Elecon Engineering Company Ltd – Gearing the Future

Incorporated in 1960 and headquartered in the state of Gujarat, Elecon Engineering Company Ltd. is a leading Indian manufacturer of industrial gear solutions and bulk material handling equipment (MHE). The company caters to key industries including steel, cement, power, sugar, marine, and mining. With a global presence across Asia, the Middle East, Europe, the UK, the USA, and Africa, Elecon operates 5 state-of-the-art manufacturing and assembly facilities – 1 in India and 4 overseas (Sweden, the Netherlands, the UK, and the USA) – supported by 2 integrated R&D centres. The company also holds the distinction of being the first in India to design and manufacture advanced bulk material handling equipment, reinforcing its position as a pioneer in industrial engineering.

Products and Services

The company’s products can be categorized under the following business segments:

- Gear Boxes – Helical, spiral bevel helical, worm, parallel shaft, planetary, high-speed gears and gear boxes, couplings, pinion shafts, etc.

- Material Handling Equipment – Stacker cum reclaimer, specialised conveyors, sizers, tandem wagon tipplers, etc.

Subsidiaries: As of FY25, the company has 12 subsidiaries and an associate company.

Investment Rationale

- Strong Order Inflow Provides Robust Revenue Visibility – The company reported a strong order intake of Rs.688 crore in Q2FY26, marking a 28% YoY growth, driven by healthy demand across both domestic and international markets. Domestic orders stood at Rs.516 crore (up 32% YoY), while overseas orders came in at Rs.172 crore (up 18% YoY). The company’s open order book as of September 30, 2025, stood at Rs.1,226 crore, compared to Rs.966 crore in the previous year, indicating a solid pipeline and sustained business momentum. Notably, the MHE segment witnessed strong traction with order inflows of Rs.191 crore, almost doubling from Rs.104 crore in Q2FY25. Management commentary indicates continued strength in inquiries and improving demand from sectors that were previously subdued.

- Strategic Focus on Export Expansion – The company aims to increase the contribution of exports to 50% of total revenue by 2030, reinforcing its long-term growth strategy through global diversification. While overseas business remained largely flat during Q2FY26 due to timing-related delays in order receipt and execution amid geopolitical uncertainties in select markets, the inquiry pipeline remains strong. The company expects a meaningful pickup in execution momentum in H2FY26 as conditions stabilize. The company’s export strategy focuses on expanding presence in underpenetrated regions such as South America, select European countries, parts of the Middle East, and the Far East, while continuing to strengthen its base in Europe and North America.

- Q2FY26 – In Q2FY26, Elecon reported revenue of Rs.578 crore, reflecting a 14% YoY growth from Rs.508 crore in Q2FY25, supported by healthy performance across divisions. The gear division grew 9% YoY, while the MHE segment expanded 33% YoY, driven by strong order execution. A timing gap between order intake and execution temporarily impacted revenue recognition during the quarter. Operating profit rose 13% YoY to Rs.126 crore (vs. Rs.112 crore in Q2FY25), while net profit remained steady at Rs.88 crore.

