Yes, you’re right. Quite the opposite of the old market adage, Sell in May and go away! A 10% fall from the highs of end January (although only about 3% for this calendar year thus far) till the low on May 7, has led to many questions (mostly in media) on whether the equity rally is over, whether one should reduce exposure to equity or shift to debt and so on. When there is plenty of skepticism, especially driven by the media, our simple suggestion has been – stay put or invest.

So what has led to the somewhat sharp corrections we have been witnessing periodically in the last couple of months? And are these reasons enough to doubt the economic and corporate fundamentals? This is our take:

The following reasons (not an inclusive list) can broadly be attributed to the volatility seen in the last couple of months:

- Dent in FII sentiment as a result of levy of minimum alternative tax (MAT) with retrospective effect; even as FII money started moving to emerging markets

- Rising crude prices

- Weakness of the rupee against the dollar as a result of FII outflow and as well as a result of rising crude oil prices

- Expectation of yet another quarter of weak earnings with consensus per share earnings for already being downgraded sharply; besides initial forecast of a weak monsoon

- Gilts giving up their gains

Here’s why we think these factors should not be worrying you much at this point in time and should definitely not worry you as a long-term investor.

Outflow more tactical

First, on FII outflows. While we do think retrospective tax amendments are not a great move, especially when India in dependent on foreign flows; we think the government may come up with some reconciliatory moves as they are not oblivious to the fact that any significant foreign outflow can be detrimental. Having said that, the currently sell off by FIIs appear to be more tactical, arising from a profit booking strategy. After all, the impact of MAT will not be felt on current investments. They are for past transactions.

We think the sharp run up in Indian markets in the past 18 months jacked up valuations relatively, when compared with other emerging markets (EM), which significantly underperformed India in 2014. FIIs, having entered in late 2013, could have well found a ripe opportunity to not only book profits in India but redeploy in EMs (such as China, South Korea or Taiwan where valuations are lower) based on a relative valuation call.

That said, nothing changes the relative fundamental position of India vis-a-vis its peers in terms of both improving economic and political situation. This is also acknowledged by the improving rating and outlook of India by international agencies.

Rising crude prices

Rising by $15-20 a barrel in a short span, the jump in crude oil price has been too much, too soon – questioning its sustainability, in our view.

The unrest in Libya, where oil exports reduced below 5,00,000 barrels per day (that’s a third of its output until 2010), civil unrest in Yemen, causing fear of disruption of oil supplies from other oil-producing nations, rise in price of oil by Saudi Arabia for supplies made to US and parts of Europe and of course draw down in stock piles in US have all led to the galloping price of crude.

Despite all of the above, it is noteworthy that the world has 487 million barrels of oils sitting in storage currently and according to reports that is an 80-year high inventory, still. OPEC nations are said to be pumping in supplies that is at least 2 million barrels a day higher than the demand. And with the prices crossing $60 a barrel – a magic figure for shale, it may be hard for US shale drillers not to resume. That means new drilling and those from unfinished wells could well resume.

In other words, even a range bound pricing for some time and settling of geo political issues could mean only downward pressure on the oil, if one viewed it for fundamental reasons. In the near term, big bets on oil futures could well swing prices, no doubt. But remember, we are talking of the long term prospects for your investments.

Depreciating rupee and rising gilt

At its lowest in over a year and a half now, the rupee’s weakness against the US dollar is seen as a result of less favourable retrospective tax issues for FIIs as well as a global debt sell off. However, the rupee still appears to be a relatively stable currency compared with peers.

Consider this: the rupee has fallen 2-3% against the dollar in the past 6 months as against 10% depreciation seen many emerging market currencies. If the rupee did not correct, it would make India less competitive with its emerging market exporting peers, whose currency has fallen significantly.

While it is true that debt market pressure in both US and parts of Europe has led to pressure in local gilts as well, the correction is positive when seen from an export-competitiveness perspective. Given how India is yet to see firm pick up in exports, the rupee in its current range could be much helpful. And remember, in the long term, most analysts do not predict a strong rupee against the dollar.

What we do not want is a swinging, volatile rupee. Any excessive weakness can always be handled by the RBI (as demonstrated in 2013) through selling dollars, given our comfortable foreign exchange reserves.

As retail investors, it would therefore be too much to worry about the rupee at this stage. Remember, your international investments (international funds and so on) too stand to gain from a weakening rupee!

The fall in gilt prices (rising yield) too is entwined with rising oil prices, currency issues as well as the global debt market, especially Germany. But is that something for markets to fear? We do not think so; at least not over the medium term if you consider this: the RBI is now on CPI-based target with real rate as an additional focus.

