CRISIL Ltd. – An S&P Global Company

CRISIL is a leading, agile and innovative global analytics company driven by its mission of making markets function better. It is the India’s foremost provider of ratings, data, research, analytics and solutions. A strong track record of growth, culture of innovation and global footprint sets the company apart. The company has delivered independent opinions, actionable insights and efficient solutions to over 100,000 customers. Their businesses operate from India, Argentina, Australia, China, Hong Kong, Poland, Singapore, Switzerland, the United Arab Emirates (UAE), The United Kingdom (UK) and the United States of America (USA). The company is majorly owned by S&P Global Inc., a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide.

Products & Services:

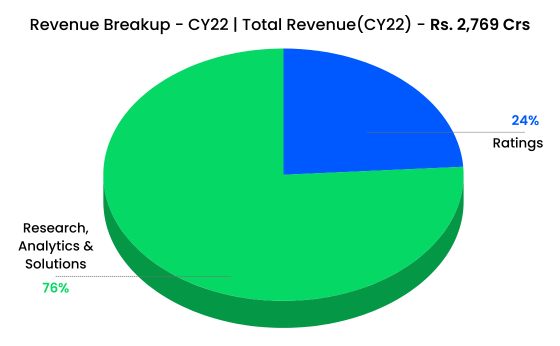

CRISIL provides a wide range of services. These Services include independent equity research, bond ratings, Credit research, Risk and analytics, Economy and industry research, Bank loan ratings, fund research etc. The company operates in two main segments such as Ratings and Research, Analytics & Solutions.

Subsidiaries: As on CY22, the company had one Indian and 13 overseas wholly owned subsidiaries.

Key Rationale:

- Leadership Position – Over the decades, company has maintained a strong growth momentum by focusing on new client acquisition and maintaining traction in securitization market led by strong operating leverage benefits. The business saw a growth in corporate bond ratings, which will lead to an increase in market share and result in maintain its leadership position in the ratings space. Their superior rating standards, diversified and innovative product offerings and strong analytics skills has seen it emerge as the strongest credit rating agency (CRA) across business cycles. CRISIL is majority owned by S&P Global Inc, a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide. Thus, CRISIL’s association with S&P Global helps blend local and global perspectives in shaping CRISIL’s strategy and governance systems.

- Segment Updates – Softening inflation and the Reserve Bank of India (RBI) pausing its rate hike cycle have led to easing of corporate bond yields, which, in turn, encouraged issuances in Q2CY23. The number of issuers have increased from 380 in H1CY22 to 530 in H1CY23. Simultaneously, the bond issuance quantum have grown at 93% YoY. Global Benchmarking Analytics (GBA) continues to strengthen its client engagement through actionable analytics and intelligence. Market Intelligence & Analytics (MI&A) saw momentum in its credit, risk, and research and consulting offerings. CRISIL Ratings hosted webinars on sectors such as oil, airports and automobiles, held the CRISIL Ratings Conclave at Kolkata, and released the Ratings Roundup for the second half of last fiscal.

- H1CY23 – CRISIL’s consolidated income from operations for the half year ended June 30, 2023 (H1CY23), rose 17.6% to Rs.1485.9 crore, compared with Rs.1263.5 crore in the corresponding period of the previous year. Segment wise, Rating services segment reported a growth of 19.3% YoY to Rs.377 crore and Research, Analytics & Solutions reported a growth of 17% YoY to Rs.1108.7 crore. Profit after tax increased 14.6% to Rs.296.3 crore in H1CY23, compared with Rs.258.5 crore in the corresponding period of the previous year. During Q2 2023, the impact of foreign exchange movement was not favourable compared with the same quarter last year.

