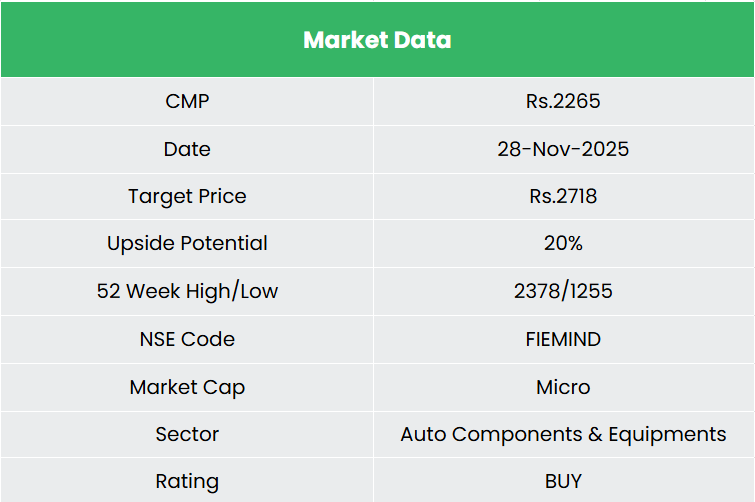

Fiem Industries Ltd – Light up the world

Fiem Industries Limited is a Tier-1 automotive components manufacturer headquartered in New Delhi, with operations anchored in India’s two-wheeler ecosystem and an expanding presence in passenger vehicles. Incorporated in 1989, the company is currently among India’s leading manufacturers of automotive lighting and signalling equipment, complemented by rear-view mirrors, plastic moulded parts, sheet metal components and select safety and electronic parts. Over the years, Fiem has steadily migrated its portfolio towards LEDs, with LED lighting now contributing to a majority of total automotive lighting revenues. Manufacturing is carried out through nine strategically located plants across key automotive hubs across India, supported by R&D and design centres in India, Italy and Japan.

Products and Services

- Automotive LED Lighting – LED headlamps, tail lamps, turn indicators, DRLs and signalling units.

- Automotive Lighting (Conventional) – Halogen headlamps, tail lamps and indicator lamps.

- Rear View Mirrors – Integrated mirror systems for two-wheelers.

- Plastic Moulded Parts – Body panels such as fenders, floor panels and side covers.

- Others – Sheet-metal parts, canisters, sensors and assorted engineered components.

Subsidiaries: As of FY25, the company has 2 subsidiaries and 2 joint ventures.

Investment Rationale

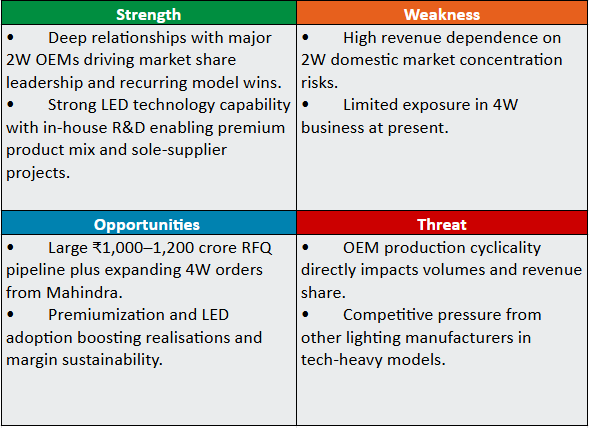

- Expansion into new platforms and vehicle segments – The company is extending its core competencies in LED lighting into higher-value vehicle platforms across both domestic and export markets. In FY25, it began supplies to Mahindra & Mahindra for their passenger vehicles, starting with LED license plate lamps, and has since secured follow-up orders for high-mounted stop lamps and fog/reflector lamps on the Bolero and Scorpio. This marks a significant diversification beyond its traditional two-wheeler base. Within two-wheelers, the company began supplies of projector headlamps for the refreshed Hero Glamour X 125, as well as winker lamps for the Glamour and Xtreme models. It also commenced LED headlamp and taillamp supplies for Yamaha’s XSR 155 and its first electric model in India. This broadening customer base across 2W EVs, ICE scooters, and passenger cars is expected to enhance revenue visibility and improve per-vehicle realisation over the medium term.

