It’s the season of tax-free bonds, or so it looks, going by the series of issues made by companies. So what exactly are these tax-free bonds and do they make for an attractive investment option now?

Tax-free bonds are bonds issued by companies, mostly, government enterprises, on which there is a fixed coupon rate (interest rate) and a long-term maturity of 10,15 or 20 years. As the money is raised for long-term infrastructure projects, these bonds have a long tenure. But given that they are issued by government-backed companies, the credit risk or risk of non-repayment is very low.

Companies such as IRFC, IIFCL, NHAI, REC, PFC, HUDCO, NHB, NTPC and NHPC are allowed to raise tax-free bonds in 2013-14. With the season just starting, REC, HUDCO and IIFCL have so far tapped the market and you may have more issues coming up in succeeding months.

The coupon rate of tax-free bonds are fixed by keeping the prevailing rates of government securities as a reference rate and reducing the same by about 55 basis points for retail investors.

The bonds are available for both residents and NRIs.

What’s tax free?

The term tax-free implies that the interest rate on the instrument is free of tax. That means, the income you receive does not suffer any form of tax. But that’s about it.

These bonds are not to be confused with tax-saving instruments such as NSC or PPF. Tax-free bonds do not receive any deduction under Section 80C or any other provision. The principal does not enjoy any tax deduction nor does it suffer any tax at the time of redemption.

For you as an investor, tax-free bonds fall under the debt asset class and carry a fixed return just like deposits. But often times, investors tend to ignore this option as the coupon rate, on the face of it, may seem lower than other debt alternatives such as bank fixed deposits.

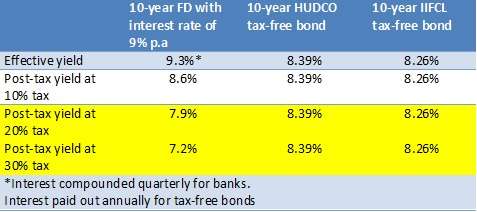

However, it is important for you to know that fixed deposit interest suffers tax, at your income tax slab rate. Hence, the net return for you, post tax, on deposits, is not the actually interest rate quoted but much lower. On the other hand, with a tax-free bond, given that their interest income is tax free, the coupon rate mentioned is actually the net return you get.

See table below to compare a 10-year fixed deposit from a nationalized bank versus the tax-free bond rates currently available. Clearly, for those in the 20% and 30% tax brackets, tax-free bonds turn out to be better options than FDs currently.

These bonds pay interest income annually throughout the period of their tenure. There is no cumulative option available.

These bonds pay interest income annually throughout the period of their tenure. There is no cumulative option available.

These bonds can be bought in physical mode or using your demat account (at FundsIndia, you can buy these bonds as long as you hold a demat account anywhere).

After the initial offer period, they are listed in the stock exchange. But given that they may not enjoy high liquidity in the bourses, you are better off holding these bonds till maturity.

Strategy

What should be your strategy with these bonds? Tax-free bonds are suitable for investors looking for steady source of income annually and can afford to lock-in their capital for at least 10 years at a stretch. If you do not need the interest income, make sure that you reinvest the interest income in high-yielding debt avenues such as debt mutual funds.

Given that the coupon rates of these bonds are fixed with reference to gilts; the rates are currently attractive as government gilts have high yields at present. This is what makes tax-free bonds attractive now.

Are tax-free bonds suitable for NRIs who are resident of USA? They would have to pay tax on these bonds to IRS at 30%. For US persons, is it better to go with taxable bonds?

Hello Vikas, If an NRI is looking at long-term investment that will provide high post-tax returns, then you will have to settle for equity mutual funds or equities. Or you will have to weigh fixed-income investment opportunities in the US and see how much the tax-free bonds will deliver against that, after IRS tax. For instance, post IRS tax, the returns on a 8.39% 10-year HUDCO tax-free bond will only be 5.8%. Would you have better fixed income opportunities in the US that will deliver post tax returns is something you need to consider.Thanks.

Thanks Vidya.

I am scared of the stock market – I dont see anything positive/high growth in the world these days.

