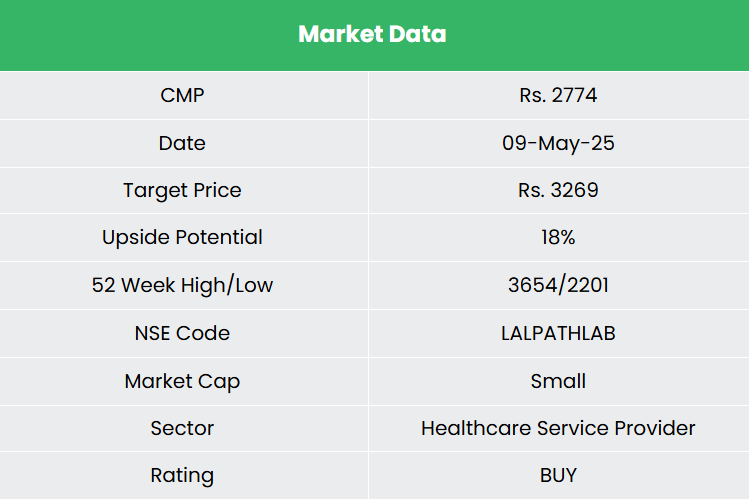

Dr Lal Pathlabs Ltd – Quality Diagnostics Services

Incorporated in 1995 and headquartered in New Delhi, Dr Lal Pathlabs Ltd. is one of India’s leading consumer healthcare brands in diagnostics services. The company operates a national ‘hub and spoke’ network, including its National Reference Laboratory in Delhi and Regional Reference Laboratories in Kolkata, Bangalore, and Mumbai. It serves a diverse clientele, including individual patients, hospitals, healthcare providers, and corporate clients. As of 31 March 2025, the company has a catalogue of 385 test panels, 3,172 pathology tests and 1,455 radiology and cardiology tests serviced by 298 clinical labs and 6,607 patient service centres.

Products and Services

The company provides a wide array of diagnostic and preventive healthcare services, including routine blood tests, specialized screenings (such as thyroid, diabetes, liver, kidney, and cancer tests), full body checkups, infectious disease diagnostics (like COVID-19, dengue, and tuberculosis), and advanced tests supporting chronic disease management, fertility assessments, and autoimmune disorders.

Subsidiaries: As of FY24, the company has 11 subsidiaries.

Investment Rationale

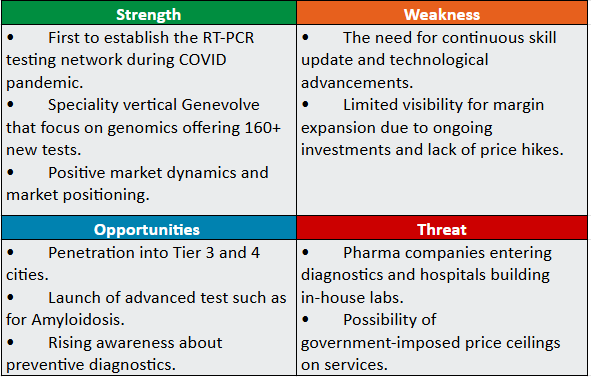

- Growth strategies – The company aims to maintain its pricing strategy to drive volume growth while ensuring affordability. It is focused on expanding access to a broader patient base and reinforcing its position as a leading diagnostic brand in India. Additionally, it seeks to leverage its growing expertise in specialized areas such as genomics, reproductive diagnostics, autoimmune disorders, and other advanced testing. The company is also targeting expansion into underpenetrated Tier 3 and Tier 4 cities, with particular emphasis on high-potential markets in the western and southern regions. It has adopted an aggressive approach toward expanding its collection network and infrastructure, with benefits expected to materialize in the coming quarters. Furthermore, the company plans to introduce its bundled test offerings – SwasthFit in these Tier 3 and Tier 4 markets.

- Launch of advanced tests – The company recently became the first in South Asia to launch advanced diagnostic tests for Amyloidosis. It has introduced Amyloid Typing using Laser Capture Microdissection and Mass Spectrometry – an innovative test that enables precise identification of various types of Amyloid proteins. To ensure nationwide accessibility, the company allows sample collection from any location in India, with all samples sent to its National Reference Laboratory in New Delhi. This specialized test is offered under the expert guidance of the National Amyloidosis Centre in London, UK. This is expected to strengthen the company’s position as a leader in specialized diagnostics, tapping into a high-value niche market while enhancing clinical credibility through international collaboration and nationwide accessibility. This move not only differentiates the brand but also drives growth through innovation and improved patient care.

