Motherson Sumi Wiring India Ltd. – Premiumisation Play

Motherson Sumi Wiring India Limited (MSUMI) was established by de-merging the wiring harness business supporting its customers in India from its parent company Samvardhana Motherson International Limited (SAMIL) [Formerly Motherson Sumi Systems Limited]. MSUMI is a leading and fast-growing full-system solutions provider to OEMs, in the wiring harness segment in India. It is a joint venture between Samvardhana Motherson International Limited (SAMIL) and Sumitomo Wiring Systems, Ltd. (SWS).

MSUMI has a product profile that benefits from favourable industry trends of premiumisation, which leads to an increase in automobile electrification, and supports current and future automotive trends. With over 40,000 employees in 26 facilities, the company has a diversified PAN India industrial footprint, close to OEM locations.

Products & Services:

The Company is in the manufacturing of Wiring Harness & its Components majorly sold to Original Equipment Manufacturers (OEMs). It offers world-class skills and broad experience in manufacturing, assembly, and in-sequence delivery of integrated, cutting-edge electrical and electronic distribution systems for power supply and data transfer across vehicle types (passenger cars, two-wheelers and three-wheelers as well as recreational, commercial and multiutility vehicles), price ranges (from entry-level to mid-range and premium level) and manufacturing locations.

Subsidiaries: As on FY22, the company has no Subsidiary, Associate or Joint Venture company.

Key Rationale:

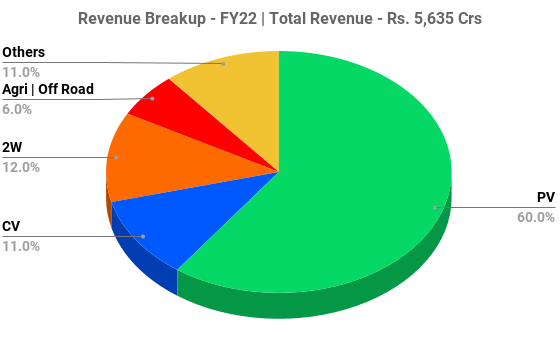

- Market Leader – MSUMI is the market leader in the domestic wiring harness industry with a market share of more than 40%. Post demerger, the company became a Domestic pure play wiring harness player which derives almost 95%+ of its revenue from the Indian market. The Indian Passenger vechicle (PV) industry growth is crucial for the company’s growth since 60% of its revenue is derived from the PV industry.

- Premiumisation Play – Globally, the automotive industry is undergoing few megatrends like electrification, premiumisation, Connected & Autonomous Vehicles (ADAS technology), Software defined Vehicles, etc. MSUMI being a leader in Wiring harness (WH) business with cost efficiencies is going to benefit from the above trends as they will lead to an increase in wiring content per vehicle. With WH content of EV is presently 2x of the ICE vehicles, the company has setup a dedicated line at Chennai for high-voltage harnesses to meet the demand for EV/hybrid vehicles (PV, CV & Two-Wheeler). WH typically constitutes ~1.75-2.25% of the value of a vehicle and the rising sales of high and mid end UV’s is directly contributing the growth of the WH market.

- Q3FY23 – During Q3FY23, the revenue grew 16% YoY/-8% QoQ to Rs.1687 crs. The EBITDA for Q3FY23 down by 14% YoY/6%QoQ to Rs.179 crs on account of high empolyee cost and other costs. Higher operating costs due to lower production at OEMs on QoQ basis, leading to lower utilisation of added capacities. The inflation in the wages is the important cause for the increase in the employee cost. The capex for Q3FY23 stands at Rs.61 crs. In Q3FY23, the company added 3 new facilities (26 now, compared to 23 earlier) and enhanced overall capacities by over 25% in terms of manhours compared to Q3FY22.

