Income tax is important. It is what we are compulsorily required to pay to our Government for all the services we receive from them. But here’s the irony – none of us are taught ANYTHING about it. For most part of our early lives, it is a “hush-hush” phrase – something that we all hear around us, yet, no one quite explains it to us. The result? We are overwhelmed by tax woes as soon as we start working. We end up doing one of two things:

- Paying a large chunk of our income towards taxes

- Saving our money in the ‘wrong’ options to save taxes – A ‘wrong’ tax-saving option is an option that is unhealthy for long-term wealth building as it does not deliver good enough returns.

Both these options aren’t good for your hard-earned money, no?

Let’s have the all-important “tax-talk” now. This article is all you need to:

– know all about income tax, and

– to make smart investment decisions to save taxes prudently

Know your income tax

In India, tax deductions on your income are calculated based on your age, and your income level. Here’s a table that will help you estimate your tax slab, i.e., the percentage of taxes you are required to pay on your income every year.

Deduce your deductions

There are MANY avenues offered by the Income Tax (IT) Act to save on taxes (the legitimate way, of course), and claim deductions. Here’s a list of some of the more important and widely applicable Sections of the Act that give you deductions.

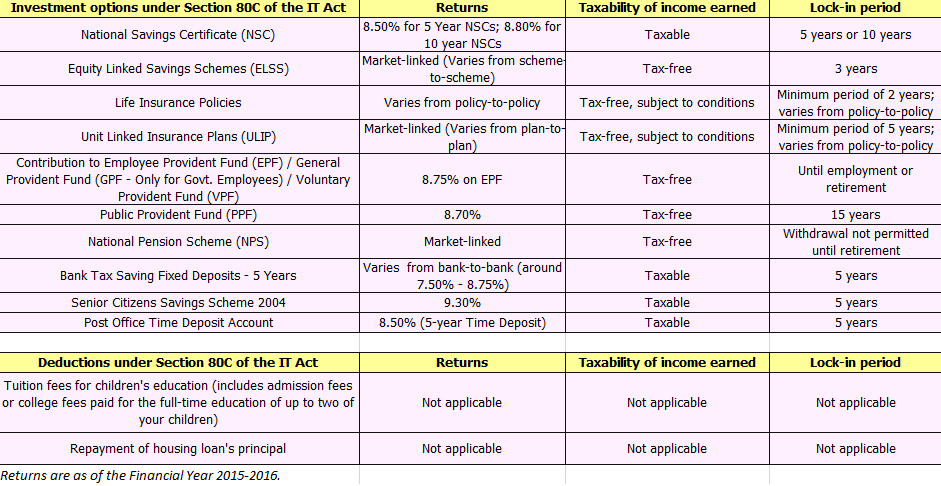

– Section 80C – All individuals can save up to Rs. 1,50,000 of their taxable income in the investments, insurance, and other expenses listed under this Section of the Act. Here’s a quick table that will tell you the main options available.

You can access our Section 80C calculator to calculate your taxable income (after deducting investments and deductions) by clicking here. For comprehensive information on all the investments that get you tax deductions under Section 80C of the IT Act, please click here.

Look at the above table closely again. If you pay close attention to it, you’d realise that not all the tax-saving investment options really reward you enough. The answer therein lies in making a smart choice, i.e., ELSS (Equity Linked Savings Schemes, or tax-saving funds).

Says Bhavana Acharya, our Mutual Fund Analyst, “One must-have is life insurance. But there is certainly no need to keep adding to the line of policies you have just to save on taxes. Then there is the EPF which most salaried individuals will also have. So, what about the remaining amount of that Rs. 1,50,000 that you can claim? If you want smart investment options for the long term, then you should consider ELSS as a part of your tax-saving portfolio. It has three main factors rooting for it. One, an ELSS has a relatively shorter lock-in period of three years. Two, an ELSS does not suffer from any taxes, whether on dividend paid, or at the time of redemption. Three, an ELSS delivers superior returns over the long term, albeit for some higher risk. This is because an ELSS invests almost its entire portfolio in equities, which is a superior asset class. For this reason, it delivers better returns than all the other traditional tax-saving options, which are mostly pure-debt instruments that do not always beat inflation too.”

To know the best ELSS chosen by our experts to invest in this year, please click here.

– Section 80D – You can claim deductions for the mediclaim premium that you’ve paid for yourself, your spouse, your dependent children, or your parents under this Section. The maximum amount that can be claimed for deduction is Rs. 25,000. For senior citizens (between 60 – 80 years of age), this amount stands at Rs. 30,000. For citizens beyond 80 years of age, a deduction of up to Rs. 30,000 can be claimed for medical expenditure.

For comprehensive information on insurance and tax deductions, please click here.

– Section 80E – If you, your spouse, or your children are pursuing higher studies, and if you’ve taken a loan for the same purpose from any financial institution, or an approved charitable institution, then you can claim deduction for the interest paid for the same under this Section of the Act. This will be applicable only if you’ve taken the loan in your name. There is no cap on the amount that can be deducted under this Section. Also, this deduction can be claimed for a time period of eight years, i.e., if the repayment of your loan exceeds eight years, then the interest is not deductable from the ninth year onward.

– Section 10 (13A) – As salaried employees you will usually receive a House Rent Allowance (HRA) as a part of your pay package. This amount may vary based on your designation. The idea of the HRA is to help you meet the cost of a rented house that you may take. Since this is towards an expense you incur, if you rent an accommodation, the Income Tax Act allows exemption on the HRA you receive under Section 10 (13A) of the Income Tax Act and Rule 2A of the Income Tax Rules.

For comprehensive information on tax deductions rules for HRA, please click here.

– Section 24(b) – While the principal amount in the repayment of a home loan is eligible for deduction under Section 80C of the IT Act, this Section allows the interest paid on such a loan to be deducted from taxable income. If the house purchased is self-occupied, then a maximum amount of Rs. 2,00,000 can be claimed for deduction. If the house has been purchased with a joint loan shared by you and your spouse, then both of you can claim a maximum amount of up to Rs. 2,00,000 as deduction. If you have rented out the property for which you’ve borrowed a loan and are paying interest, then you can claim deduction for the full interest paid on your home loan.

For comprehensive information on home loan deductions, please click here.

Remember, remember: to claim tax deductions under any of the above-mentioned Sections of the IT Act, you must have invested / paid for the deductions before March 31 of that financial year.

File your returns

The last date for individuals to file their income tax returns for the year is July 31 of any financial year (August 31 this year). The IT Department of India has made it relatively easy to file your taxes online now with their site. We’ll be releasing another post that will have a step-by-step guide on filing your taxes online soon.

So, you see? That’s all there is to the hush-hush “tax talk”. Not so taxing now, is it? Make sure you start planning for your taxes early on, make the right tax decisions, and most importantly, have the tax talk with your young ones. A little education does go a long way.

Other than this there is Rs15000 deduction for claiming medical bills.

Other than this there is Rs15000 deduction for claiming medical bills.

Very informative article

Very useful information. Thanks. Very nicely articulated.

Thanks.

This is indeed very useful. I am aware of section 80C & 80D. But this is really good for additional information. Have bookmarked it.

Thanks again.

Thanks.

This is indeed very useful. I am aware of section 80C & 80D. But this is really good for additional information. Have bookmarked it.

Thanks again.

Very useful information. Thanks. Very nicely articulated.

Very informative article