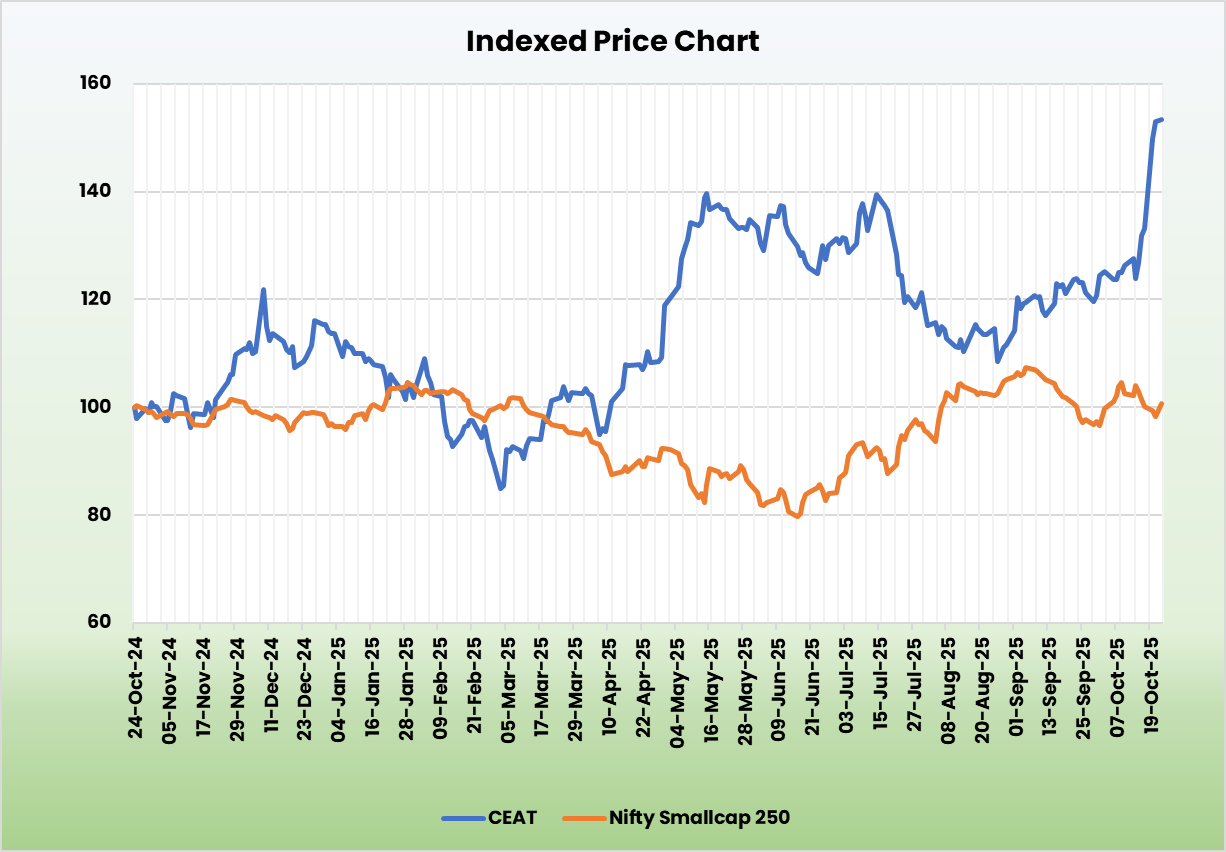

CEAT Ltd – Driven by Purpose, Powered by Progress

Founded in 1958 and headquartered in Mumbai, CEAT Ltd. is one of India’s premier tyre manufacturers. The company serves a diverse range of segments, including two- and three-wheelers, passenger and utility vehicles, commercial vehicles, and off-highway vehicles. As a flagship entity of the RPG Group, the company has a strong global footprint, operating in over 110 countries, with key markets spanning the United States, Latin America, Africa, the Middle East, India, Southeast Asia, and Europe. Its extensive distribution network comprises more than 5,700 dealers, over 61,000 sub-dealers, and 1,115+ retail outlets across India. CEAT operates six manufacturing facilities and offers a wide product portfolio with over 2,300 unique tyre variants, backed by 52 granted patents.