- Robust Product Portfolio providing a strong proxy to Auto momentum – FIEM’s extensive product coverage including headlamps, taillamps, indicators, mirrors, plastic and sheet-metal parts, create a revenue stream that tightly tracks the performance of India’s automotive industry, which is currently in a strong upcycle. In Q2FY26, 2-wheelers contributed ~97.7% of revenue, and FIEM has deep relationships with all major OEMs including TVS, Honda, Yamaha, Suzuki and Royal Enfield, forming over 85% of its sales mix. The shift toward premium and LED-equipped models continues to benefit FIEM, a key driver of value growth and margin expansion. Supplementing this are growing EV engagements and early traction in passenger vehicles, cementing FIEM as a broad-based play on India’s ongoing mobility demand.

- Q2FY26 – During the quarter, the company reported revenue of Rs.711.4 crore, up 17.1% YoY compared to Rs.607.5 crore in Q2FY25. EBITDA rose to Rs.99.1 crore, a 23.5% increase from Rs.80.3 crore in the corresponding quarter, with EBITDA margin expanding from 13.2% to 13.9%. Net profit stood at Rs.63.8 crore, growing 28.0% YoY from Rs.49.8 crore in Q2FY25. LED contribution reached 63.9% of total lighting revenues, reflecting the company’s continued shift towards higher-value, technology-driven products. The margin expansion was supported by a richer product mix and improving scale benefits.