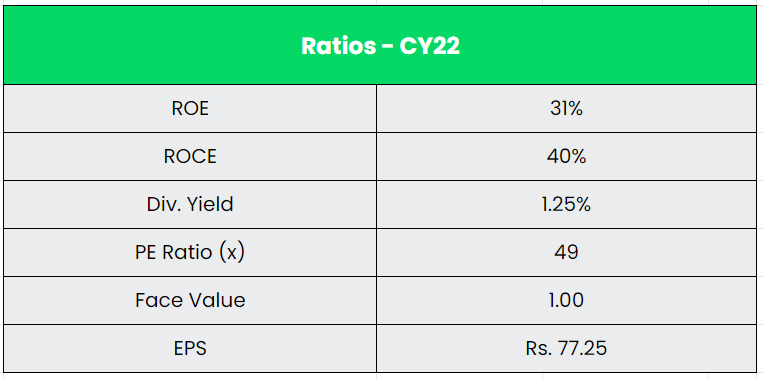

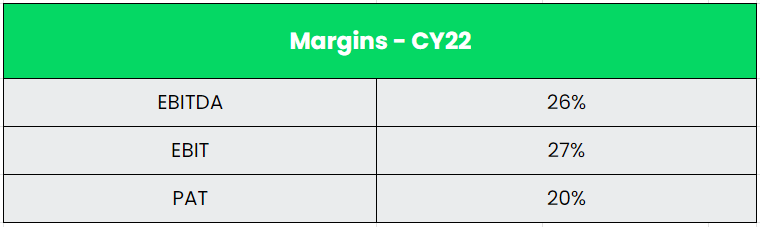

- Financial Performance – CRISIL is a zero-debt company since its inception. The Company has been incurring capex through internal accruals. It is also expected that company to continue with the same strategy of being an un-levered firm with consistency in capex across the various business segments. The revenue and PAT CAGR have grown at 11% and 14% between CY17-22. Also, the company maintained an average ROCE of ~40% and an average ROE of ~30% for the past 5 years.

Industry:

The country’s financial services sector consists of capital markets, insurance sector and non-banking financial companies (NBFCs). The credit rating industry grew significantly in FY2023 despite the inflationary pressures and the fears of global recession due to the geo-political challenges arising out of the Russia-Ukraine war. The growth in rated volumes for the industry was backed by growth in bank credit outstanding by more than 15% and bond issuances by 28%. High global interest rates as global central banks tackled inflation and uncertainty on exchange rates pushed the domestic borrowers to the domestic funding market. The Indian bond market is currently valued at approximately $2.34 trillion, with $1.83 trillion allocated to government bonds and $510 billion to corporate bonds. With the government looking to further develop the country’s infrastructure, a larger impetus will be on raising this capital from retail investments.

Growth Drivers:

- Easing inflation and the pause in the rate hikes will support the bond issuances.

- At the beginning of this year, the Government had announced an issuance calendar for Sovereign Green Bonds (SGrBs) in order to mobilize resources for green infrastructure. It is expected to raise Rs.16,000 crore in two tranches.

- Commercial paper issuance is picking up steam among Indian corporates and a growing number of domestic firms are turning towards these short-term debt instruments to meet their working capital needs even as risk averse banks continue to sit on a huge liquidity.

Competitors: ICRA and Care Ratings.

Peer Analysis:

Though CRISIL has historically traded at premium to its peers – ICRA and CARE, its diversified revenue mix, healthy margins, superior return ratios, and strong parentage justifies the value. The revenue per employee is the core metric for companies with fixed cost centric business. Clearly, CRISIL is the winner in the said metric with Rs.64.70 lakhs of revenue generating from a single employee.

Outlook:

The company recently completed the acquisition of 100% stake in Peter Lee Associates, an Australian research and consulting firm. This acquisition will accelerate their strategy in the Asia-Pacific region to be the foremost player in the growing market of benchmarking analytics across the financial services globe. The company is also eyeing a clear opportunity in the ESG Ratings space. ESG is evolving globally and in India. The company has already launched scores for 580 plus companies. Globally, there is demand for ESG evaluation, ESG ratings, third party opinions, on various aspects related to sustainability and ESG. The company is waiting for the final regulatory details on the ESG space which includes pricing the product.

Valuation:

