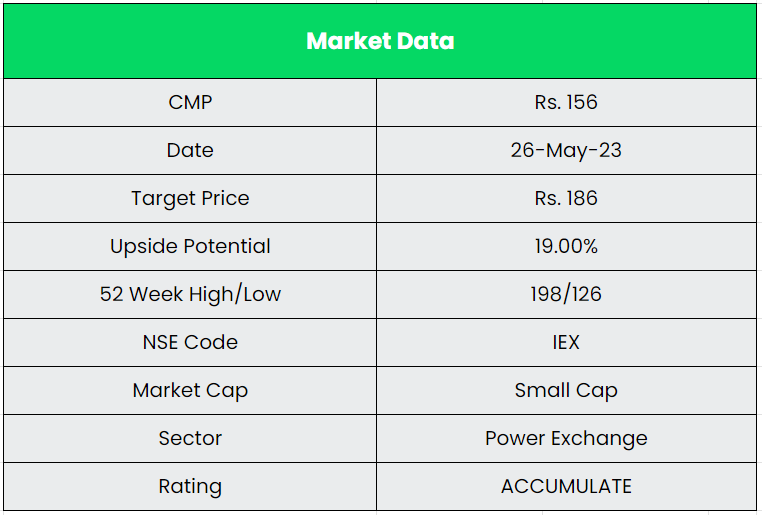

IEX Ltd. – Monopolistic Power Exchange

Incorporated in 2008, Indian Energy Exchange Limited (IEX) is India’s premier energy marketplace, which is approved and regulated by the Central Electricity Regulatory Commission (CERC) and provides nationwide automated power trading. The platform leverages technology to provide solutions for sustainable energy, ensuring competitive, transparent, and reliable access.

The exchange platform enables efficient price discovery and increases the accessibility and transparency of the energy market in India while also enhancing the speed and efficiency of trade execution. The Exchange is ISO Certified for quality management, Information security management and environment management since August 2016. The exchange is having a robust eco system of 7500+ registered participants, 4500+ commercial & industries, 55+ Distribution companies (Discoms) and 600+ Electricity Generators.

Products & Services:

The company has a various type of products which are listed below.

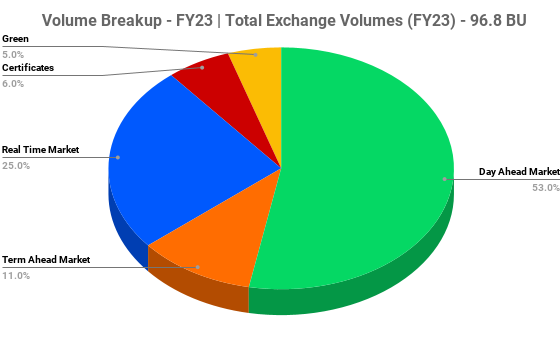

- Day Ahead Market (DAM) – DAM is a physical electricity trading market for deliveries for any/some/all 15-minute time blocks in 24 hours of next day starting from midnight.

- Term Ahead Market (TAM) – TAM provides a range of products allowing participants to buy/sell electricity on a term basis for a duration of up to 11 days ahead.

- Real Time Market (RTM) – Electricity Delivery After 4-time blocks or 1 hour of delivery.

- Renewable energy certificates – RECs are tradable, intangible energy commodities which represent the attributes of electricity generated from renewable resources.

- Green Term Ahead Market – GTAM is a new market segment for trading in renewable energy following the CERC approval. The new market segment features contracts such as Green-Intraday, Green-Day-ahead Contingency (DAC), Green-Daily and Green-Weekly.

Subsidiaries: As on 31st Mar 2023, the company has two subsidiaries and one associate company.

Key Rationale:

- Strong Market Position – IEX is the first and the largest energy exchange in India. It allows for trading of electricity on its platform just like NSE and BSE allow trading of stocks. There are electricity generation companies (called gencos) like NTPC, Tata Power, Adani Power, etc. Then there are energy distribution companies (discoms). IEX comes in between the generation and distribution companies. IEX’s primary revenue sources include transaction fees (about 80% of revenues) and annual subscription fees (4% of revenues). Since the commencement of its business in 2008, the trading volume on its exchange has been increasing at a staggering rate of over 30% CAGR. The company has a market share of more than 99% in the DAM and RTM category. The company’s overall electricity market share (including all the products) in FY23 stands at 88.4%.