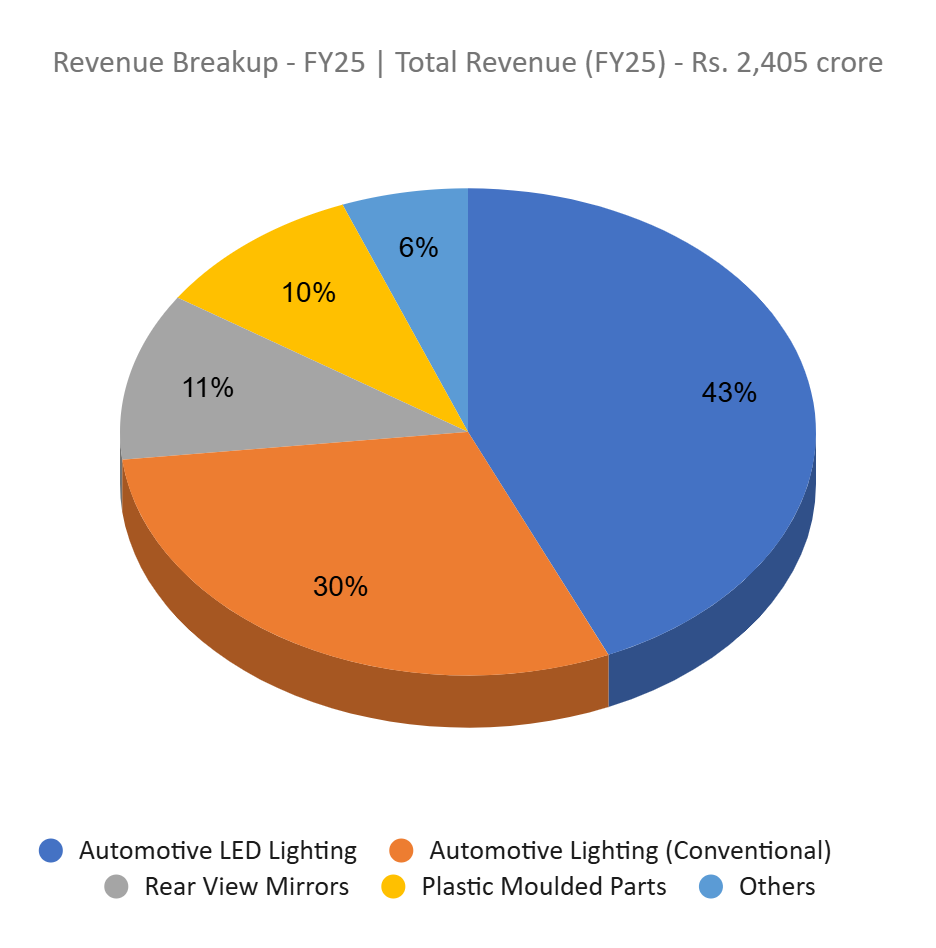

- FY25 – During FY25, the company generated revenue of Rs.2,405 crore, an increase of 19% compared to the FY24 revenue. EBITDA is at Rs.322 crore, up by 20% YoY. The company reported a net profit of Rs.205 crore, an increase of 24% YoY.

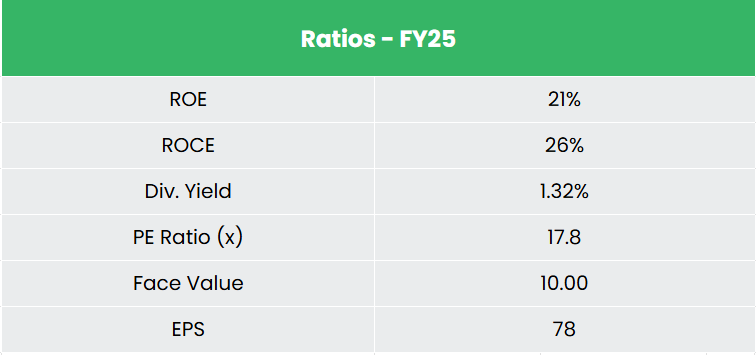

- Financial Performance – The 3-year revenue and net profit CAGR stands at 16% and 29% respectively between FY23-25. The company has a debt-to-equity ratio of 0.06. The 3-year average ROE and ROCE are around 20% and 27% for FY23-25 period.

Industry

India’s auto components sector is expanding rapidly, supported by a growing workforce, higher disposable incomes, and a realignment of global supply chains. The industry reached US$ 78.74 billion in FY25, growing at a 14% CAGR over FY20–25. It is expected to expand further with domestic OEM component sales rising to US$ 89 billion by 2030. The government’s push for manufacturing self-reliance and lower import dependence is strengthening the position of domestic suppliers. India is increasingly serving as a sourcing base for major global OEMs, benefitting from its geographic closeness to key automotive markets across Asia and Europe. Rising income levels, continued infrastructure development, and targeted policy support, especially for electric mobility are further accelerating sector growth. As electrification and hybrid adoption rise worldwide, Indian component makers are well-positioned to capture emerging demand.

Growth Drivers

- 100% FDI permitted under the automatic route for auto components manufacturing.

- Lower personal tax burden in Union Budget 2025 – 26 expected to boost discretionary spending by the expanding middle-class.

- Rs.7,400 crore allocation for the EV ecosystem in Budget 2025 – 26, representing a 74% YoY increase.

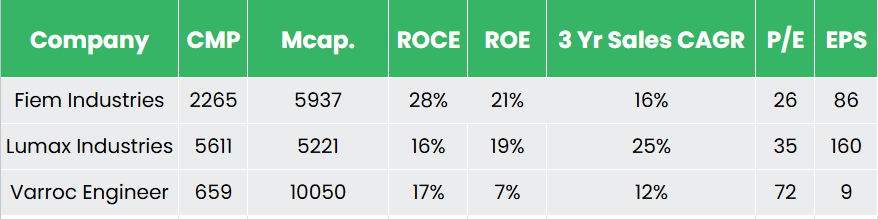

Peer Analysis

Competitors: Lumax Industries Ltd and Varroc Engineering Ltd, etc.

Compared to its peers, the company demonstrates disciplined capital allocation and strong overall financial performance.