Shouldn’t NRIs just go with taxable NCDs like Shriram/Muthoot etc which are giving ~12%. Based on my reading of the DTAA, IRS will take ~15% and GOI will take ~15%, post tax returns can be ~8.5%.

hello Vikas, Pl. remember that the risk of a tax-free bond and NCD is not alike. the former carried almost nil credit risk as they are issued by government enterprises. If you are ok with the risks, then it you may go for NCDs. thanks

Which Bond is good to invest (PFC/NHPC/IIFCL) up to 35 Lakhs Rs., Please suggest Bonds are better or Debt Funds, Equity Funds etc.

I Fall in to 30% bracket please suggest. Where I can place my funds – As of now I am keeping my funds in FSDs –

Vidya Could you suggest –

hello Nishant, Unless you need a yearly income flow, debt funds make more sense for long-term investing ,both on liquidity and return grounds, as mfs enjoy capital gains indexation for investment over 1 year. You can at best use tax-free bonds as a diversifier and go for the one with higher returns for 10 years (PFC/NHPC have higher returns) although IIFCL carries slightly lower risk than the other 2.

Equity funds are not to be compared with debt products as their risk-return profile is different. Every portfolio should have some exposure to equity if the time frame is long term. How much equity would depend on one’s risk appetite and time frame.

Thanks

Hi Vidya

I was just reading your article oIn this regard, I would request you to help me with some tax related inputs based on my case study.

I have recently got admitted in an US University for doing doctoral study. I am married and have a kid, who will remain in India presently. I have some bank balance and some shares in demat account. Now I need to generate steady source of income for my famility back in India. As I understand that my resident a/c will be designated as NRO account after I become an NRI.

Initially I thought of selling my shares and invest the sale proceeds in tax free bonds, which will generate steady returns sufficient for my family. I read that interest earned on my NRO deposit will be taxed at 30.90% unless tax residency certificate is provided. What I am not clear about is whether the interest from these tax free bonds( which would have otherwise remained tax free interest if I were an Indian Resident), which will get credited to my NRO account will become taxed and if so at what rate? is it flat 30.9% or as per prevailing income tax slabs?

Taxing the entire interest income from bonds will be very severe for me. Please suggest if you have any alternative planning for the given case study.

Hello Sumanta,

Sorry for the delayed response. First, not all tax-free bonds are available to NRIs. If they are, they are tax-free here as far as I understand. However, you may have to disclose it as income in the US and get taxed there. You would do well to consult an auditor in this regard. And of course tax-free bonds will close by March 31. Only if fresh approvals by govt. is made will you have any new issues after that. One option may be for you to make the investments through your spouse. thanks, Vidya

Hi Vidaya

Can you please explain the major difference between NCDs, Bonds and Fixed Deposits/ Term Deposits ? Also what would be the treatment of interest for tax purposes for each of these entities ? Submitting form 15H/G would entile you for no TDS for each of them ? Thanks

Hello Sivakumar, NCDs and bonds are issued by companies or NBFCs and based on the company’s financial performance may be risky or low on risk. Deposits of companies and NBFCs too fall in the same category in terms of risk. They are also not secured. That means, you will get your money after many other lenders, if the company does bust. But while NCDs and bonds are listed in the debt market, deposits are not. Terms deposits are deposits of banks.

The interest in all the cases, except tax-free bonds (interest is free of tax), are added to your income and taxed at your slab rate. You will have TDS if you cross Rs 10,000 per year as interest for bank deposits. For NCDS and corporate deposits, such limit is Rs 5000 per year. Pl. note that whether TDS is deducted or not, all such income is taxable. You have to declare the entire interest at the end of the year while filing tax and pay tax on it. thanks, Vidya

Hi

I am a little confused on where should I invest my money in.

My requirements are high returns and easy liquidity.

Which of the following should I go for :

PPF or Tax Free Bonds or FDs..

Please help..Thanks in advance

Hi Arpit, You have not stated the overall time frame of your investment. If you want reasonable returns with a short time frame like say 1 year, then ultra short-term funds are your best choice. These are debt funds that have reasonably low risk and highly liquid. Currently, they deliver returns of over 9% (1 year). In PPF and tax-free bonds your money is totally locked for the said time period. If you need money within few months, then liquid funds are options. thanks, Vidya

Would you have info on date /month of issue for upcoming tax free bonds for rest of the year? Would help to plan cash for investment..thanks..ramesh

Hi,

Can you please confirm that there are no put-and-call option in these tax free bonds indicating the bonds will not be recalled earlier and will mature only after 10, 15 and 20 years as may be desired.