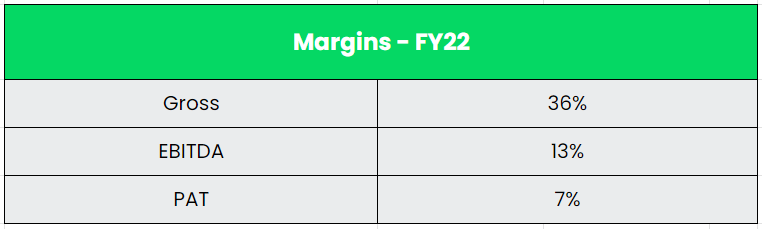

- Financial Performance – FY22-23 is the first reporting financial year for MSUMI as independent public listed company (Group reorganisation implemented in Jan–March 2022 quarter with approval of Hon’ble NCLT, Mumbai. During FY23, MSUMI expanded capacity (Capex of 9MFY23 is Rs.147 crores) in line with customers forecasted requirements as well as orders for new models/programs awarded to company. The company developed products for 11 new/full model change and 4 facelift model in the passenger vehicle segment during first nine months and is currently working on 6 new/full model changes which will be launched in next 3-6 months. These will contribute nearly 40% of the total business of the company, requiring the company to hire and train additional manpower (approx. 7000 people) upfront for successful launch of these programs. The company has the industry leading return ratios, Asset turns and margins. The company had a revenue growth of 9% CAGR between FY17-22 outperforming the Passenger Vehicle Industry growth for the same period.

Industry:

India is expected to be the world’s third-largest automotive market in terms of volume by 2030. India holds a strong position in the international heavy vehicles arena as it is the largest tractor manufacturer, second-largest bus manufacturer, and third largest heavy trucks manufacturer in the world. It is also the world’s largest 2W and 3W manufacturer. India’s Automotive Industry is worth more than $222 Bn and contributes 7.1% of India’s GDP & 49% of its manufacturing GDP. Passenger vehicles posted highest ever retail sales at 36,20,039 units in FY 2022-23 with a growth of 23% YoY. The Overall EV sales in India also reached a record mark of more than 1 million units in a financial year (FY23). The EV market is expected to grow at CAGR of 49% between 2022-2030 and is expected to hit 10 Mn-unit annual sales by 2030. India automotive wiring harness (WH) market is currently ~US$1.5bn vs ~US$20bn of Asian WH market and global WH market size of ~US$40bn.

Growth Drivers:

- In the Union Budget 2023, the government has increased the budget allocation of FAME II subsidy by 78% to Rs.5172 crs.

- Rise in the customer preference towards premiumisation (connected/autonomous vehicles) and electrification is likely to drive the wiring harness industry.

- The Production Linked Incentive (PLI) Scheme for Automobile and Auto Component successful in attracting proposed investment of Rs.74,850 crore against the target estimate of investment Rs.42,500 crore over a period of five years.

Competitors: Minda Corporation.

Peer Analysis:

The company’s closest domestic peers are operating in the unlisted space namely Yazaki India, Aptiv India, etc. In the domestic listed space, we took Minda corporation for comparison as it has a negligible amount of revenue generation from the wiring harness solutions and it is clear that MSUMI has a near monopoly status in the wiring harness space. The return ratios and margins of MSUMI are also way ahead of its peers.

Outlook:

Started its journey as a ‘Build-to-Print’ player in the domestic wiring harness with Maruti Suzuki, the company has now evolved as a full-system solution provider and has built large operational scale with sheer dominance over its competitors. Strong support from its parent companies Samvardhana Motherson International Ltd. (SAMIL) – for sourcing of wires and components, sharing of common support functions, strategic guidance and leasing of land and building) and Sumitomo Wiring Systems (SWS) – access to leading technologies will help the MSUMI to sustain the dominance in the domestic wiring harness industry. The company guided for ~1.5x wiring harness content in an SUV vs. a hatchback car while the same print for sedan was at ~1.4x. Also, ~1.2x wiring harness content in a top variant of PV model vs. the base variant and ~1.1x wiring harness content in a top 2-W variant vs. base variant. In the EV Segment, the company has guided for ~2.4x wiring harness content in an electric PV vs. ICE driven PV and ~8x wiring harness content in an electric 2-W vs. ICE powered 2-W. The Group also reiterated its revenue target of US$36 billion by FY25 with 40% RoCE & 40% dividend payout. It also aims to realise 75% of revenues from the auto space and rest 25% from non-auto domain.