Outlook

FIEM is actively building capacity to support the strong demand outlook and ensure it remains ahead of OEM volume growth. In H1 FY26, the company invested Rs.37.81 crore in capex, with another Rs.50–60 crore planned in H2, taking FY26 capex to ~Rs.100 crore, fully aligned with future scale-up requirements. Management highlighted capacity utilization moving toward the 80% range, signalling strong demand outlook. The company also sees visibility from its 100+ ongoing development projects, which are estimated to generate Rs.1,000 – 1,200 crore of revenue over the next few years. With a continued focus on lighting technology upgrades and RFQ conversion momentum in both 2W and 4W segments, the company is well positioned to sustain its guidance of 15–20% annual revenue growth.

Valuation

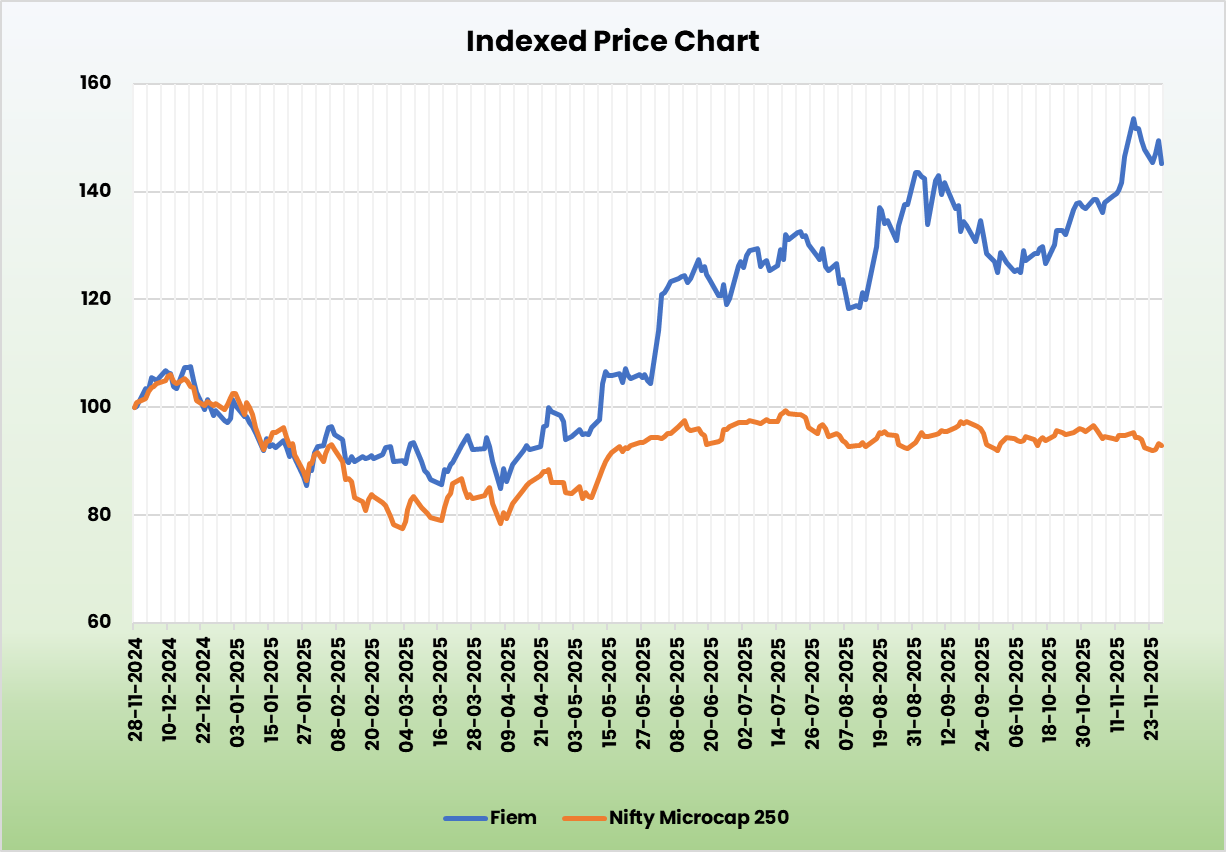

Fiem’s robust product portfolio is well positioned to benefit from the upcycle in auto demand, backed by strategic capacity expansions and deep OEM relationships. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,718, 21x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.