With market mood turning somber and a potential slide in the offing, it’s a good time to discuss how your fund manages bearish markets. How well a fund contains losses in a market downturn is rather more important than how well it does when markets climb. Why? Because it takes a lot of effort to just recover the losses. And it’s only after this that gains can be made.

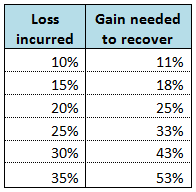

Take a look at the table alongside.

Say you invested Rs 50,000 in Fund A. But as markets bled, it lost 20 per cent. The fund then bounced back with a 35 per cent gain when sentiments turned, doing much better than the broad market. But 25 per cent would be needed to just recover what you lost. Only gains beyond this would help you make money on your investment. In this case, the 35 per cent rise will bring your investment to Rs 54,000. The gain you will actually be sitting on after the market rise works out to 8 per cent.

That puts a Fund B that lost 10 per cent in a better position, as it has a smaller loss to recoup. Fund B can thus quickly recover and deliver returns even if its performance in the market uptick doesn’t quite match up to Fund A. Assume Fund B gains 25 per cent. Your returns at the end would be at 12.5 per cent.

To consider a real-time example, in the mid-cap fuelled 2012 rally, funds such as HSBC Midcap Equity or Principal Emerging Bluechip comfortably beat their category averages by 3-4 percentage points. But in the 2011 market downturn, they had had steeper losses than their category to the tune of 9-20 percentage points. Overall gains across the two cycles were thus lower by 16-37 percentage points than peers such as SBI Magnum Global or Canara Robeco Emerging Equities, which didn’t gain as much but then, didn’t lose as much either.

Look for protection

Therefore, a fund that tops the charts in bull markets will not be of much use if it is at the bottom of the heap during bearish phases. For one, it will cap the overall return you make as the recovery from losses swallows a good chunk of the gain. Besides, in order to deliver the high returns needed, the fund may take riskier bets. This feeds back into the problem, since the tendency would be to pick stocks that are the flavor of the market. Such stocks can sink quickly when they aren’t fancied anymore. Two, the effect of compounding of returns reduces when losses are steep. And three, swift rises and sharp falls increase a fund’s volatility and risk. It’s low volatile strategies that work best over the long term.

True. This is one reason why I prefer (and invest in ) a balanced fund as against a large-cap fund.

For example, HDFC Top 200’s annualized returns for 1, 2, 3 and 5 yeas are -1.9%, 24.6%, 15.6%, and 7.9% respectively; whereas those of HDFC Balanced fund’s are: 9.0%, 32.7%, 20.4% and 14.0% respectively (as on September 15, 2015). The returns are truly based on how the fund contains losses in a falling market than a gains in a rising market.

If someone is investing with a 25 year horizon for accumulating wealth, then such comparison still matter. Which fund would you suggest. HDFC Top 200 Vs HDFC Bal

As marked by Vijay, HDFC Bal knocked out Top 200. Why is that

Hi Rohit,

Apologies for the delayed reply. HDFC Top 200 is a pure equity fund, with no debt component. Its heavy dependence on bank stocks (State Bank of India and ICICI Bank) has hurt its recent performance; the fund is also tilted more towards cyclical sectors such as energy, capital goods, power, and construction which have seen their stock market run slow. The fund tends to take longer term view of sector and stock prospects. HDFC Balanced fund is not directly comparable to HDFC Top 200, as it is in a completely different category and risk profile. This fund benefited from both the equity and the debt rally. Hope this helps.

Thanks, Bhavana

Thanks Bhavana for your reply. Valid point.

Can you answer this: If someone is investing with a 25 year horizon for accumulating wealth and an aggresive investor, then such comparison still matter. Which fund would you suggest. HDFC Top 200 Vs HDFC Bal

Hi Rohit,

A balanced fund aims at containing risk and downsides. For an aggressive investor, especially one who has a horizon of 25 years can stay invested in equities and won’t really need a balanced fund at all. That said, whether or not HDFC Top 200 (or HDFC Balanced) has to be invested in depends on what other schemes are already held and how much the investment is, besides other factors.

Thanks,

Bhavana

If someone is investing with a 25 year horizon for accumulating wealth, then such comparison still matter. Which fund would you suggest. HDFC Top 200 Vs HDFC Bal

As marked by Vijay, HDFC Bal knocked out Top 200. Why is that

Hi Rohit,

Apologies for the delayed reply. HDFC Top 200 is a pure equity fund, with no debt component. Its heavy dependence on bank stocks (State Bank of India and ICICI Bank) has hurt its recent performance; the fund is also tilted more towards cyclical sectors such as energy, capital goods, power, and construction which have seen their stock market run slow. The fund tends to take longer term view of sector and stock prospects. HDFC Balanced fund is not directly comparable to HDFC Top 200, as it is in a completely different category and risk profile. This fund benefited from both the equity and the debt rally. Hope this helps.

Thanks, Bhavana

Thanks Bhavana for your reply. Valid point.

Can you answer this: If someone is investing with a 25 year horizon for accumulating wealth and an aggresive investor, then such comparison still matter. Which fund would you suggest. HDFC Top 200 Vs HDFC Bal

Hi Rohit,

A balanced fund aims at containing risk and downsides. For an aggressive investor, especially one who has a horizon of 25 years can stay invested in equities and won’t really need a balanced fund at all. That said, whether or not HDFC Top 200 (or HDFC Balanced) has to be invested in depends on what other schemes are already held and how much the investment is, besides other factors.

Thanks,

Bhavana

Can you please advice..

Thanks

My idea behind comparing a pure large cap fund to a balanced one was solely based on how each fund handles a downturn. The debt part in the balanced definitely provides a cushion during a bear run, and doesn’t have to work as hard as a large-cap to recover losses.

I invest in HDFC balanced via SIP. Remember to avoid any fund which is tilted to sector (as Bhavana explained Top 200 is).

Can you please advice..

Thanks

My idea behind comparing a pure large cap fund to a balanced one was solely based on how each fund handles a downturn. The debt part in the balanced definitely provides a cushion during a bear run, and doesn’t have to work as hard as a large-cap to recover losses.

I invest in HDFC balanced via SIP. Remember to avoid any fund which is tilted to sector (as Bhavana explained Top 200 is).

True. This is one reason why I prefer (and invest in ) a balanced fund as against a large-cap fund.

For example, HDFC Top 200’s annualized returns for 1, 2, 3 and 5 yeas are -1.9%, 24.6%, 15.6%, and 7.9% respectively; whereas those of HDFC Balanced fund’s are: 9.0%, 32.7%, 20.4% and 14.0% respectively (as on September 15, 2015). The returns are truly based on how the fund contains losses in a falling market than a gains in a rising market.