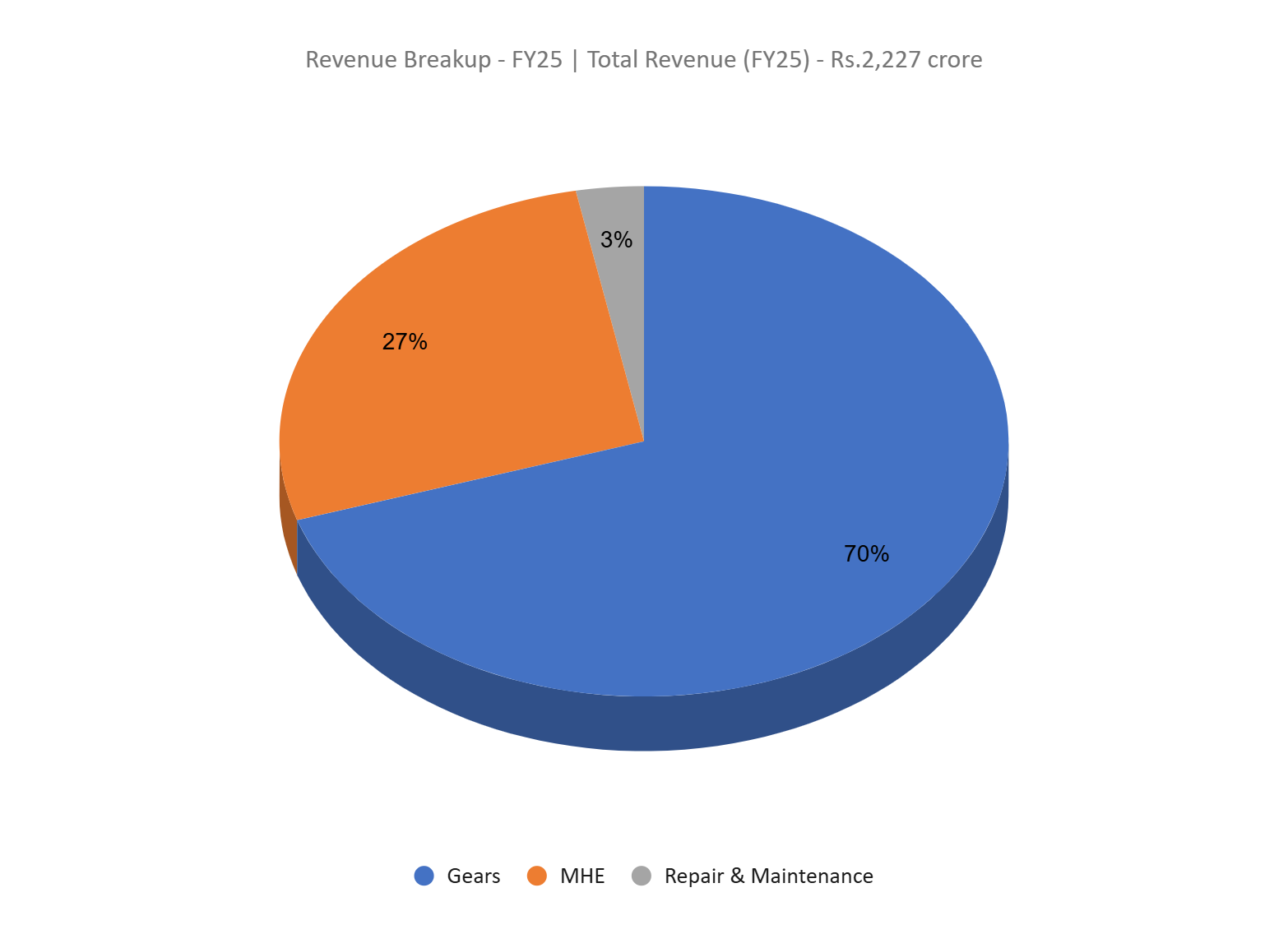

- FY25 – During FY25, Elecon recorded revenue of Rs.2,227 crore, reflecting a 15% YoY growth over FY24, driven by robust demand across both domestic and international markets. Operating profit stood at Rs.543 crore, up 14% YoY, while net profit rose 17% YoY to Rs.415 crore, supported by strong execution and cost efficiency. The domestic business contributed 83% of consolidated revenue, with the remaining 17% derived from overseas markets. As of March 31, 2025, the company’s consolidated order book stood at Rs.948 crore, up from Rs.796 crore a year earlier, representing a 19% YoY increase.

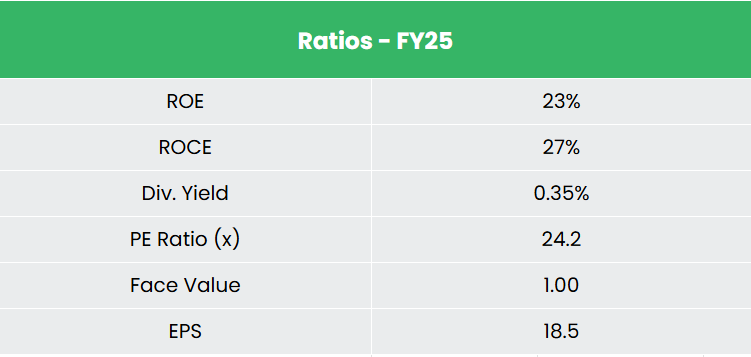

- Financial Performance – The 3-year revenue and net profit CAGR stands at 22% and 42% respectively between FY23-25. The company has a robust capital structure with a debt-to-equity ratio of 0.11. Average 3-year ROE and ROCE is around 23% and 28% for FY23-25 period.