Products and Services

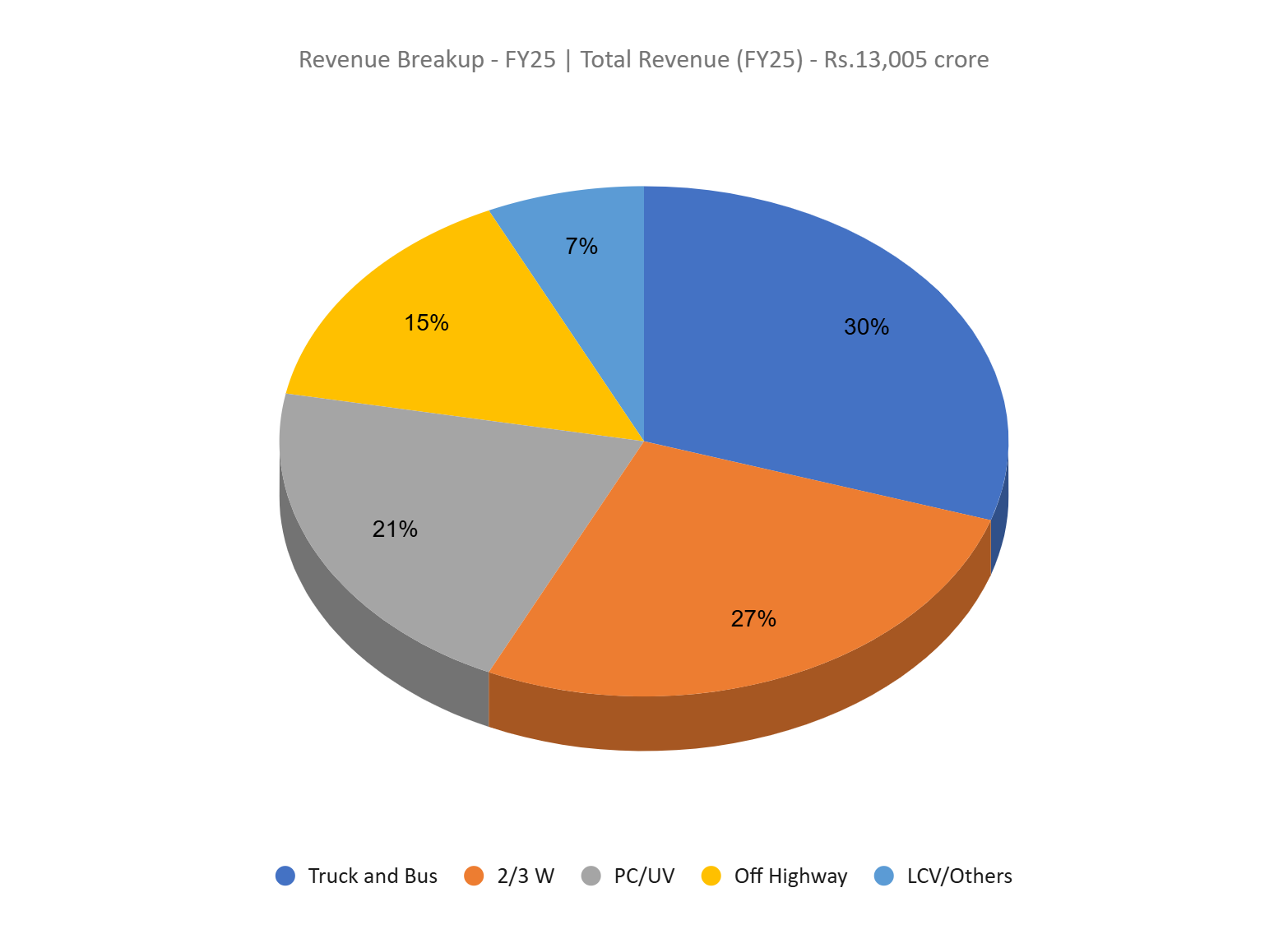

The company manufactures and supplies a diverse range of tyres, tubes and flaps for truck and buses, 2/3W, passenger cars and utility vehicles, off highway, LCV and others.

