If you were asked to name an investment option that will allow you to put small sums on a regular basis, recurring deposits of banks would be the one on top of your mind. Small monthly sums, interest compounded quarterly at FD interest rates, no TDS and a lump sum at the end of the tenure – it’s all a neat proposition, no doubt.

But did you know that the returns turn out to be not so lucrative once the taxman takes a slice off your interest income pie? Yes, post-tax returns of recurring deposits (RD interest is very much taxable, in case you thought otherwise) can be quite unattractive. But here’s a good supplement that not only generates better returns over the long term but is far more tax efficient.

Welcome to the world of income funds – a class of debt mutual funds.

Suitability

If you had a minimum of 2-3 year investment time frame and wish to invest small sums regularly, a systematic investment plan (SIP) in income funds would be a good option. Income funds invest in a diverse basket of debt instruments that include certificates of deposits of banks, treasury bills, commercial papers, bonds and debentures of top-rated companies as well as government securities (called gilts).

That means they provide exposure to myriad debt instruments with varying risk-return profile and maturity. Income funds try to get the best of the underlying instruments by shifting their portfolios in line with interest rate cycles.

Even as they generate accrual income (which comes from holding the instrument till its maturity), they also seek capital appreciation by selling instruments when prices rally. This is one reason why their return potential is enhanced when compared with traditional debt products.

Income funds are also highly liquid, unlike RDs. They allow you to withdraw money any time you seek to.

Yes, income funds are market linked. That means their returns are not guaranteed or fixed, the way your recurring deposit interest is. It also means that their risk profile is higher than RDs.

But just to illustrate the kind of returns they generate, we took a 3-year monthly RD (invested 3 years ago at the rate of 8.75% prevailing then) and compared it with an SIP in the income funds from FundsIndia’s Select funds’ list. We took a period of 36 months ending June 30, 2013.

The table below illustrates the final sum you would have generated by investing Rs 4,000 a month for 36 months in an RD and Rs 1000 each in FundsIndia’s select list of 4 income funds.

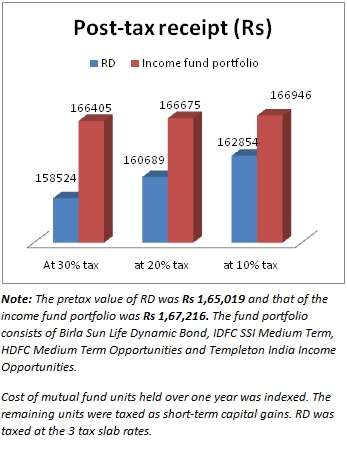

On the face of it, the difference in the final sum you receive will not seem very high at about Rs 2000. The pre-tax IRR works out to 9.9% for our portfolio against 9.1% for RD.

But take a look at the post-tax returns in each tax slab – 10%, 20% and 30% in the graphic below. The gain in our portfolio is about Rs 8000 at the highest tax slab and Rs 4000 at the lowest.

Tax advantage

The above difference arises as a result of a key tax benefit available to debt funds – capital gains indexation benefit for units held more than a year. Simply put, if you held debt fund units for over one year, you are allowed to bring your cost of those units to the present value, using the cost inflation index declared every year.

The gain, post indexation, is taxed at 20%. Investors also have an option to simply pay a 10% tax on the gains without indexing the cost.

Units held for less than a year alone are taxed at your income tax slab rate.

As against this, all interest incomes from deposits are taxed at your slab rate. There is no capital gain benefit available to deposits. As a result, investors, especially in the higher tax bracket, benefit immensely on the tax front when they invest in instruments such as debt funds that enjoy capital gain benefits.

In a highly inflationary scenario the indexed cost is often higher than even the market value resulting in a notional capital loss. That means you do not get to pay any tax and the loss can be set off against any other long-term capital gain.

In the illustration provided, the units held for more than one year did not suffer any long capital gains tax as a result of a notional capital loss (although in reality you gained quite a good sum).

Liquidity, tax efficiency and superior returns make income funds a good supplement to RDs. If you are simply a RD investor, take a third of your monthly surplus kept aside for RD and start an SIP in an income fund. That way you will have a good mix of a guaranteed fixed return product like RD and at the same time, a better yielding product called income funds.

Go to our Select funds list to choose income funds under the category Debt funds – long term.

Vidya, compliments to you. Yet again, you have come up with a well written piece so simple and lucid yet very effectively communicated.

