The good news from the RBI’s first bi-monthly monetary policy is that if inflation behaves as per expectations, RBI may not feel the need to hike rates. But the not so good news is that neither is the RBI in a hurry to cut rates, at least not based on short-term rosy pictures painted by inflation and other economic indicators.

The good news from the RBI’s first bi-monthly monetary policy is that if inflation behaves as per expectations, RBI may not feel the need to hike rates. But the not so good news is that neither is the RBI in a hurry to cut rates, at least not based on short-term rosy pictures painted by inflation and other economic indicators.

The RBI kept the repo rate and CRR unchanged on April 1, even as it tweaked the borrowing available in the overnight call money market.

The Central Bank halved the liquidity available under the overnight call market from 0.5% to 0.25% of each bank’s Net Time and Demand Liability (NDTL). But it increased the liquidity under the 7-day and 14-day term repo to 0.75% from 0.5%.

The takeaway for you as an investor is that bond markets are not expected to be volatile from the move. That said, your opportunities still remain ripe in the short-to-medium term debt fund category, as written by us during the previous monetary policy in January 2014. You can click here to read our note.

So what is the RBI Governor conveying to the markets? That it is going to take a long-term approach – to inflation, to liquidity and to attract foreign inflows. The following moves suggest this:

- One, it is now evident that RBI’s monetary policy decisions will not simply be based on transient one off data points – such as a fall in inflation here or a pick up in IIP there. Rather, trends or averages in data points such as consumer inflation or core inflation will become driving factors for rate cuts or rate hikes, as the need arises.

- Two, the RBI appears to be doing a very fine balancing act of managing liquidity, and at the same time, ensuring that policy impulses are felt across the interest rate spectrum.

- It is to this extent that the RBI reduced the availability of the overnight call money market that gives a more guaranteed or pre-set access to funds for banks and instead, shifted more focus to longer windows through term repos. This would mean that increasingly, the impact of liquidity will be felt actively in instruments such as 1-month CDs.

- The RBI appears to be working towards reducing the kind of volatility in FII flows that was witnessed in mid-2013.

Allowing FIIs to hedge their currency risk using currency futures in domestic exchanges and the proposal to allow foreign investors to hedge their coupon (interest) receipts falling due over the next 12 months are efforts to this end. It is noteworthy that the FII flows into the debt market has been robust in 2014 thus far.

What it means to you

The RBI’s ‘gliding path’ approach to disinflation means that we may not be able to expect rate cuts any time soon given the elevated prices of vegetables, concerns over monsoon and high core inflation. The RBI has a CPI target of 8% by January 2015 and 6% by January 2016.

That means bond markets do not have too many reasons to fluctuate save for marginal movements. That said, lower availability of liquidity in the overnight call market could mean some return opportunities in liquid funds. But this may not be significant. Also, higher tapping of 14-day term repos would influence rates of 1-month CDs. It is noteworthy that CD and CP rates have been on the decline, triggering some price rally.

Investors would do well to remain with short-term funds that could provide sufficient opportunities at this juncture. Longer-dated bonds have not received any signal from the policy, for any kind of price rally, and may not in the near future.

Funds to hold now

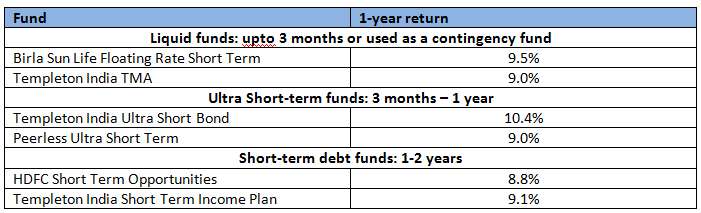

Liquid funds remain attractive: As recommended by us last time, we stick to Birla Sun Life Floating Rate Short Term and Templeton India Treasury Management (TMA) remain our picks in the liquid fund category based on their consistent record and very low maturity profiles.

We believe with the overnight repo liquidity being reduced, there could be some marginal spike in rates in this segment and an accrual strategy, which is followed by liquid funds, would ensure that you gain from slightly higher yields in the short term.