Subsidiaries: As of FY25, the company has 10 subsidiaries and 1 joint venture.

Investment Rationale

- Strategic alliances – The company recently completed the acquisition of Michelin Group’s CAMSO Construction Compact Line (CCL) business, marking a strategic milestone in its transformation into a global Off-Highway Tyre (OHT) leader. The acquisition comprises two advanced manufacturing facilities in Sri Lanka (Midigama and Kotugoda) and includes global rights to the CAMSO brand, under a three-year licensing arrangement following which permanent ownership will transfer to CEAT. The CAMSO business recorded ~US$213 million in CY2023 revenues and currently operates at ~60% capacity utilisation, which CEAT expects to ramp up in the coming quarters. The transaction is expected to be margin accretive and to boost CEAT’s topline by 10 – 15% in the medium term. Importantly, with CAMSO’s strong brand equity across Europe and North America, CEAT gains access to 40+ global OEMs and premium distributors, significantly enhancing its international reach and accelerating its vision to be a global leader in Off-Highway mobility.

- Capacity additions – CEAT is undertaking calibrated capacity expansions across key product segments to meet rising domestic and export demand. The company commissioned a new Truck & Bus Radial (TBR) facility in FY25 with an initial capacity of 1,500 tyres/day, and plans to scale output by an additional 2,000 units/day at its Chennai plant by FY26. Passenger Car Radial (PCR) capacity at Chennai is also slated to rise 30–40% over the same period. Meanwhile, a Rs.500 crore investment at the Nagpur plant will enhance capacity by ~30%, and expansion at Ambernath will support export-led growth. These initiatives are expected to strengthen CEAT’s competitive positioning across passenger, commercial, and farm tyre segments, enabling it to capitalize on the structural uptick in replacement and OEM demand.

- Q2FY26 – During the quarter, the company generated revenue of Rs.3,773 crore, an increase of 14% compared to the Rs.3,305 crore of Q2FY25 – backed by a robust growth in the OEM and international segments. Operating profit increased from Rs.368 crore of Q2FY25 to Rs.511 crore of Q2FY26, a growth of 39%. Gross and EBITDA margins expanded on account of operating leverage and cost efficiencies. The company reported net profit of Rs.186 crore, an increase by 52% YoY compared to Rs.122 crore of the corresponding period of the previous year.

- FY25 – During the FY, the company generated revenue of Rs.13,005 crore, an increase of 11% compared to the FY24 revenue. Operating profit is at Rs.1,496 crore, down by 11% YoY. The company reported net profit of Rs.473 crore, a degrowth of 26% YoY. The de-growth was due to the global uncertainties due to tariff and non-tariff situations in Q4FY25.

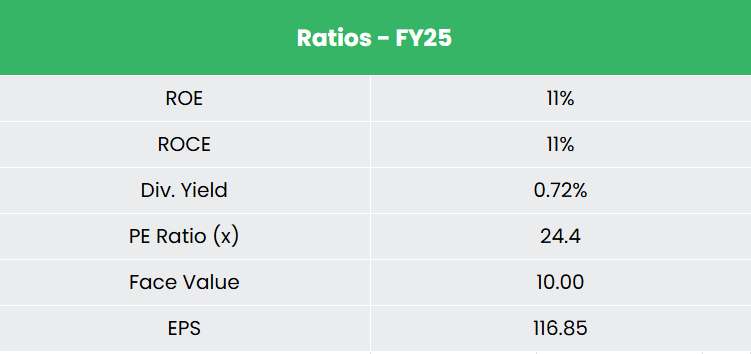

- Financial Performance – The 3-year revenue and net profit CAGR stands at 12% and 79% between FY23-25. Average 3-year ROE and ROCE is around 12% and 15% for FY23-25 period. Debt to equity ratio is at 0.49.

