Larsen & Toubro Ltd. – Powering the Nation’s Hopes

Larsen & Toubro Limited (L&T), incorporated in 1946 and headquartered in Mumbai, is India’s leading multinational conglomerate operating across engineering, construction, manufacturing, technology services, and financial services. The company undertakes Engineering, Procurement and Construction (EPC) projects spanning infrastructure, energy, hi-tech manufacturing, IT & technology services, financial services, and development projects. L&T has a diversified international presence, with its Power Transmission & Distribution business alone serving customers across 30 countries in SAARC, ASEAN, the Middle East, Africa, North America and CIS regions, supported by multiple manufacturing facilities including large tower and container-integration units at Kancheepuram (Tamil Nadu), Kansbahal (Odisha) and Hazira (Gujarat) catering to transmission towers, BESS containers, heavy engineering and minerals & metals equipment. Beyond its core EPC and manufacturing operations, the company has strategic ventures in emerging technology areas including data centers (L&T-Cloudfiniti), semiconductor design (L&T Semiconductor Technologies), digital B2B marketplace (L&T-SuFin), electrolyser manufacturing for green hydrogen, and small modular reactor development.

Products and Services

The company’s business can be categorised across 5 business:

- Construction – Among India’s largest construction companies, L&T executes projects across heavy civil infrastructure, water & effluent treatment, power T&D, buildings & factories, transportation and metals & mining.

- Energy – Provides EPC solutions spanning hydrocarbon (onshore and offshore), green and clean energy, CarbonLite solutions and offshore wind projects.

- Manufacturing – Manufactures engineered-to-order equipment and systems for core industries through precision engineering, heavy engineering, special steels and heavy forgings businesses.

- Services – Offers IT and digital solutions, ER&D services for global clients, along with edutech and B2B e-commerce platforms.

- Allied Businesses – Operates in realty, construction & mining equipment, rubber processing machinery, industrial valves and related segments.

Subsidiaries – As of FY25, the company has 87 subsidiaries, 6 associate companies, 11 joint ventures, and 36 jointly held operations.