- Q4FY25 – The company reported a revenue of Rs.603 crore marking an increase of 11% compared to the Rs.545 revenue of Q4FY24. The growth was primarily driven by mix improvement and volume growth. EBITDA stood at Rs.169 crore against the Rs.145 crore of Q4FY24, a growth of 17% YoY. Net profit stood at Rs.115 crore which is a growth of 34% as compared to the Rs.86 crore of the same period in the previous year. Revenue per patient has grown by 6% during the period to Rs.887 crore, due to favourable mix tests and geography mix.

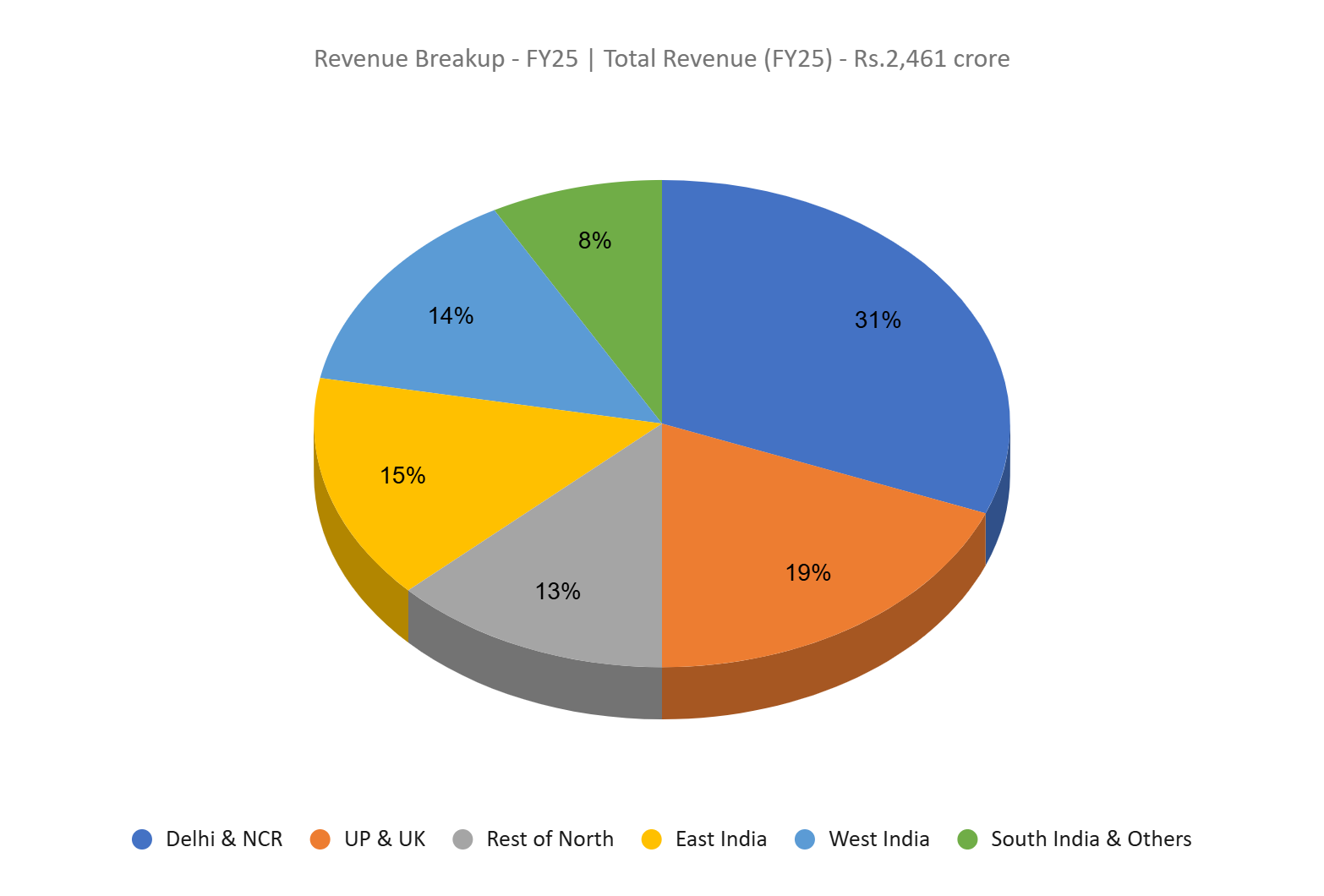

- FY25 – The company generated revenue of Rs.2,461 crore during FY25, an increase of 11% compared to the FY24 revenue. EBITDA was at Rs.696 crore, up by 14% YoY. The company reported net profit of Rs.451 crore, an increase of 25% YoY. Notably, the company achieved margin expansion during the period with EBITDA margin improving from 27% to 28% and net profit improving from 16% to 18%.