Thanks

Hi, There are no put-call options. thanks, Vidya

Can you please tell me how can I buy Tax free bonds physically (not using dmat account)?

Hi Mitun, You can buy with any financial product distributor. thanks, vidya

there is some talk that when interest rates fall in the future maybe 1-3 years out .. there will be an opportunity to trade these tax free bonds, please can you explain what this means? theoretically what if interest rates fall what will be the impact on the returns an investor holding these tax fee bonds can make.

Thanks in advance !

Hi Gaurav, yes when yields fall, there is a price rally as they adjust to the new lower yields. Hence, tax-free bonds, along with other long-term bonds can see a price rally (pl. note that long-term bonds already say much rally last year). But the risk with tax-free bonds is that the liquidity is not high. Hence it may be tough to find takers in the market, esp. at a time when everybody tries to sell to lock in to price rallies.

For investors who simply hold the bond, the impact is nil as the interest rate (the payout) does not change (only the yields traded in the market changes). thanks.

Hi vidya………

I want to know – is it ever possible that we want to liquidate the BOND (in normal scenario and not when bench mark interest rates are too low or like wise) – we may not get any buyer for buying this Bond for few months….in that case we shall be ready to hold investment for full tenure…..please explain on this aspect

thanks,

Axay Shah

Hi Axay, I assume you are talking about tax-free bond. Tax-free bonds are erratically traded and hence it may not be always easy to find takers in the market. Also, if you sell at the wrong price (you need to track debt market closely to get it right), you will lose. Hence, it is best to invest with the full tenure in mind as a retail investor. Thanks, Vidya

I am aged 45 and took VRS due to some health issues. I have savings of around 1 Crore. I have invested this in a mix of equity & Debt funds. I am working as an engineeriung consultant but not in a bigway, earning around 2-3 lakhs in a year.

will it be a good idea to invest 5 lakhs in a 20 year tax free bond?

Regards

Melly Thomas

Hello melly, if you need a regular source of income then you can consider the tax-free bond. Otherwise, a mix of deposits and mutual funds should be good enough. thanks.

Your inputs on different queries has been educative. Appreciate your precise and understandable answers. Thank you.

Welcome. Thanks. Vidya

Hi Vidya,

I wish to invest in PFC tax free bonds in physical form as i do not have a demat account. Can these bonds be redeemed earlier than the maturity period? If yes, then what value would i get?

Regards,

Dev

Hello Dev,

If you invest in tax-free bonds in physical form, youc annot sell them in the stock exchange. if you need to sell before the maturity period, you will have to sell in the exchange (you have to hold ind emat) at the price at which it is traded then. the price may be above or below your purchase price, based on market yields. hence, for a retail investor, a buy and hold till maturity is a better strategy for bonds. thanks, Vidya

Hello Vidya

Thanks for detailed blog.Can you suggest some tax free bonds for year 13-14 and I think they will fall under 80ccf. Any option to invest online as I have online demat account

Hello Gaurang, 80CCF bonds are infrastructure bonds. they are not available this financial year. Tax-free bonds are different. they are merely long-term bonds where the interest income is tax free. there is no tax deduction on the principal under any of the Sec 80 provisions. thanks, Vidya

Hello Vidya

Thanks for detailed blog.Can you suggest some tax free bonds for year 13-14 and I think they will fall under 80ccf. Any option to invest online as I have online demat account

Hello Gaurang, 80CCF bonds are infrastructure bonds. they are not available this financial year. Tax-free bonds are different. they are merely long-term bonds where the interest income is tax free. there is no tax deduction on the principal under any of the Sec 80 provisions. thanks, Vidya

Dear Friends,

Can u tell me hudco tax free bonds, ntpc ta free bonds when coming.

Helo Chetan, One tranche of HUDCO bonds issue is over. they may come out again. NTPC has just got approval. The dates are not yet out. Thanks

Hello Vidya

I would prefer that pl. do not to give my email in your reply.

if one retail investor buys a tax free bond and later gives gift to NRI close relatives is it possible,,,are there any tax issues in INDIA,,,one may not be able to sell but one can give gift????does close relative needs PAN no.

Kiran, I am afraid you will have to check with your auditor on this one. You will have capital gains on transfer but whether it will be treated as income in recipient’s hand is something you need to check. Gift tax is not applicable for ‘clsoe relative’ But pl. get the definition of ‘relative’ clarified.