Investment Rationale

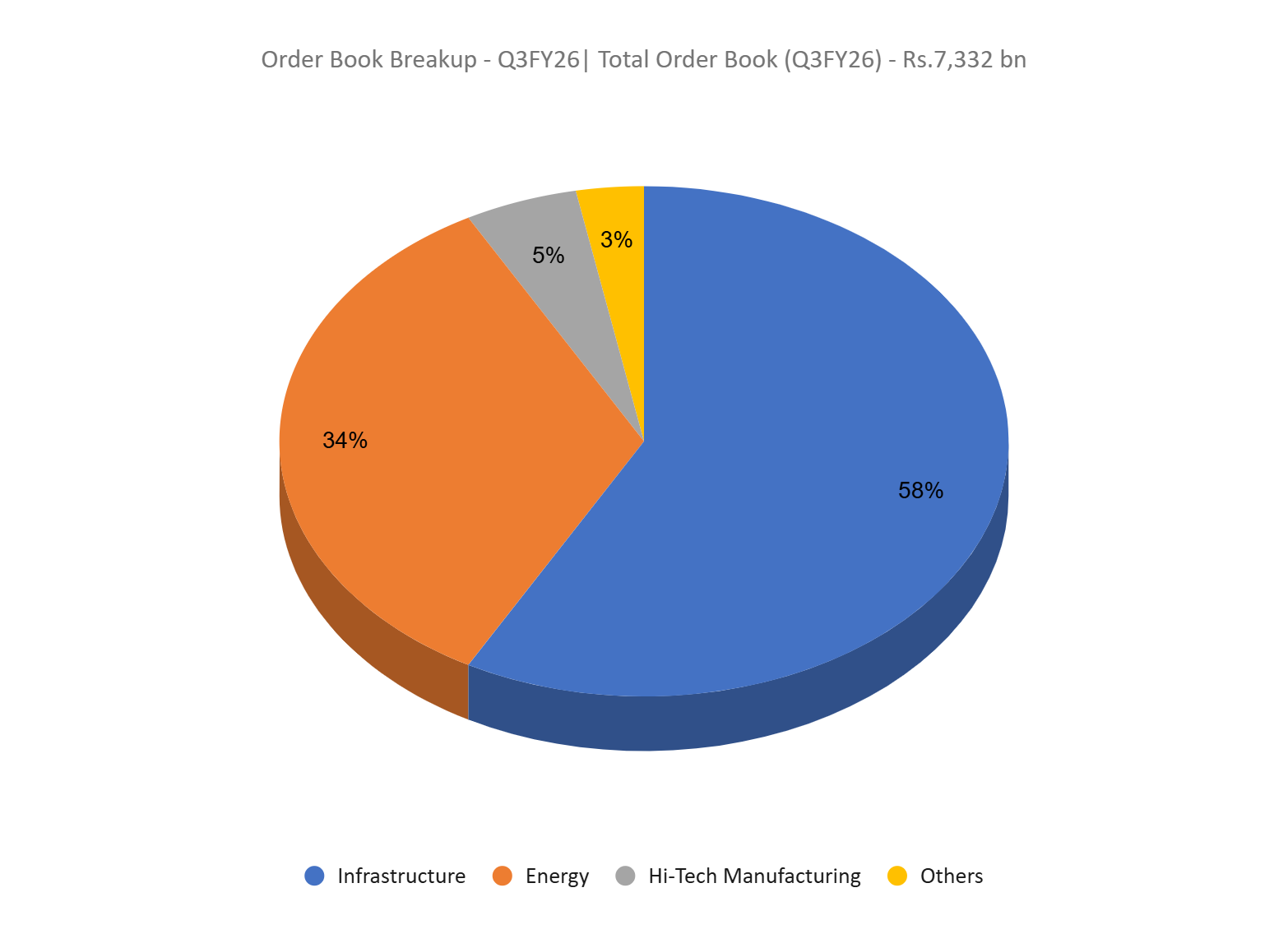

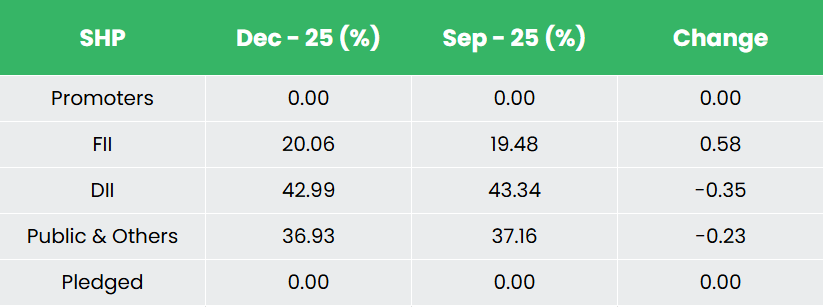

- Robust order inflows support earnings visibility – L&T reported its highest ever quarterly order inflow of Rs.1.36 trillion (+17% YoY) in Q3FY26, led by broad-based demand across India and overseas markets. The core Projects & Manufacturing (P&M) segment contributed Rs.1.16 trillion (+18% YoY) with domestic orders rising sharply 30% YoY, driven by hydrocarbons, buildings & factories and CarbonLite/energy transition opportunities, while international inflows grew a steady 7%. The near-term prospect pipeline expanded to Rs.5.92 trillion (+7% YoY) and the total order book surged 30% YoY to Rs.7.33 trillion translating into multi-year revenue visibility. Importantly, the mix is improving: private sector share increased to 36% (vs 21% in Mar-25), indicating an early private capex revival rather than reliance purely on government spending. Infrastructure and Energy together form ~92% of the book, while geographic diversification remains balanced (51% domestic / 49% international), reducing cyclicality risk.

- Segment performance margins stabilising with near-term energy drag – P&M revenue grew 11% YoY to Rs.523 billion with margin improving to 8.1% (+50 bps YoY), indicating operating leverage beginning to play out. Infrastructure saw strong ordering (+26% YoY) from private sector buildings, data centres, semiconductors and renewables; execution remained healthy internationally and margins improved to 6.1% (+60 bps YoY) despite temporary domestic water-segment slowdown. The Energy segment posted robust revenue growth (+15% YoY) on a larger order book but margins declined to 5.9% due to cost overruns in legacy hydrocarbon projects – management expects this drag to persist only for the next few quarters as these projects close out. Hi-Tech Manufacturing delivered strong 34% revenue growth, supported by defence and precision engineering execution ramp-up and better job mix.

- Q3FY26 – During the quarter, the company posted consolidated operating revenue of Rs.71,450 crore, registering a 10% YoY increase from Rs.64,668 crore. EBITDA rose 19% YoY to Rs.7,417 crore from Rs.6,255 crore, while net profit declined 4% YoY to Rs.3,215 crore compared with Rs.3,359 crore. As of December 2025, the Net Working Capital to Revenue ratio improved to 8.2%, a 450 bps YoY improvement, driven primarily by stronger customer collections and a reduction in gross working capital over the past 12 months.

- FY25 – During FY25, the company reported consolidated operating revenue of Rs. 2,55,734 crore, representing a 16% YoY increase compared to Rs. 2,21,113 crore in FY24. Operating profit stood at Rs. 34,335 crore, up 19% YoY, and net profit was recorded at Rs. 17,673 crore, posting a growth of 14% YoY.