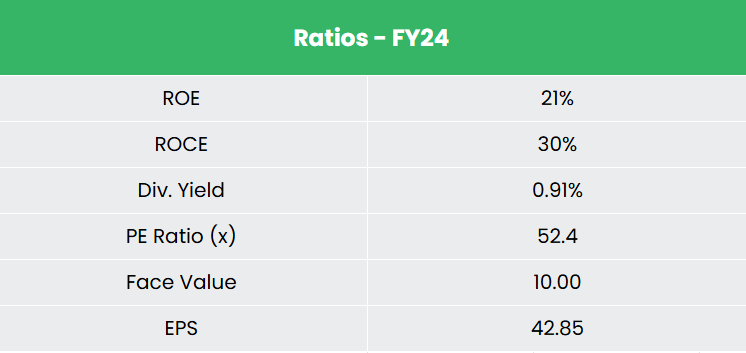

- Financial Performance – The revenue and net profit CAGR of the company for the past 3 years is around 6% and 12% between FY22-FY25 with the TTM growth being 11% and 36%. The 3-year average ROE and ROCE for the company is around 20% and 24% for the past 3 years. The company has a robust capital structure with a debt-to-equity ratio of 0.07.

Industry

The Indian healthcare sector, one of the country’s largest in terms of both revenue and employment, is expanding rapidly due to enhanced coverage, improved services, and increasing investments from both public and private sectors. The affordability of medical services has fuelled the growth of medical tourism, drawing patients from around the globe. Factors such as rising incomes, an aging population, greater health awareness, a shift toward preventive care, and wider health insurance coverage are expected to drive demand for healthcare services in the future. India’s hospital market which was valued at US$ 98.98 billion in 2023 is projected to grow at a CAGR of 8.0% from 2024 to 2032, reaching an estimated value of US$ 193.59 billion by 2032. The country has also become one of the leading destinations for high-end diagnostic services with tremendous capital investment for advanced diagnostic facilities, thus catering to a greater proportion of the population.

Growth Drivers

- Increasing healthcare awareness, rising demand for preventive healthcare and advancements in diagnostics technologies.

- India’s Union Budget 2025-26 emphasizes transforming the healthcare sector through increased digital infrastructure and a revised health expenditure of Rs.89,287 crore (US$ 10.70 billion), aiming to enhance accessibility and innovation in healthcare services.

- Government initiatives such as Ayushman Bharat, MedTech Mitra, The Pradhan Mantri Jan Arogya Yojana etc, aimed to enhance healthcare quality, ease of doing business and reduced import dependence while fostering indigenous development of affordable and high-quality diagnostics devices.

Peer Analysis

Competitors – Vijaya Diagnostic Centre Ltd, Thyrocare Technologies Ltd, etc.

The company demonstrates consistent sales growth and robust investment returns than its competitors, reflecting effective capital allocation and expanding market penetration.

Outlook

In FY25, the company demonstrated strong expansion momentum by opening 18 new laboratories, significantly enhancing its footprint in Tier 3 and Tier 4 cities while further consolidating its network in Tier 1 and Tier 2 locations. With the strategic advantage of being an early mover in underserved regions, the company continues to strengthen its presence across geographies. Additionally, the company added 845 patient service centres – a 14% YoY increase – highlighting robust network growth. For FY26, management has guided for revenue growth of 11 – 12% and operating margins around 27%. Looking ahead, the company plans to maintain its pace by adding approximately 18 new labs annually over the next 1 – 2 years, indicating a sustained focus on expansion and operational efficiency.

Valuation

We believe the company possesses a strong market position with its extensive network, comprehensive test offerings, and technological investments. We recommend a BUY rating in the stock with the target price (TP) of Rs.3,269, 55x FY27E EPS.

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.