Use liquid funds to either park money temporarily or for creating a contingency fund. If you receive a hefty sum post your performance appraisal this month and remain undecided where to invest or use it, park it in liquid funds. This remains your best bet in terms of returns with least risk until you find a purpose for the money.

Ultra short-term funds: If you have a slightly longer duration of say over 3 months, then this category of funds would fit your requirement. We continue to like Templeton India Ultra Short Bond Fund in this space. Peerless Ultra Short Term Fund is an option for those with a slightly higher risk profile, given its longer maturity and of course higher yield to maturity.

Short-term debt funds: In this category, we would like to slightly tweak our approach to focus a bit more on funds that invest in corporate bonds as opposed to primarily CDs and CPs. While a portfolio with CPs and CDs will certainly hold a lower risk profile, we think the recent dip in yields in this category has already provided some returns.

From our policy-related recommendation in January 2014, we retain HDFC Short Term Opportunities, but add Templeton India Short Term Income Plan. Both the funds have higher exposure to corporate CDs, with the HDFC fund sporting more AAA-rated bonds while the Tempeton fund has higher weight to AA-rated bonds. The yield to maturity and average maturity of the Templeton fund is higher, and therefore its risk profile is a notch higher.

If you are wondering what you should do if you had a longer-term view, we will, in the forthcoming weeks, have a call on long-term debt funds that have an accrual strategy and seek to keep volatility related to rates low. Given the elevated rate regimen we seem to be in for, we think this strategy could work to deliver. Look out for our weekly call on this.

Hi Vidya,

Could you please share a couple of lines on BSL FRF Long Term Plan w.r.t. this recent policy updates.

Thanks,

Mustafizur

hello Rahaman, Sorry for the delayed response. It remains a good fund but with short-term yields coming off a bit, past returns may not repeat itself. thanks, Vidya

One more point to add. 2 months back, I had done my financial planning from FI & I was advised Templeton India Ultra Short Bond & HDFC Cash Management Savings Fund. Now, I don’t see HDFC fund appearing in this list & I did not find it either previously also in your blog. I understand that there are good funds outside this list & liquid funds selection keeps on varying in every 3-6months. But don’t you think as an investor it is confusing for me to have been recommended for a fund which I don’t find in your list :)?

I want 2 funds for the emergency corpus purpose, that liquidity is a very important aspect but I don’t have a fixed time frame. It is more of, I have a X target, I will keep on accumulating till X is reached & that fund will remain there, I will withdraw only when there is a need, otherwise it would be untouched.

hello Rahaman, the funds you mentioned remain good bets. As you will know, not all good funds can be featured in a Select list. Also, it is important for advisors to help investors choose funds that can also be used for transfers etc. easily. hence the choice of HDFC may be there in your case. At fundsIndia we do not believe in ‘top funds’ and prefer to customise portfolio as far as possible (within the research mandate) to suit individual needs. but when we give a general call, it is more strategic in nature and based on ‘point in time’ analysis.

This is because with liquid funds, especially, the portfolio is of such short duration, it is simply not possible to extend the current portfolio into future as the instruments available later will be entirely different. While the HDFC fund mentioned by you remains consistent, these 2 funds mentioned by us in the article, have certainly outperformed a wee bit with higher yielding instruments in recent times. As an investor, with liquid options, it may be best not to try chase returns as it would involved literally churning portfolio every 3 months. It is also not something we favour. What you can do as an investor in such funds is check with your advisor on a half yearly basis or so (for short-term funds) on whether the fund performance is worthy of continuing. thanks, Vidya

What about investing in liquid fund. Is there any downside risk associated with it. Why i am asking this question is, I have invested Rs 1 lac in Sbi dynamic bond fund and have lost 2500 as of now. I thought bond was safe before investing

Hello Sir,

Debt funds have widely varying risk profiles. Liquid being the least and income/dynamic and gilt funds being higher risk. of these, those with higher maturity profile are risky in a rising rate scenario. hence, your choice of SBI hurt you. Such funds are meant for longer holding periods only and will have volatility. thanks, Vidya

I am invested in IDFC dynamic bond fund (Direct Plan-Growth). I have just completed 1 year since investment and would like to know if I should switch to some other type of Income/liquid/debt fund at this point of time?