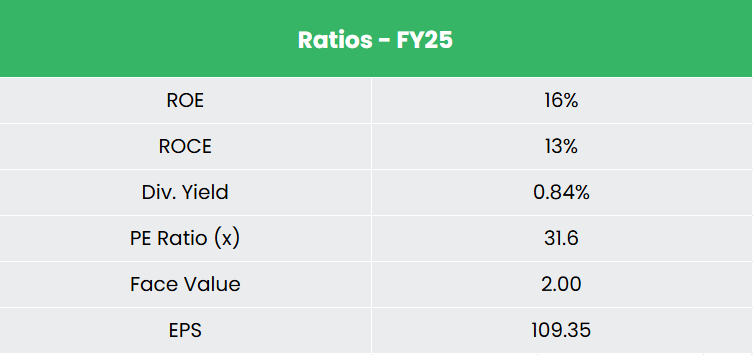

- Financial Performance – The 3-year revenue and net profit CAGR stands at 18% and 23% respectively between FY23-25. The company has a debt-to-equity ratio of 1.32, and the 3-year average ROE and ROCE are around 14% and 13% for FY23-25 period.

Industry

The Indian engineering and capital goods sector form a critical backbone for the economy, contributing 1.9% to India’s GDP and supporting key end-markets such as construction, infrastructure, power, consumer goods, and automotive. In FY25, exports of engineering goods reached Rs.9,86,328 crore (US$116.67 billion), with engineering accounting for about 25% of India’s total merchandise exports and positioning the sector as one of the largest foreign exchange earners. The capital goods industry has scaled up significantly, with production in the heavy engineering and machine tools segment rising from Rs.2,29,533 crore (US$27.2 billion) in CY15 to Rs.4,29,001 crore (US$50.7 billion) in CY24, while India’s construction equipment market stood at Rs.69,046 crore (US$7.91 billion) in FY25 and is projected to reach Rs.1,02,827 crore (US$11.78 billion) by FY30 at a CAGR of 8.3%.

Growth Drivers

- Strong domestic demand visibility – Highway construction, power capacity addition, and a Rs.11,21,000 crore FY26 infrastructure capex outlay are driving sustained demand for engineering and capital goods.

- Export momentum in engineering – Engineering goods exports reached Rs.9,86,328 crore (US$116.67 billion) in FY25, with a target of US$200 billion by 2030.

- Policy support and liberalized FDI regime – A de-licensed sector with 100% FDI permitted under the automatic route and schemes like the National Capital Goods Policy 2016 and Capital Goods Competitiveness Scheme support.

Peer Analysis

Competitors: IRB Infrastructure Developers Ltd, Kalpataru Projects International Ltd, etc.

Compared to peers, the company benefits from its scale, which supports superior execution and stronger return ratios. Its diversified order book underpins more stable performance and reflects disciplined project selection and risk management. Cash flows are structurally supported by advance payments typical of large EPC contracts, aiding liquidity and limiting incremental funding requirements during execution.

Outlook

L&T’s outlook remains constructive supported by strong capex momentum, with 9MFY26 order inflow growing 30% YoY and management indicating it will exceed the 10% FY26 inflow guidance backed by a healthy pipeline. Revenue growth of 12% so far keeps the company on track to achieve ~15% FY26 growth aided by the typical Q4 execution ramp-up. P&M EBITDA margin at 7.9% is progressing toward the ~8.5% full-year target, while legacy hydrocarbon project impact should fade over the next few quarters, supporting margin expansion thereafter. Working capital has improved sharply (8.2% vs earlier 12% guidance) reflecting better collections and contract terms, strengthening cash flows and return ratios. With strong order visibility, improving mix toward private capex and energy transition, and normalising margins, earnings growth visibility remains high.

Valuations

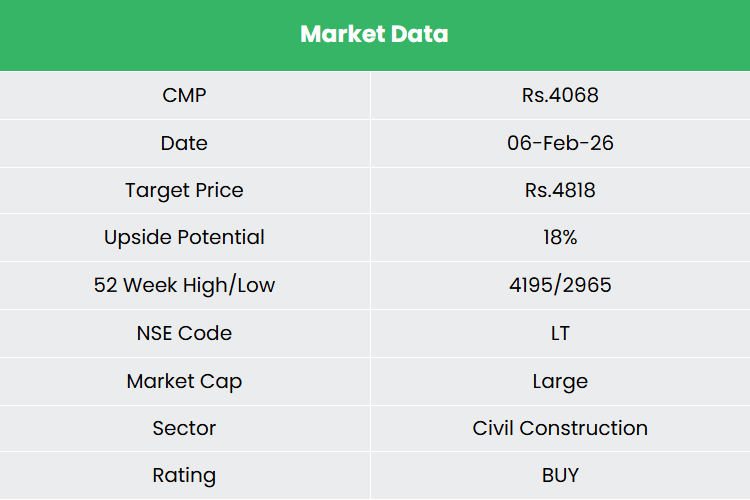

L&T is a strong player in India’s capex spend for infrastructure development and execution of the nation’s strategic projects. We expect the company to retain its leadership position in the mid to long term as well. We recommend a BUY rating in the stock with the target price (TP) of Rs.4,818, 31x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.