To Vinay Wagle:- One cannot redeem the principal amount before the maturity period (say 10 years), but you can sell it in the secondary market at BSE or NSE stock exchanges using your demat+trading account. It is not like Bank FD in this aspect. Still liquidity is based on the trading at the moment. So you may sell it for higher return or lower. (prevailing discounts at the time). In a sense it acts like a stock in your portfolio till the maturity period.

can you pl tell me whether the nominee will get the full value of the tax free bond before maturity on surrendering to the concerned company in case of the death of the bond holder

hello, As far as I get, the nominee can only hold the bonds in his/her name and not surrender prematurely. If there is liquidity in the debt market, the same may be sold. thanks

Hi Vidya,

Have seen your various advises above.

If an NRI wants to Invest in these Tax Free Bonds from their NRO account in India, is that allowed. Will the Interest also be free of Tax for them.

Does Funds India also assist in developing a suitable Portfolio.

Rgds

Rajeev Gupta

Hello Rajiv, First check if the bonds are allowed for NRIs. While most of them are allowed, some aren’t. For instance, currently HUDCO does not allow NRI investments.

As for bank account, investment would be allowed on a non-repatriation basis if you invest through an NRO account. If you wish to repatriate you will need a NRE account. As for interest, it is tax free in India. but whether you would have to declare in the country of your residence would depend on the tax laws of country you are residing in. You would need a demat account with FundsIndia or quote an existing demat account no. (if you have them with any other broker), to buy through FundsIndia. You may call +91 7667 166 166 or contact@fundsindia.com to help you with this.

thanks, Vidya

Hi,

As u have mentioned hudco bonds cannot be bought by NRIs. I am a resident Indian and had bought hudco bonds. Now I am planning to shift base to outside India. What should be done now? Can I continue to hold the bonds or do I have to sell before I become NRI? What if I don’t get buyers?

hello Bikram, you need not sell it. Since you were a resident Indian at the time of buying, it holds good. But if there is any change in your bank account etc. pl. intimate your distributor or the company. thanks, Vidya

Hi Vidya,

I am not sure whether I am a welcome guy here on this thread or not, but just wanted to clarify that the current HUDCO issue allows “Eligible NRIs” to invest in its tax-free bonds. So, if somebody wants to or has already invested in these bonds, there is no such issue and he/she can very well do that.

Hi,

I am an NRI but my wife is a house wife and indian resident. I moved to india recently for next couple of years. Can you pls. suggest good investment options and whether i should invest on my name or my wife as she doesn’t have any other income and can save better with low tax bracket. Is NRI FD(quarterly interest paid with zero tax) is better than annual interest paid tax free bonds?

Thanks.

Venkat

Hi Venkat, if you have completed 180 days here, then you would become resident Indian (provided you are still a citizen of India).You can invest in your name as well if you are investing for the long term in equity mutual funds. They are anyway tax exempt if held for more than a year. I hope youa re aware that over the long term of 5-20 years, equity funds have proven to generate returns superior to all other asset classes like debt or gold.

If you wish to have advice in this regard, request you to complete your formalities with opening your FundsIndia account and you can receive our fund advice by using the ‘Ask Advisor feature (click help tab) in your FundsIndia account.

The current rates offered by tax free bonds would be superior to NRI deposits. But if you still have your NRI status, not all tax-free bonds will be available for you. Hence, you can consider investing in your wife’s name.

In any other investment which is taxable, pl. note the clubbing provisions of Income tax may be attracted if you invest your savings in your wife’s name. Although gift is exempt, the income arising from such gift/investment is taxable in the hands of the person who gifted. thanks, Vidya

my son is green card holder in USA , he is interested to invest in tax free bonds. How can he invest while staying in US. He does not have any demat account but have saving account in Axis bank. Please guide

PCG

Hello sir,

If you son has the status of an ‘NRI’ then some bonds allow investment by NRI. You need to first find whether the bonds that are open allow NRIs. If you do not have a demat, you will have to seek offline distributors to make the investment. thanks, Vidya

Can you please clarify which tax-free bonds can be purchased by US citizen holding PIO card and living permanently in India?