- Power Exchange Players – About 90% of electricity traded on the exchange is through IEX. The power exchange market was duopolistic in Nature till 2022 with IEX and PXIL. Both players started operations almost at the same time in FY09. However, over the years, IEX has dominated and captured the market. PXIL is promoted by National Stock Exchange, NCDEX, Tata Power, PFC, GMR Energy, and Gujarat Urja Vikas Nigam. PXIL currently is a loss-making entity with a market share of only 5%. In July 2022, a new exchange was started in the name of Hindustan Power Exchange (HPX).

- New Subsidiary – In Q3FY23, IEX incorporated a wholly owned subsidiary, ICX (International Carbon Exchange), to leverage opportunities in the carbon market, for which it is closely working with agencies like the Bureau of Energy Efficiency (BEE), major carbon exchanges, and potential players in this space. ICX will enable participants to buy and sell voluntary carbon credits at competitive prices through its transparent & reliable Exchange platform, helping large corporates meet their ESG requirements. By facilitating the companies to meet their climate commitments goals, ICX will help India achieve its target of reducing the carbon emission of its GDP by 45% by 2030 to limit global warming to 1.5 degrees Celsius. On the other hand, its subsidiary turned associate company IGX has launched a Gas Index named GIXI. GIXI represents volume weighted average price for all gas traded on any day (excluding domestic ceiling price gas). The IGX had a total volume of 50.9 million MMBtu with a YoY growth of 319%.

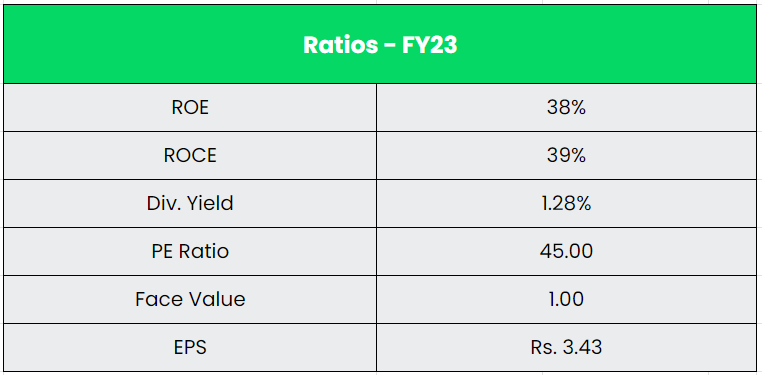

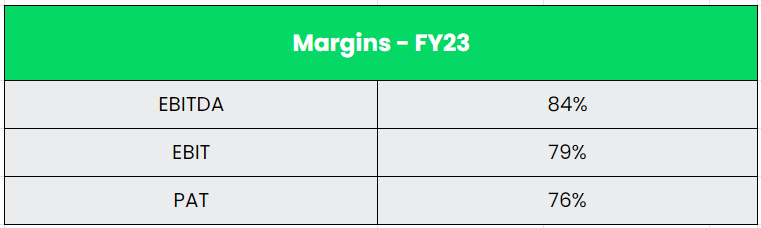

- Financial Performance – The company has been completely debt free for the past 10 years with around Rs.1268 crs of cash and cash equivalents (9% of the Market Cap.) making the balance sheet robust. The Revenue and PAT CAGR of the company for the past 5 years is around 12% and 19% between FY18-FY23. The 5-year Average ROE for the company is around 42% for the past 5 years.

Industry:

India has become the third-largest electricity producer globally as a consequence of its economic growth, leading to a surge in its energy demand. This demand has been accommodated by the continual expansion of power generation capacity through various sources. Between FY17 and FY22, India’s overall energy consumption increased from 1,135 billion Units (BU) to 1,381 BU at a CAGR of 4%. By FY30, this consumption is expected to reach 2,280 BU at a CAGR of 6% between FY23-30. According to International Energy Agency, despite this increase, India’s average per capita electricity consumption in FY21 was ~1,200 kWh, which is just over one-third of the global average of ~3,500 kWh, leaving considerable potential for further expansion.

Growth Drivers:

- India’s rapidly growing population and economy have led to a significant increase in demand for electricity across various sectors, particularly in urban and industrial areas.

- The Government is focusing on improving electricity infrastructure, including transmission and distribution networks, to improve access to electricity in rural areas and increase grid stability.

- To meet India’s 500 GW renewable energy target and tackle the annual issue of coal demand supply mismatch, the Ministry of Power has identified 81 thermal units which will replace coal with renewable energy generation by 2026.

Competitors: MCX, etc.

Peer Analysis:

IEX is the only listed player in the power exchange market. Being a monopoly in the listed space, we thought we can compare it with the other monopolistic companies. MCX on the other hand is a listed commodity exchange company which is also a monopoly in its segment.

