3).

Subsidiaries: As of FY24, the company has 10 subsidiaries and 2 joint ventures.

Investment Rationale

- Established position – Blue Star is a market leader in both conventional and inverted ducted air-conditioning systems, and ranks among the top two players in the VRF and chiller product categories. The Unitary segment has shown exceptional growth, outpacing industry performance in the quarter. Segment revenue increased by 22% in Q3FY25, supported by a 100-basis point margin expansion. On the international front, the company is developing new products focused on decarbonization and energy efficiency for key OEMs in Europe and North America. Additionally, the company is in the second phase of expansion at its Sri City plant, aiming to boost its capacity from the current 300,000 units to 600,000 units, with further plans to expand the capacity to 16,00,000 units in a phased manner.

- Growth strategies – The company continues to expand its portfolio with new products and variants in FY24. In the room AC segment, the company launched 3 new variants in the inverter split ACs. The company has also launched super energy efficient & heavy duty ACs and new range of window and light commercial ACs. It also launched new value-added products such as smart ACs with wi-fi and voice command technologies, hot & cold as well as anti-virus ACs. In the commercial air conditioning division, the company has developed the sixth-generation top discharge VRF systems. It also launched new range of packaged air conditioners and centrifugal chillers. The company has also expanded its offerings in deep freezers to offer a comprehensive range from 300L to 600L to smaller capacity models in the range of 60L to 200L.

- Q3FY25 – Revenue for the quarter was Rs.2,807 crore compared to Rs.2,241 crore during Q3FY24, representing a growth of 25%. EBITDA was at Rs.209 crore an increase of 35% compared to the Rs.155 crore of Q3FY24. The company reported net profit of Rs.132 crore marking an increase of 32% compared to the Rs.100 crore of the corresponding quarter in the previous year. Benefitting from the strong festive demand, the room AC business continued its strong growth trajectory. The carry forward order book stood at a record Rs.6,802 crore, a 13% YoY growth.

- FY24 – The company generated revenue of Rs.9,685 crore, an increase of 21% compared to FY23 revenue. Operating profit is at Rs.665 crore, up by 35% YoY. The company posted net profit of Rs.414 crore, an increase of 3% YoY.

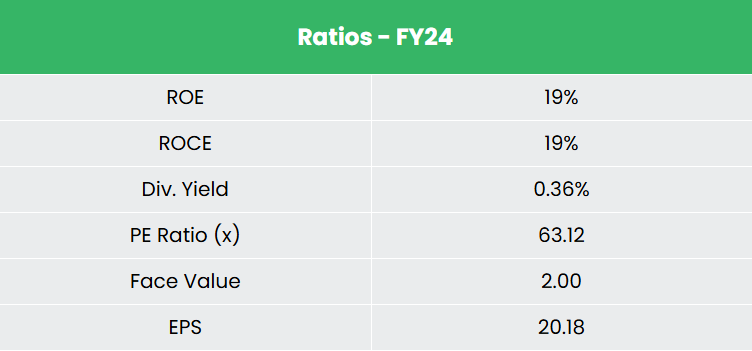

- Financial performance – The company has generated revenue and PAT CAGR of 31% and 78% over the period of 3 years (FY21-24). Average 3-year ROE & ROCE is around 21% and 24% for FY21-24 period. The company has a robust capital structure with a debt-to-equity ratio of 0.13.

Industry

White goods or consumer durables industry encompass significant household appliances including air conditioners, LED lights, refrigerators, dishwashers, freezers, coolers etc. The market is broadly segregated into urban and rural markets and is attracting marketers from across the world. Rural sector presents the next significant growth potential for the industry, driven by increased penetration. The industry is expected to experience an accelerated demand with rising disposable income, easy access to credit, and wide usability of online sales. The Indian room air conditioner market is projected to reach Rs.50,000 crore (US$ 5.6 billion) by FY29.

Growth Drivers

- 100% FDI allowed in the electronics hardware-manufacturing.

- The reduction in the tax burden in the 2025-26 Union Budget is expected to boost spending among the expanding middle class population.