Valuation:

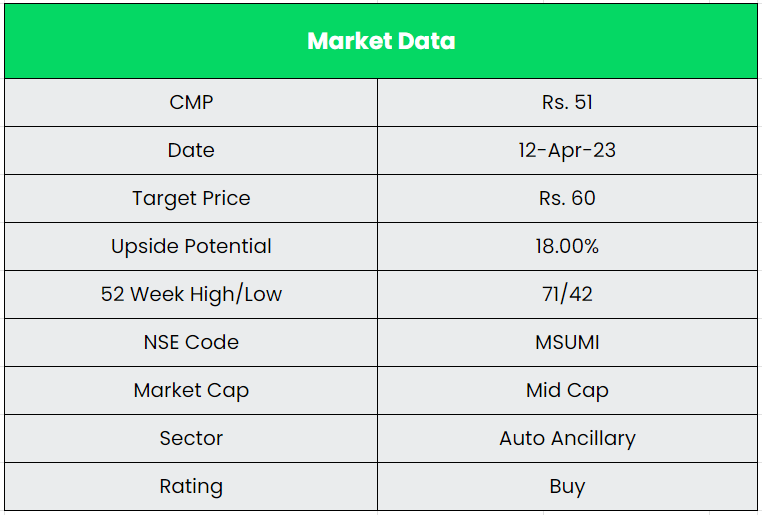

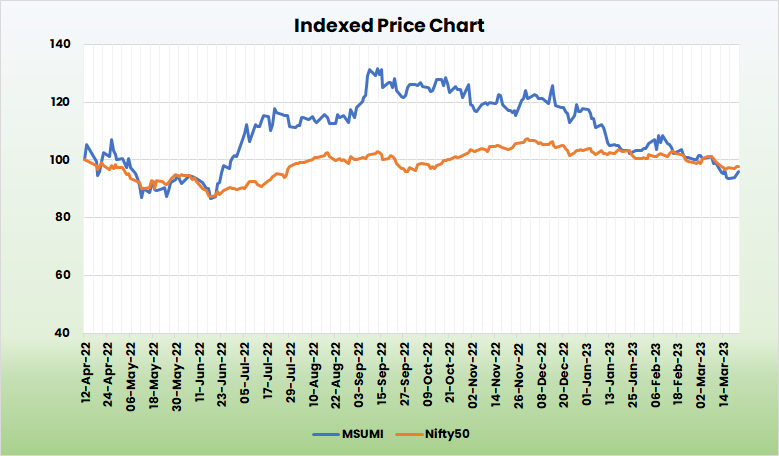

MSUMI is a strong play in the recovering Passenger Vehicle industry with strong fundamentals and structures a long-term growth with the increase in content per vehicle through electrification and Premiumisation. We recommend a BUY rating in the stock with the target price (TP) of Rs.60, 40x FY25E EPS.

Risks:

- Client concentration Risk – MSUMI has a high concentration of business in PVs and particularly with MSIL (Maruti Suzuki India Ltd.). It enjoys ~60% wallet share of MSIL. Any market share loss at the OEM level could impact MSUMI sales negatively.

- Technology shift – With the industry moving towards electrification, which needs more wiring and cables while simultaneously focusing on lightweight would need the emergence of newer technology. This will reduce the weight of wires or any development in wireless technology can significantly hamper MSUMI’s business.

- Raw Material Risk – Any major inflation in copper costs or other key input commodity costs like that of aluminium or polymers would impact gross margin, as it would be tough for the company to pass on the margin.