Outlook:

IEX enjoys a virtual monopoly in the power exchange segment and it has gradually increased its market share in overall short-term power market. IEX has remained committed to expanding its product portfolio in response to the ever-evolving consumer demands. The Company’s constant focus on expanding its product basket has enabled it to establish a first-mover advantage. It is in the process of setting up a Coal exchange and regarding that the Ministry of Coal has appointed a consultant for finalising the framework for a coal exchange in India. Further, IEX plans to also bring in trading in petroleum product pipeline capacity. The Company remains committed to exploring new areas and launching products that align with market requirements. IEX’s success can be attributed to its ability to launch tailored products that meet customers’ needs, resulting in customer stickiness reflected in the company’s continued dominant position in the market.

Valuation:

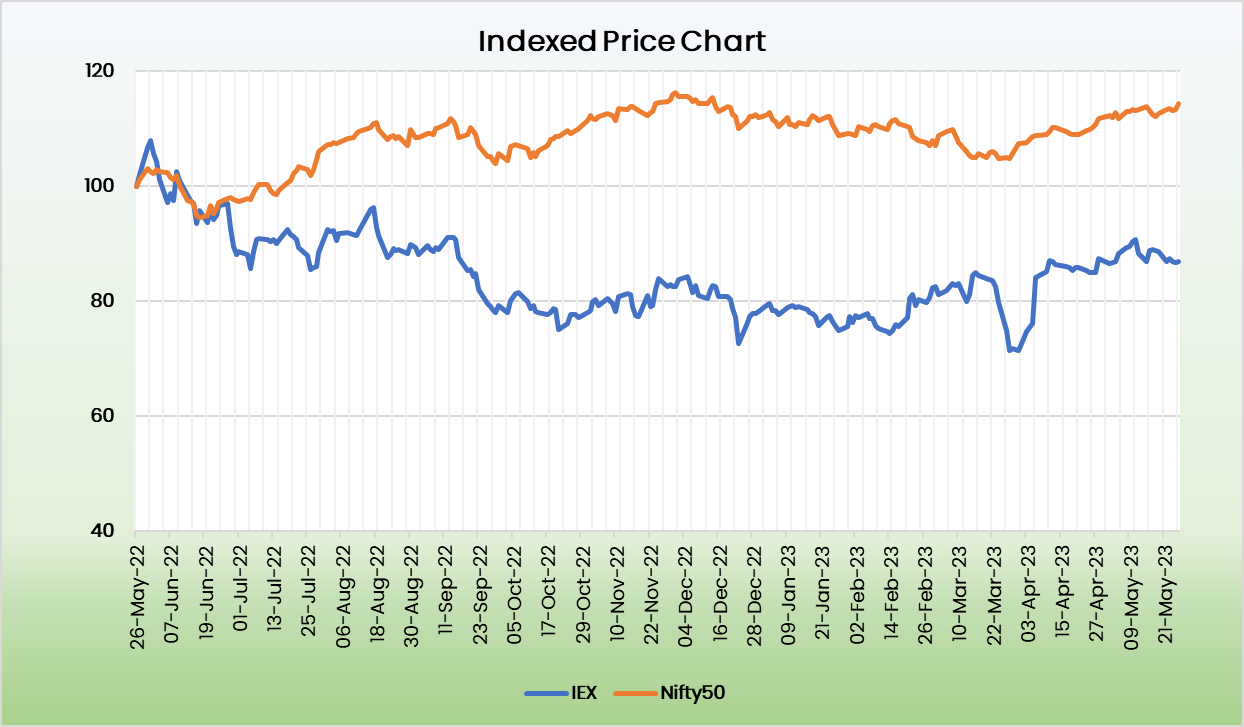

IEX has been a pioneer of power trading in India and it aligns with the transformational journey, the Indian power market is headed i.e., ‘One Nation, One Grid and One Price. The volumes on the platform have been on the rise over the last many quarters on account of the new product addition and shift of volumes from traditional modes of transaction. We recommend an ACCUMULATE rating in the stock with the target price (TP) of Rs.186, 41x FY25E EPS.

Risks:

- Regulatory Risk – IEX is regulated by CERC which is a key regulator of power sector in India and it also decides the per unit charge that exchanges charge on trading. It may pass regulations like introduction of new exchange or decreasing the per unit charge that can harm the monopoly status and margins which IEX enjoy.

- Competitive Risk – Market share gain by the new exchange or any aggressive move by PXIL may impact the volume growth which results in a competitive risk.

- Product Execution Risk – New product introduction would help market participants to optimize their energy requirement through combination of product mix and that would play a significant role in overall power sector development and power exchanges. Any delay in product launch may derail the growth momentum for the company.