I can share my experience with investment in income funds. Last few years, I have had virtually no tax liability on the capital gains from income funds as the indexed adjusted capital gains were negative. The only hindrance, if I may say so is managing the information for tax computation and claiming benefits on indexed basis. This could be even more difficult when a SIP investment is withdrawn as capital gains will have to be calculated on each SIP. But I think the little pain is worth it as there is a second and major tax benefit. The notional loss can be set-off against short term capital gains say from equities/debt funds as well as long term capital gains from other assets like property and can also be carried forward for future set-off for 8 years.

Hello Mr Shenoy, thank you for sharing the information and your own experience. tks, Vidya

Dear Shenoy,

If the registrar is CAMS for your funds, they provide you capital gain statement with indexation and without indexation. Just go to camsonline.com and enter your e-mail id registered in the folio. Thats it….

I have not done this for Karvy and Franklin… so, no idea..

I thought Short term Capital Gains on shares sold cannot be adjusted at all from any loss?Am I wrong?

Hello Ramamurthy, Short-term capital loss can be set-off against an share term capital gain from the shares sold. Only, long-term capital gains from shares cannot be used for this purpose as LTCG is exempt. thanks

This is a very good strategy to play on the current debt mkt volatility. http://www.ddramanathan.blogspot.in

This is also a good time to invest in FMPs given the steepness at the shorter end of the yield curve.

Vidya, compliments to you. Yet again, you have come up with a well written piece so simple and lucid yet very effectively communicated.

I can share my experience with investment in income funds. Last few years, I have had virtually no tax liability on the capital gains from income funds as the indexed adjusted capital gains were negative. The only hindrance, if I may say so is managing the information for tax computation and claiming benefits on indexed basis. This could be even more difficult when a SIP investment is withdrawn as capital gains will have to be calculated on each SIP. But I think the little pain is worth it as there is a second and major tax benefit. The notional loss can be set-off against short term capital gains say from equities/debt funds as well as long term capital gains from other assets like property and can also be carried forward for future set-off for 8 years.

Hello Mr Shenoy, thank you for sharing the information and your own experience. tks, Vidya

Dear Shenoy,

If the registrar is CAMS for your funds, they provide you capital gain statement with indexation and without indexation. Just go to camsonline.com and enter your e-mail id registered in the folio. Thats it….

I have not done this for Karvy and Franklin… so, no idea..

I thought Short term Capital Gains on shares sold cannot be adjusted at all from any loss?Am I wrong?

Hello Ramamurthy, Short-term capital loss can be set-off against an share term capital gain from the shares sold. Only, long-term capital gains from shares cannot be used for this purpose as LTCG is exempt. thanks

This is a very good strategy to play on the current debt mkt volatility. http://www.ddramanathan.blogspot.in

This is also a good time to invest in FMPs given the steepness at the shorter end of the yield curve.

Vidya, “Income Funds” and “Dynamic Bond” funds are mentioned in same category, so are they same?

Hi Sheetal, Yes, dynamic bond funds are nothing but a sub-set of income funds. Income funds is a very broad term used for funds that seek income accrual even as they scout for capital appreciation. Tks.

Vidya, “Income Funds” and “Dynamic Bond” funds are mentioned in same category, so are they same?

Hi Sheetal, Yes, dynamic bond funds are nothing but a sub-set of income funds. Income funds is a very broad term used for funds that seek income accrual even as they scout for capital appreciation. Tks.

many a times these are interchangeably used causing confusion among investors. thanks for the enlightenment. http://www.ddramanathan.blogspot.in

many a times these are interchangeably used causing confusion among investors. thanks for the enlightenment. http://www.ddramanathan.blogspot.in

I am not sure it would be a wise option to invest in Income funds with a 2-3 year horizon.

Given the volatility of the markets in recent times one would be better off to stick to RD.

At least you can protect your capital.

But Yes with someone with an horizon of 5 years and above SIP in Income Funds is a way to go.

Rakesh

I am not sure it would be a wise option to invest in Income funds with a 2-3 year horizon.

Given the volatility of the markets in recent times one would be better off to stick to RD.

At least you can protect your capital.

But Yes with someone with an horizon of 5 years and above SIP in Income Funds is a way to go.

Rakesh

Thanks Vidya ji for this article.

Though the concept isn’t new, the recent developments brings jitters for new investors like me.

The immediate future seems uncertain as of now.