Industry

India’s growing working population and expanding middle class continue to be significant drivers of demand in the automotive sector. As the world’s third-largest automobile market by both value and volume, India is rapidly establishing itself as a key global hub for auto component sourcing. The industry currently exports over 25% of its production annually, with export values projected to reach Rs.8,54,700 crore (US$ 100 billion) by 2030. Recent years have seen India emerge as the fastest-growing major economy globally, supported by rising incomes, increased infrastructure investments, and favourable manufacturing incentives. These factors have collectively accelerated growth in the automobile sector, making it a vital pillar of the country’s broader economic expansion. The surge in domestic and international demand has also fuelled the growth of original equipment manufacturers (OEMs) and auto component producers, helping India develop deep industry expertise.

Growth Drivers

- 100% FDI is allowed under the automatic route for auto components sector.

- The reduction in the tax burden in the 2025-26 Union Budget is expected to boost spending among the expanding middle class population.

- Reduced GST rates on automobiles and tyres will lower costs for consumers, boosting demand and driving growth in both new vehicle sales and tyre replacements.

Peer Analysis

Competitors: MRF Ltd, Apollo Tyres Ltd, etc.

Compared to its competitors, CEAT appears reasonably valued and demonstrates stronger capital allocation efficiency, as reflected in its performance metrics and sales growth.

Outlook

CEAT’s growth outlook remains constructive, supported by the CAMSO acquisition, ongoing capacity expansions, and healthy demand across OEM and replacement segments. The CAMSO transaction enhances CEAT’s global presence in the premium Off-Highway Tyre market and is expected to be margin accretive in the medium term. Q2FY26 performance reflected robust topline growth and margin improvement, indicating operating leverage benefits. Despite near-term headwinds in FY25 from global trade disruptions, balance sheet metrics remain healthy with prudent leverage and improving returns. With planned capex of Rs.1,000 crore in FY26, CEAT is positioned to deliver steady volume-led growth and margin stability over the medium term.

Valuations

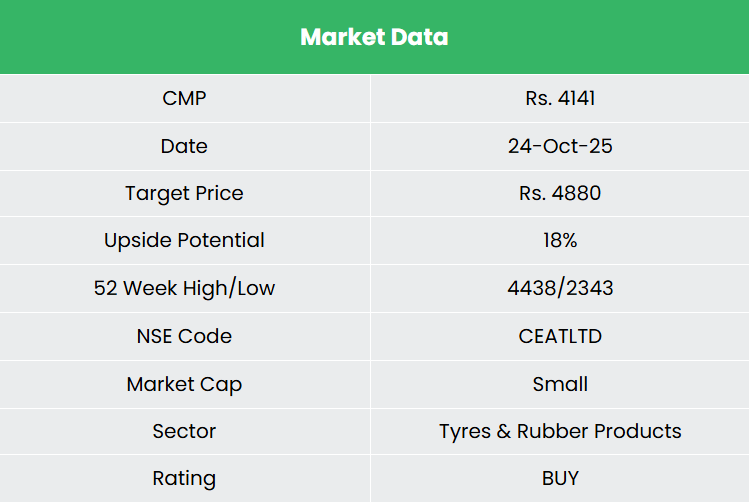

With a strong market position, expanding capacity base, and improving brand equity, we believe CEAT is well positioned to benefit from the anticipated upcycle in automobile demand. We recommend a BUY rating in the stock with the target price (TP) of Rs.4,880, 26x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

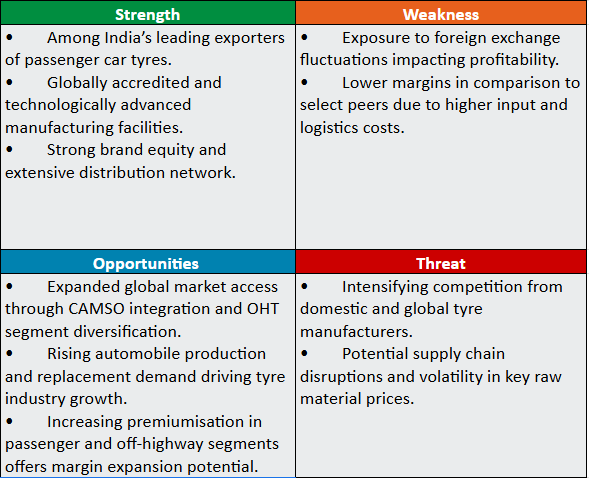

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.