What would be the tax treatment of the gains (only about 5%) since i have been invested for over an year

Hello Vikas,

Your time frame would be important for us to let you know the choice of funds. Since you have an activated FundsIndia account, I shall ask one of our advisors to get in touch with you for details so that we can make the right suggestion. Debt investments made over 1 year will have capital gains indexation benefit. You will pay long-term capital gains tax at 10% without indexation or 20% with indexation. It is your choice whether to go for indexation or not.

Also, pl. note our portfolio advice and review are for investments made through the FundsIndia platform.

thanks, Vidya

One more point to add. 2 months back, I had done my financial planning from FI & I was advised Templeton India Ultra Short Bond & HDFC Cash Management Savings Fund. Now, I don’t see HDFC fund appearing in this list & I did not find it either previously also in your blog. I understand that there are good funds outside this list & liquid funds selection keeps on varying in every 3-6months. But don’t you think as an investor it is confusing for me to have been recommended for a fund which I don’t find in your list :)?

I want 2 funds for the emergency corpus purpose, that liquidity is a very important aspect but I don’t have a fixed time frame. It is more of, I have a X target, I will keep on accumulating till X is reached & that fund will remain there, I will withdraw only when there is a need, otherwise it would be untouched.

hello Rahaman, the funds you mentioned remain good bets. As you will know, not all good funds can be featured in a Select list. Also, it is important for advisors to help investors choose funds that can also be used for transfers etc. easily. hence the choice of HDFC may be there in your case. At fundsIndia we do not believe in ‘top funds’ and prefer to customise portfolio as far as possible (within the research mandate) to suit individual needs. but when we give a general call, it is more strategic in nature and based on ‘point in time’ analysis.

This is because with liquid funds, especially, the portfolio is of such short duration, it is simply not possible to extend the current portfolio into future as the instruments available later will be entirely different. While the HDFC fund mentioned by you remains consistent, these 2 funds mentioned by us in the article, have certainly outperformed a wee bit with higher yielding instruments in recent times. As an investor, with liquid options, it may be best not to try chase returns as it would involved literally churning portfolio every 3 months. It is also not something we favour. What you can do as an investor in such funds is check with your advisor on a half yearly basis or so (for short-term funds) on whether the fund performance is worthy of continuing. thanks, Vidya

Hi Vidya,

Could you please share a couple of lines on BSL FRF Long Term Plan w.r.t. this recent policy updates.

Thanks,

Mustafizur

hello Rahaman, Sorry for the delayed response. It remains a good fund but with short-term yields coming off a bit, past returns may not repeat itself. thanks, Vidya

What about investing in liquid fund. Is there any downside risk associated with it. Why i am asking this question is, I have invested Rs 1 lac in Sbi dynamic bond fund and have lost 2500 as of now. I thought bond was safe before investing

Hello Sir,

Debt funds have widely varying risk profiles. Liquid being the least and income/dynamic and gilt funds being higher risk. of these, those with higher maturity profile are risky in a rising rate scenario. hence, your choice of SBI hurt you. Such funds are meant for longer holding periods only and will have volatility. thanks, Vidya

I am invested in IDFC dynamic bond fund (Direct Plan-Growth). I have just completed 1 year since investment and would like to know if I should switch to some other type of Income/liquid/debt fund at this point of time?

What would be the tax treatment of the gains (only about 5%) since i have been invested for over an year

Hello Vikas,

Your time frame would be important for us to let you know the choice of funds. Since you have an activated FundsIndia account, I shall ask one of our advisors to get in touch with you for details so that we can make the right suggestion. Debt investments made over 1 year will have capital gains indexation benefit. You will pay long-term capital gains tax at 10% without indexation or 20% with indexation. It is your choice whether to go for indexation or not.

Also, pl. note our portfolio advice and review are for investments made through the FundsIndia platform.

thanks, Vidya