Hello, Yes, provided the bond is available for investment by NRIs. You can provide proof of PIO card while applying. Some tax-free bonds are not open for NRIs. thanks.

Ma’am, can you please specifically name some bonds that accept investments from US citizens?

Hi Vidya,

Read with interest your views on Tax free bonds.

My query is – whether the cap of 10 lacs for retail investor (for higher interest rate) is per tranche of same Issuer say HUDCO ? OR

Can a retail investor invest max of 10 lacs each in say REL/HUDCO/PFC/NHPC/IIFCL and still get ‘Tax Free Interest Income’ ?

hello Girish, The cap is for each issue and not a total cap. thanks, Vidya

I would want to know whether a Individual or a HNI can invest any amount of money in these tax free bonds ? Like for example if i want to invest 50 crs as a individual can i do so ?

Is there a limit to tax free interest or i will continue to get tax free interest on any investment done.

If i buy a tax free bond of 15 years and want to sell it after 5 years on exchange will i be liable to pay any capital gain tax , if i sold in profits.

If the PSU like IRCTC goes in loss , is there a gaurantee that i will continue to get tax free interest on my investment.

Will the Interest rate on the tax free bond remain stagnant for the next 15 years i.e. if i buy today for 8.5% , i will continue to get 8.5% irrelevant of where the interest rates are going in future ?

Hello Gary, yes you can invest any amount; over Rs 10 lakh would fall under HNI. the interest rates is highest only for retail investors. No limit on tax-free interest applies.

If you are able to sell it in the market (if ou find liquidity) capital gains will apply.

Given that they are PSUs and backed by govt, default of interest is unlikely.

Yes, the rate will remain fixed for the tenure of 10 or 15 years.

thanks

I would want to know whether a Individual or a HNI can invest any amount of money in these tax free bonds ? Like for example if i want to invest 50 crs as a individual can i do so ?

Is there a limit to tax free interest or i will continue to get tax free interest on any investment done.

If i buy a tax free bond of 15 years and want to sell it after 5 years on exchange will i be liable to pay any capital gain tax , if i sold in profits.

If the PSU like IRCTC goes in loss , is there a gaurantee that i will continue to get tax free interest on my investment.

Will the Interest rate on the tax free bond remain stagnant for the next 15 years i.e. if i buy today for 8.5% , i will continue to get 8.5% irrelevant of where the interest rates are going in future ?

Hello Gary, yes you can invest any amount; over Rs 10 lakh would fall under HNI. the interest rates is highest only for retail investors. No limit on tax-free interest applies.

If you are able to sell it in the market (if ou find liquidity) capital gains will apply.

Given that they are PSUs and backed by govt, default of interest is unlikely.

Yes, the rate will remain fixed for the tenure of 10 or 15 years.

thanks

Hi Vidya,

An intuitive search led me to this page and I was impressed to see our answers to all the queries that were posted.

I am NRI and in last six months I have invested in NRE-fixed deposits where the interest is tax free.

I do not see any advantage in tax free bonds when I am already getting similar returns that are tax free. Also my NRE account is re-patriable, just in case funds are needed overseas.

Correct me if I missed any thing.

THsnk,

Vishal

Hello Vishal, yes for NRIs NRE deposits make sense right now, given that there is no taxation locally at present. Only, we cannot be sure if NRE deposits can become taxable in some future date. On the other hand, tax-free bonds – as stated – will remain tax free. I only hope you do not have all your savings in NRE deposits; they are not vehicles for superior returns in the long run, especially, if you are still in your working life and not retired. Vidya

Dear Madam

I would like to invest in tax free bonds which are listed in exchanges. can you suggest me which is highest yielding listed bond which I can invest immediately. please reply…

Hello Sir, We do not have recommendations on secondary market bonds. We go with a buy and hold of primary issues. thanks, Vidya

hi Vidya

Cud u give me comprision on following points between NSC and Govt Bonds – tax free

1) Safety

2) Liquidity

3) Interest Rates

Secondly does govt bonds give cumulative options to pick up funds at maturity

Cud u give me comparision between latest 3 optionsof govt bonds of Enmore, Indian Renewable and IIFCL

fourthly is their capital gains in tax free govt bonds and when

further is there any risk or taxation when interest rates are down in markets

1. safety – both

2. liquidity – tax-free bonds offer slightly mroe liquidity as they are traded (but whether they are all liquid in the market is something we will know only when they are traded)

3. Rates: tax-free bonds right now offer better rates.

No cumulative option since interest is tax free. You may directly compare the rates of the 3 bonds you mentioned. Ennore Port has a slightly lower rating. IIFCL and IREDA are similar.