- The government’s rural electrification efforts have improved power supply in tier 3/4 towns and villages, enabling the use of electrical products.

Peer Analysis

Competitors: Whirlpool of India Ltd, Johnson Controls-Hitachi Air Condition. India Ltd, etc.

Among the competitors listed above, Blue Star stands out with superior return ratios and more consistent revenue growth, reflecting the company’s financial stability and its ability to generate income and returns from invested capital efficiently.

Outlook

The company aims to achieve a 15% market share and maintain an 8.5% operating margin. It plans to invest Rs.750-800 crore over the next 3 years in manufacturing, product development, and digitalization. The company targets a 25% growth in Segment 1 and over 20% growth in Segment 2 for FY25. It is focused on expanding manufacturing capacity, boosting R&D, and advancing digitalization to support growth and profitability. Its prudent cash management supports moderate net borrowing and a healthy debt-to-equity ratio.

Valuation

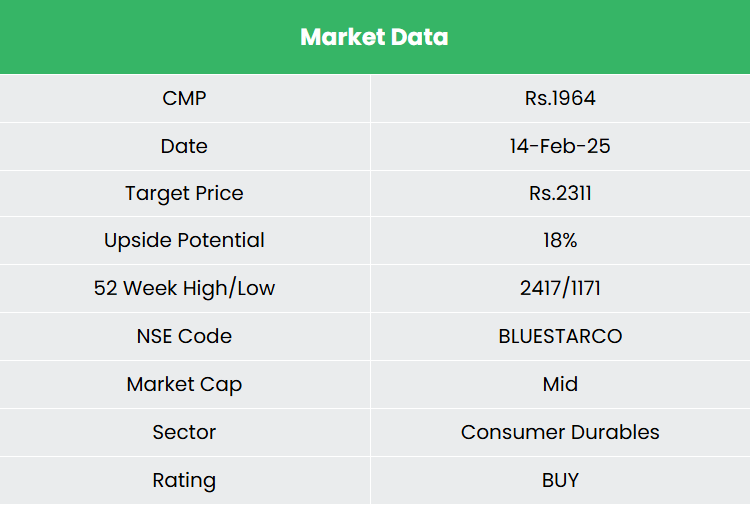

The company aims for significant profit growth by focusing on cost management, optimizing its product portfolio, expanding offerings, and entering new market and customer segments. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,311, 65x FY26E EPS.

Risk

- Seasonality Risk – Majority of the products sold by the company is seasonal in nature. Unforeseen weather patterns such as extended winter, pleasant summer, less than normal monsoon, excess monsoon, or any kind of disruptions during the peak selling seasons may lead to either a stock-out or excess inventory situation and impact revenue growth.

- Supply chain constraints – The company might face challenges in meeting demand, controlling costs and maintaining operational efficiency if there is any limitation or disruption in supply chain.

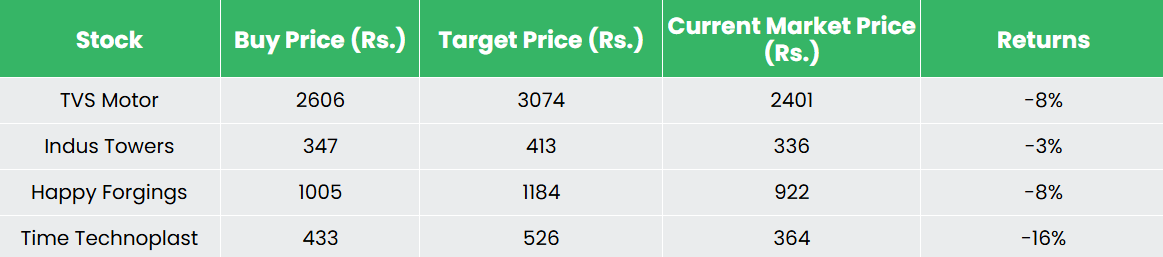

Recap of our previous recommendations (As on 14 February 2025)

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.