Industry

The Indian electrical equipment market is poised for robust growth, with an expected incremental expansion of Rs.6,44,533 crore (US$76.24 billion) at a CAGR of 14.3% between FY24 and FY28. The capital goods manufacturing industry forms the backbone of India’s engagement across diverse sectors such as engineering, construction, infrastructure, and consumer goods. Rising demand in industries like infrastructure, power, mining, oil and gas, steel, automobiles, and consumer durables is driving the growth of engineering services. India’s competitive edge in manufacturing costs, market expertise, technology, and innovation continues to strengthen its global position. Increased investments in infrastructure and industrial production have further fuelled the sector’s expansion, underscoring its strategic importance to the national economy. Additionally, India has emerged as a preferred hub for design, research, and development (R&D) for global equipment manufacturers, with multinational corporations increasingly leveraging local capabilities for innovation and process development.

Growth Drivers

- The government has de-licensed the engineering sector with 100% FDI permitted.

- In the Union Budget FY26, the government announced allotment of Rs. 11,21,000 crore (US$ 128.42 billion) (3.1% of GDP) towards capital expenditure.

- The ‘Make in India’ initiative, along with the government’s emphasis on improving the ease of doing business, is expected to create numerous opportunities in the engineering and capital goods sectors in the coming years.

Peer Analysis

Competitors: Transformers & Rectifiers India Ltd, Shanthi Gears Ltd, etc.

Compared to its listed peers, Elecon appears undervalued relative to its revenue-generating potential and strong financial performance.

Outlook

With over six decades of operations and high entry barriers in its core segments, Elecon remains well-positioned for sustainable growth. Despite a muted start to FY25, the company ended the year strongly supported by operational efficiency and robust demand. A strong order inflow provides clear visibility toward achieving its FY26 revenue guidance of Rs.2,650 crore. Backed by three global brands, Elecon continues to strengthen its global footprint through R&D-driven innovation and strategic tie-ups with leading OEMs. Domestic demand from core sectors such as power, steel, and cement remains healthy, while exports continue to deliver higher margins. With a net cash position of around Rs.600 crore and a planned capex of Rs.400 – 1,000 crore for FY26 – FY28 toward new facilities in Chennai, Ambernath, and Nagpur, the company is well-placed to sustain margins, enhance capacity, and deliver consistent growth in both domestic and international markets.

Valuations

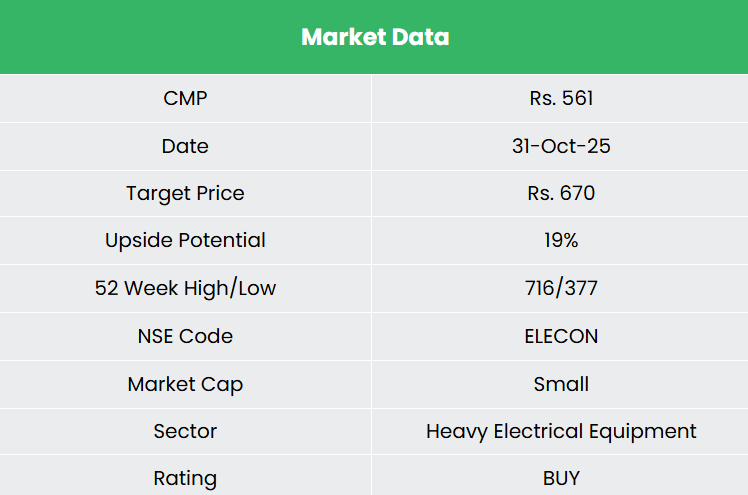

We believe the company is well placed to maintain its growth momentum, supported by a strong order book and proven execution capabilities. We recommend a BUY rating in the stock with the target price (TP) of Rs.670, 29x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

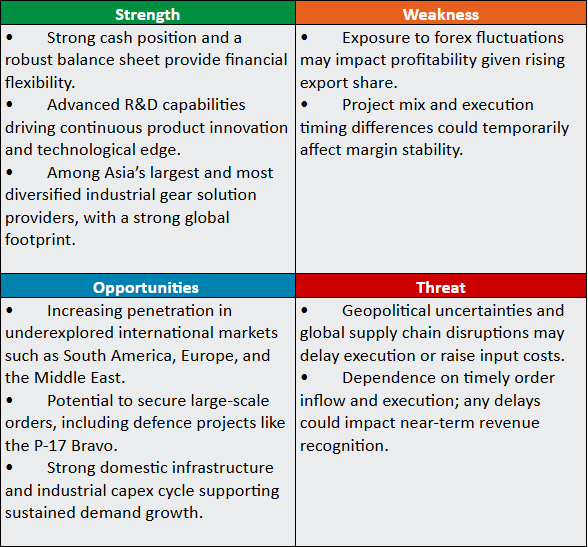

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.