There is capital gain only if yous ell in the secondary market. Since you will get back only principal on maturity (interest paid out every year) there is no question of capital gain if you hold till maturity.

No risk if you hold till maturity. If you trade in the market, risk of timing wrong and getting lower price (if rates go up) exists.

thanks

vidya

pls suggest upcoming bonds and how do i apply

Pl. see our page for latest tax-free bonds..http://www.fundsindia.com/content/jsp/fixedDeposit/FixedDepositAction.do?method=showFixedDepositHome

you can register with us and apply if you have a demat account with us or with anybody else.

Good article Vidya. Considering highest rated tax free bonds along with highest interest option could be good bet to get tax free returns in longer run.

hi Vidya,

I have some tax free bonds in electronic form? If I want to sell them now, how to do that ?

If you wish to sell them before maturity, you have to place the trade using your brokerage account, like it is with shares. If the bonds are liquid enough, your trade will get executed. But first know the price at which they are trading before taking a call. thanks, Vidya

Dear Sir / Madam,

My PPF account is maturing by August end after 15 years. The options available to me are

1. extend the PPF account

2. Close the PPF account & invest the corpus ? where – Tax free bond etc

3. After investing the corpus open fresh PPF account

My initial plan was to invest the PPF corpus in FMP & take indexation benefit. But with the new budget norms GOI has increased the tenure upto 3 years. My age is 48 & I fall in the highest tax bracket. Kindly suggest

Thanks

Hello Deepak, You need to be clear about your investment time frame/goal and risk appetite. If you have a 15-year time frame, then why not invest a part on equity funds to earn far superior returns? You do not always have to look at tax benefits and earn mediocre returns. You have to wait for tax-free bond issue if you have to deploy the money and we do not know if they will be issued this fiscal. You can always open a PPF account but ensure you are sufficiently exposed to other asset classes such as equity to earn superior long-term returns. thanks, Vidya

I have invested in various Tax Free Bonds which stand in my D-MAT account. Will the nominee to D-MAT account automatically inherit these bonds or a separate nomination has to be provided to the issuer of the bonds.

Thanks and Regards

Hello Deepak, Ideally having a nomination in your demat should reflect in all your holdings in that demat. This is the case with equity holdings Do check with your broker if this is indeed the case with bonds as well. thanks, Vidya

Hi Vidya,

I have a question on the coupon rate applicable for tax free bonds. As many of them have diff coupon rates for retail and others. Suppose I had purchased bond worth 5 lakh during the IPO of the taxfree bond and buy more from secondary market and it crosses the retail limit ( 10 lakh ?) will

that mean will get lower coupon rate ( non retail) for the whole ?

Also when buying from secondary market ( and not crossing limit of 10 lakh) wiill get the retail coupon rate ? (even if the seller could be non retail )?

Viral, when you buy in the secondary market, you get the coupon rate of the bond that you buy. Bonds with different coupon will be traded. You are free to buy whichever you wish, based on the price and your requirement and carefully choosing the right one – as long as they are traded freely in the secondary market. There will be no such restriction once the bonds hit the secondary market. thanks, Vidya

Hi Vidya,

I have a question on the coupon rate applicable for tax free bonds. As many of them have diff coupon rates for retail and others. Suppose I had purchased bond worth 5 lakh during the IPO of the taxfree bond and buy more from secondary market and it crosses the retail limit ( 10 lakh ?) will

that mean will get lower coupon rate ( non retail) for the whole ?

Also when buying from secondary market ( and not crossing limit of 10 lakh) wiill get the retail coupon rate ? (even if the seller could be non retail )?

Viral, when you buy in the secondary market, you get the coupon rate of the bond that you buy. Bonds with different coupon will be traded. You are free to buy whichever you wish, based on the price and your requirement and carefully choosing the right one – as long as they are traded freely in the secondary market. There will be no such restriction once the bonds hit the secondary market. thanks, Vidya

Hi

I am a little confused on where should I invest my money in.

My requirements are high returns and easy liquidity.

Which of the following should I go for :

PPF or Tax Free Bonds or FDs..