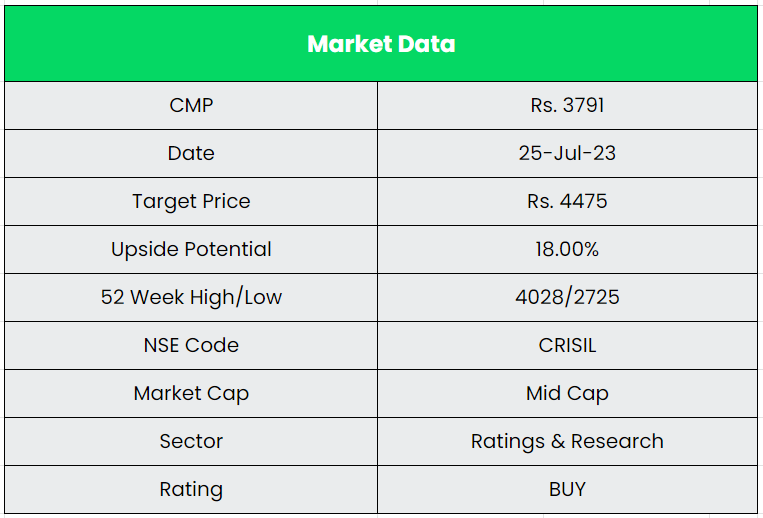

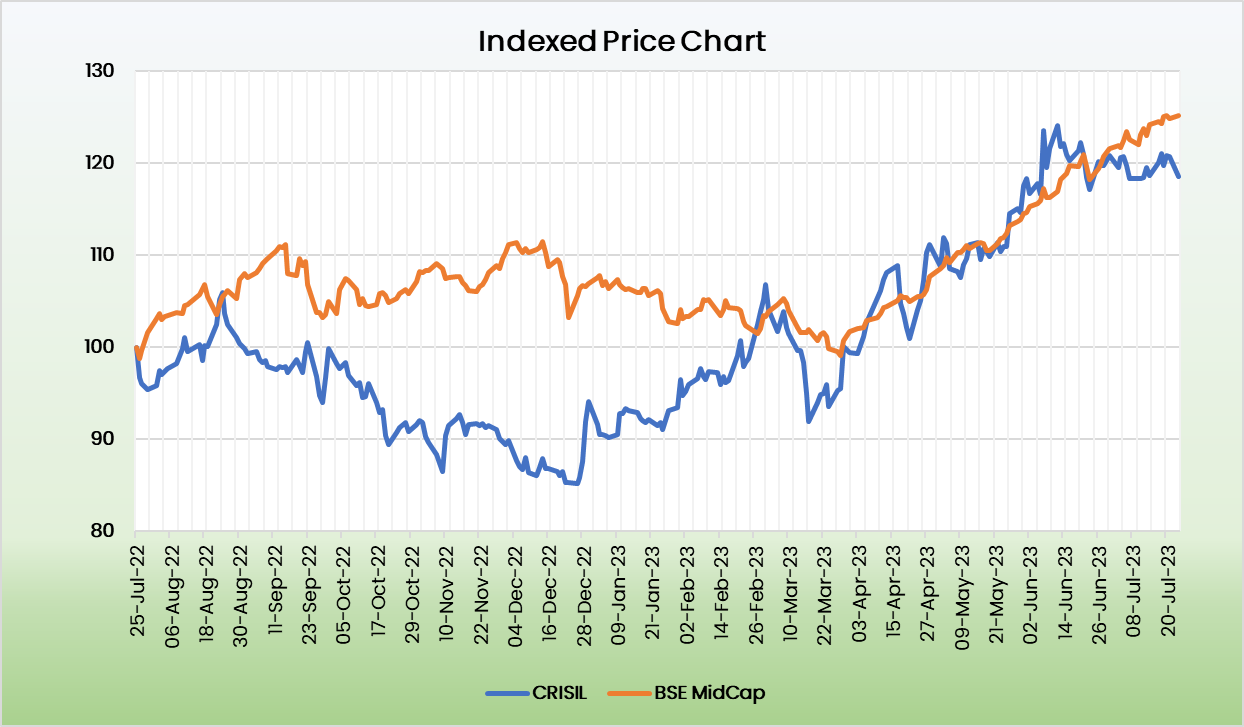

CRISIL remains the largest beneficiary of the strong uptick in the systemic credit growth. This coupled with all round improvement in the research segment and opportunities in the advisory division will drive overall revenue/earnings growth higher. We recommend a BUY rating in the stock with the target price (TP) of Rs.4475, 45x CY24E EPS.

Risks:

- Operational Risk – Ratings are primarily used as indicators to determine early warning signs of worsening health of corporates. Failure to indicate early warning signal can result in loss of trust in the rating agency and thus impact rating revenue growth.

- Attrition Risk – Employees are the core asset for a credit rating agency and hence attrition can be a huge risk. While CRISIL remains the best paymaster, the employee movement (especially at the middle / senior management level) can expose it to grave risk.

- Economical Risk – Rating revenues for credit rating agencies are directly reflected in the state of the economy and its growth.