If we do achieve the 4% inflation target, then bond yields will reduce as it is hard to imagine a real rate of 3-4% (real rate is the excess return over inflation)! Now, forget the external risks, which are more sentimental is nature.

The internal risk is that of poor monsoon and higher food prices as these could only trigger inflation and prevent fall in yields. It is noteworthy that we have been through a year of below-average monsoons as well as unseasonal rains at a time when the government was tackling a much higher inflation number than we are at present. And it would be fair to say that it was tackled well; if the fall in food prices from their peak is any evidence.

Therefore, it one were to assume there are no big shocks to inflation, over the medium term, fall in yields in line with lower inflation may seem inevitable; much as yields remain stubborn today.

Earnings – still in expectation mode

We have, early this year, stated that unlike 2014, 2015 will be a stock-specific rally, based on earnings and we see that panning out now.

While some of the index companies have delivered strong numbers, early trend suggests that we could have yet another lack lustre earnings season for the broad market. This has led to almost a 6.-8% downgrade in earnings estimate by many analysts. Where does that leave us? At more comfortable levels; taking into account the market correction as well.

That leaves us with an about 15% earnings growth estimate over 2 years (FY16 and FY-17). The current forward valuations at 15-16 times P/E does appear to be in line with the growth outlook. But that also means not much upside for the year until earnings improve.

And when can you expect earnings to improve? Stage 1: When lower input costs and interest costs show up in the numbers. Stage 2: when revenue pick up significantly as a result of higher investments/capacity additions. We think stage 2 is well over a year away. But stage 1 is already visible in some companies and can be expected to be making itself conspicuous before the end of the fiscal. Either which way you need to wait a bit.

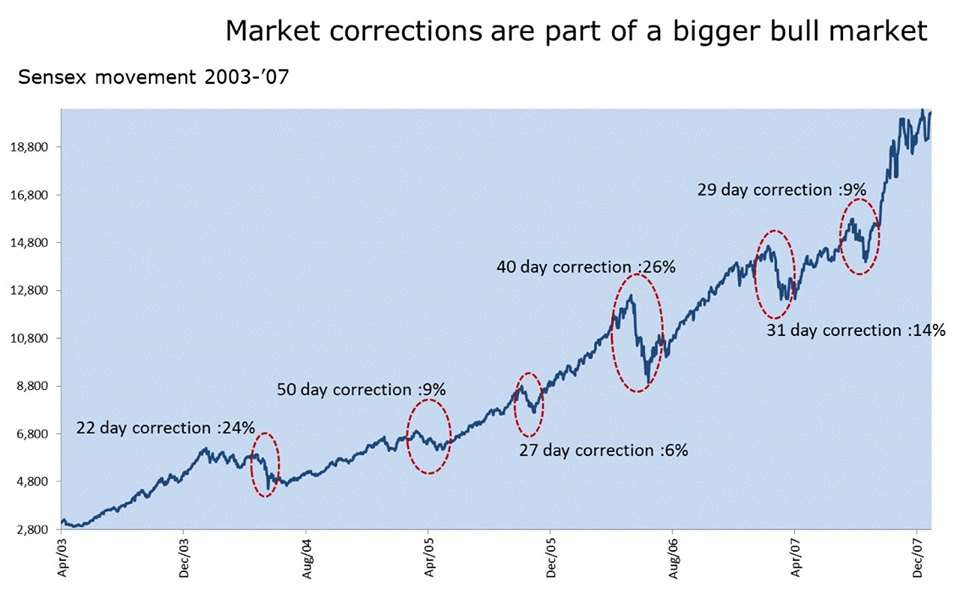

No rally without pull backs

A bull market correction typically happens when there are short-term pain points, external shocks not anticipated and generally higher valuations. The current phase would fit this description as the fundamental factors whether in terms of inflation, deficit or growth have not changed significantly.

We borrowed this image (unable to acknowledge source) below, that is doing the rounds in the social media now, to show how in one of the best bull markets between 2003-07, there were plenty of corrections.

A 15% or more correction cropped up on 3 occasions in the last cycle. As we often reiterate, we view these as normal, healthy and necessary to provide you opportunities to average costs better.

While we have tried explaining the reasons for the market volatility, we keep our strategy on what you should in such a scenario, unchanged. We urge you to read our earlier view on what you should do in a correction.

Volatility of the rupee, oil price and gilt could well be opportunities. And when the market maker (FIIs) are selling, you know there could be deep discounts. Even if you do not make the best out of it, resist the fear of moving out with them. Remember, you do not have destinations, sae for a now-reduced deposit to park your money in. And when they come back, it may be too late for you!