Please help..Thanks in advance

Hi Arpit, You have not stated the overall time frame of your investment. If you want reasonable returns with a short time frame like say 1 year, then ultra short-term funds are your best choice. These are debt funds that have reasonably low risk and highly liquid. Currently, they deliver returns of over 9% (1 year). In PPF and tax-free bonds your money is totally locked for the said time period. If you need money within few months, then liquid funds are options. thanks, Vidya

Hi,

Can you please confirm that there are no put-and-call option in these tax free bonds indicating the bonds will not be recalled earlier and will mature only after 10, 15 and 20 years as may be desired.

Thanks

Hi, There are no put-call options. thanks, Vidya

Are tax-free bonds suitable for NRIs who are resident of USA? They would have to pay tax on these bonds to IRS at 30%. For US persons, is it better to go with taxable bonds?

Hello Vikas, If an NRI is looking at long-term investment that will provide high post-tax returns, then you will have to settle for equity mutual funds or equities. Or you will have to weigh fixed-income investment opportunities in the US and see how much the tax-free bonds will deliver against that, after IRS tax. For instance, post IRS tax, the returns on a 8.39% 10-year HUDCO tax-free bond will only be 5.8%. Would you have better fixed income opportunities in the US that will deliver post tax returns is something you need to consider.Thanks.

Which Bond is good to invest (PFC/NHPC/IIFCL) up to 35 Lakhs Rs., Please suggest Bonds are better or Debt Funds, Equity Funds etc.

I Fall in to 30% bracket please suggest. Where I can place my funds – As of now I am keeping my funds in FSDs –

Vidya Could you suggest –

hello Nishant, Unless you need a yearly income flow, debt funds make more sense for long-term investing ,both on liquidity and return grounds, as mfs enjoy capital gains indexation for investment over 1 year. You can at best use tax-free bonds as a diversifier and go for the one with higher returns for 10 years (PFC/NHPC have higher returns) although IIFCL carries slightly lower risk than the other 2.

Equity funds are not to be compared with debt products as their risk-return profile is different. Every portfolio should have some exposure to equity if the time frame is long term. How much equity would depend on one’s risk appetite and time frame.

Thanks

Hi Vidya

I was just reading your article oIn this regard, I would request you to help me with some tax related inputs based on my case study.

I have recently got admitted in an US University for doing doctoral study. I am married and have a kid, who will remain in India presently. I have some bank balance and some shares in demat account. Now I need to generate steady source of income for my famility back in India. As I understand that my resident a/c will be designated as NRO account after I become an NRI.

Initially I thought of selling my shares and invest the sale proceeds in tax free bonds, which will generate steady returns sufficient for my family. I read that interest earned on my NRO deposit will be taxed at 30.90% unless tax residency certificate is provided. What I am not clear about is whether the interest from these tax free bonds( which would have otherwise remained tax free interest if I were an Indian Resident), which will get credited to my NRO account will become taxed and if so at what rate? is it flat 30.9% or as per prevailing income tax slabs?

Taxing the entire interest income from bonds will be very severe for me. Please suggest if you have any alternative planning for the given case study.

Hello Sumanta,

Sorry for the delayed response. First, not all tax-free bonds are available to NRIs. If they are, they are tax-free here as far as I understand. However, you may have to disclose it as income in the US and get taxed there. You would do well to consult an auditor in this regard. And of course tax-free bonds will close by March 31. Only if fresh approvals by govt. is made will you have any new issues after that. One option may be for you to make the investments through your spouse. thanks, Vidya

Thanks Vidya.

I am scared of the stock market – I dont see anything positive/high growth in the world these days.

Shouldn’t NRIs just go with taxable NCDs like Shriram/Muthoot etc which are giving ~12%. Based on my reading of the DTAA, IRS will take ~15% and GOI will take ~15%, post tax returns can be ~8.5%.

hello Vikas, Pl. remember that the risk of a tax-free bond and NCD is not alike. the former carried almost nil credit risk as they are issued by government enterprises. If you are ok with the risks, then it you may go for NCDs. thanks

Hi Vidaya

Can you please explain the major difference between NCDs, Bonds and Fixed Deposits/ Term Deposits ? Also what would be the treatment of interest for tax purposes for each of these entities ? Submitting form 15H/G would entile you for no TDS for each of them ? Thanks

Hello Sivakumar, NCDs and bonds are issued by companies or NBFCs and based on the company’s financial performance may be risky or low on risk. Deposits of companies and NBFCs too fall in the same category in terms of risk. They are also not secured. That means, you will get your money after many other lenders, if the company does bust. But while NCDs and bonds are listed in the debt market, deposits are not. Terms deposits are deposits of banks.

