It’s that time of the year when you will look back at performance and have questions about your portfolio – specifically underperformance in your funds. In years like 2018 when there has been broad-based underperformance, it may be hard for you to accept the reality of your funds’ returns. These are some of frequently asked questions we come across, in our interactions with you.  We would like to share our responses to such questions. This can help you and give you some comfort when you undertake your annual portfolio review.

We would like to share our responses to such questions. This can help you and give you some comfort when you undertake your annual portfolio review.

I read in the newspaper that X was the best performing fund for 2018. Why didn’t you suggest it for me?

The answer depends on whether the fund you are talking of is a short-term outperformer and whether it fits your own profile. For example: Axis Multicap is a top performer in the past 1 year in the multi-cap category. It was launched only in November 2017 and had the advantage of deploying its money in the correcting market of 2018 and took concentrated exposure in some stocks. Without a track record of how it will do in various markets, this fund would not have passed our research criteria and hence would not have been recommended by your advisor.

A few of you thought you missed the rally in technology funds or an international fund like HSBC Brazil Fund. But if you were an investor just starting out with a core portfolio, know that a sector fund would not find a place there. These funds require some timing and to be used only as additions to your core portfolio. The point is – there could be reasons ranging from your time frame, to your risk profile to your savings capability as to why you were not given a certain fund. For example, we did add a technology fund to our theme list at the beginning of 2018 and gave it selectively for those who could handle risks. We also had US-based funds for diversification.

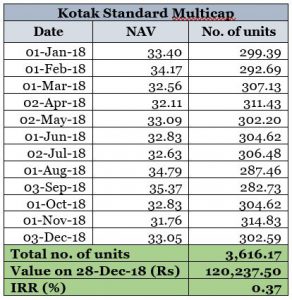

You suggested SIPs to tide over market volatility. They are all doing miserably. Why should I continue?

If you started investments last year and your SIPs returns are flat or negative, it has nothing to do with SIP being a bad tool.  It has everything to do with the market.

It has everything to do with the market.

For example, Kotak Standard Multicap would have returned 0.37% IRR while its benchmark Nifty 200 returned -1.2% in 2018. What the fund did in a fall year is to buy more units. For Rs 10,000 invested you would have received 299 units in January 2018, but it went to 314 units in November 2018. Essentially, you have been cost averaging at lower NAVs. The table alongside shows how your unit accumulation would have taken place over the course of 2018.

As we have pointed out before, SIPs don’t guarantee you positive returns. They help you make the best of market falls. Running SIPs does not excuse you from the necessity of holding equity for the long term.

You had drawn a plan for me at the beginning of the year. The returns are lower than the assumed rate for the plan. What course correction should be done now?

When we draw a long-term plan for you based on best estimates (on long-term inflation and equity and debt return), it is drawn as an annual plan for the sake of understanding your savings pattern. This does not mean that the long-term returns will be replicated every year. For example, a 12% return assumed for a 5-year equity portfolio may not be 12% every year. In some years, the returns are lower and other years make it up.

What we try to do when we review your portfolio is whether a shortfall is due to your fund’s poor performance or due to market underperformance. When we think it is the former, we suggest course correction. In the case of the latter, depending on the depth of the correction, we don’t wait till the end of the year or at your request. We sound you off on ‘averaging’ or ‘add more’ opportunities as and when they arise through the year. We did resort to those in 2018. If you make the best of such opportunities, you will see that your plan derails very little.

We have more such questions, on portfolio review, portfolio building, funds’ performance, markets and so on which we will try and cover in our Money Talk column. Meanwhile, stay the course and stay invested!