My portfolio containing dynamic bond funds are in the red.

I don’t know how many people will be able to stomach this.

How long do you think is this volatility going to last?

hello hari, We have to take the volatility only as events unfold. Rupee’s stablity and near term liquidity pressure from advance tax payment (due mid September) will ensure that uncertainty remains for now. tks.

Two queries for you vidya ji

A. How important is the AUM when choosing a debt fund?

B. Many advised me to opt for arbitrage fund than a debt fund. Your views on that..

Hello Hari,

1. AUM is important for liquidity. In periods when debt funds have to actively take calls, such as the current period, this becomes important.

2. Arbitrage funds cannot be substitute for debt, simple because they have a tax edge. The returns of well managed debt funds, especially when rate cycles are turning can beat arbitrage. Arbitrage funds are good to hold with the idea of hedging a portfolio.

Thanks.

Vidya Ji,

What happens to income funds during increasing interest rate period?

Will they suffer losses?

hello hari, A well managed income fund will not suffer if the interest rate hike is gradual. Income funds can mostly straddle over various instruments and time frames. hence it a rising interest rate scenario, they tend to keep their portfolio maturities short, get accrual income and make gains.

Look at the returns of income funds in years such as 2009 and 2011. But in year such as 2009 when the rate hike was unexpected, funds that held too much gilt woudl have suffered a bit but usually bounce back.Chances are that long gilt funds willf ace losses in an unexpected rate hike move. Thanks.

Hi Vidya, I have another question – what would be the impact on Income and Gilt funds if the INR keeps going up against the dollar? If these are risky assets during such a phase which debt fund would be more suitable in the mentioned context? Thanks.

Hello Sheetal,

The rupee movement does not directly affect the bond rates. if the rupee keeps going up, the Central Bank would take measures that amount to higher rates. That in turn will make bond market volatile and increase yields of short-term instruments. In such an uncertain scenario, holding to ultra short funds or FMPs with a 1-year maturity (esp when you cannot take volatility) may be an option. But if you are holding income funds currently with a long-term view, it may be better not to disturb them Opportunities in these funds are immense as and when rates reverse. Thanks, Vidya

Thanks Vidya ji for this article.

Though the concept isn’t new, the recent developments brings jitters for new investors like me.

The immediate future seems uncertain as of now.

My portfolio containing dynamic bond funds are in the red.

I don’t know how many people will be able to stomach this.

How long do you think is this volatility going to last?

hello hari, We have to take the volatility only as events unfold. Rupee’s stablity and near term liquidity pressure from advance tax payment (due mid September) will ensure that uncertainty remains for now. tks.

Vidya Ji,

What happens to income funds during increasing interest rate period?

Will they suffer losses?

hello hari, A well managed income fund will not suffer if the interest rate hike is gradual. Income funds can mostly straddle over various instruments and time frames. hence it a rising interest rate scenario, they tend to keep their portfolio maturities short, get accrual income and make gains.

Look at the returns of income funds in years such as 2009 and 2011. But in year such as 2009 when the rate hike was unexpected, funds that held too much gilt woudl have suffered a bit but usually bounce back.Chances are that long gilt funds willf ace losses in an unexpected rate hike move. Thanks.

Hi Vidya, I have another question – what would be the impact on Income and Gilt funds if the INR keeps going up against the dollar? If these are risky assets during such a phase which debt fund would be more suitable in the mentioned context? Thanks.

Hello Sheetal,

The rupee movement does not directly affect the bond rates. if the rupee keeps going up, the Central Bank would take measures that amount to higher rates. That in turn will make bond market volatile and increase yields of short-term instruments. In such an uncertain scenario, holding to ultra short funds or FMPs with a 1-year maturity (esp when you cannot take volatility) may be an option. But if you are holding income funds currently with a long-term view, it may be better not to disturb them Opportunities in these funds are immense as and when rates reverse. Thanks, Vidya

Two queries for you vidya ji

A. How important is the AUM when choosing a debt fund?

B. Many advised me to opt for arbitrage fund than a debt fund. Your views on that..

Hello Hari,

1. AUM is important for liquidity. In periods when debt funds have to actively take calls, such as the current period, this becomes important.

2. Arbitrage funds cannot be substitute for debt, simple because they have a tax edge. The returns of well managed debt funds, especially when rate cycles are turning can beat arbitrage. Arbitrage funds are good to hold with the idea of hedging a portfolio.

Thanks.