The interest in all the cases, except tax-free bonds (interest is free of tax), are added to your income and taxed at your slab rate. You will have TDS if you cross Rs 10,000 per year as interest for bank deposits. For NCDS and corporate deposits, such limit is Rs 5000 per year. Pl. note that whether TDS is deducted or not, all such income is taxable. You have to declare the entire interest at the end of the year while filing tax and pay tax on it. thanks, Vidya

Would you have info on date /month of issue for upcoming tax free bonds for rest of the year? Would help to plan cash for investment..thanks..ramesh

there is some talk that when interest rates fall in the future maybe 1-3 years out .. there will be an opportunity to trade these tax free bonds, please can you explain what this means? theoretically what if interest rates fall what will be the impact on the returns an investor holding these tax fee bonds can make.

Thanks in advance !

Hi Gaurav, yes when yields fall, there is a price rally as they adjust to the new lower yields. Hence, tax-free bonds, along with other long-term bonds can see a price rally (pl. note that long-term bonds already say much rally last year). But the risk with tax-free bonds is that the liquidity is not high. Hence it may be tough to find takers in the market, esp. at a time when everybody tries to sell to lock in to price rallies.

For investors who simply hold the bond, the impact is nil as the interest rate (the payout) does not change (only the yields traded in the market changes). thanks.

Hi vidya………

I want to know – is it ever possible that we want to liquidate the BOND (in normal scenario and not when bench mark interest rates are too low or like wise) – we may not get any buyer for buying this Bond for few months….in that case we shall be ready to hold investment for full tenure…..please explain on this aspect

thanks,

Axay Shah

Hi Axay, I assume you are talking about tax-free bond. Tax-free bonds are erratically traded and hence it may not be always easy to find takers in the market. Also, if you sell at the wrong price (you need to track debt market closely to get it right), you will lose. Hence, it is best to invest with the full tenure in mind as a retail investor. Thanks, Vidya

Your inputs on different queries has been educative. Appreciate your precise and understandable answers. Thank you.

Welcome. Thanks. Vidya

I am aged 45 and took VRS due to some health issues. I have savings of around 1 Crore. I have invested this in a mix of equity & Debt funds. I am working as an engineeriung consultant but not in a bigway, earning around 2-3 lakhs in a year.

will it be a good idea to invest 5 lakhs in a 20 year tax free bond?

Regards

Melly Thomas

Hello melly, if you need a regular source of income then you can consider the tax-free bond. Otherwise, a mix of deposits and mutual funds should be good enough. thanks.

Can you please tell me how can I buy Tax free bonds physically (not using dmat account)?

Hi Mitun, You can buy with any financial product distributor. thanks, vidya

Hi Vidya,

I wish to invest in PFC tax free bonds in physical form as i do not have a demat account. Can these bonds be redeemed earlier than the maturity period? If yes, then what value would i get?

Regards,

Dev

Hello Dev,

If you invest in tax-free bonds in physical form, youc annot sell them in the stock exchange. if you need to sell before the maturity period, you will have to sell in the exchange (you have to hold ind emat) at the price at which it is traded then. the price may be above or below your purchase price, based on market yields. hence, for a retail investor, a buy and hold till maturity is a better strategy for bonds. thanks, Vidya

To Vinay Wagle:- One cannot redeem the principal amount before the maturity period (say 10 years), but you can sell it in the secondary market at BSE or NSE stock exchanges using your demat+trading account. It is not like Bank FD in this aspect. Still liquidity is based on the trading at the moment. So you may sell it for higher return or lower. (prevailing discounts at the time). In a sense it acts like a stock in your portfolio till the maturity period.

Hi,

I am an NRI but my wife is a house wife and indian resident. I moved to india recently for next couple of years. Can you pls. suggest good investment options and whether i should invest on my name or my wife as she doesn’t have any other income and can save better with low tax bracket. Is NRI FD(quarterly interest paid with zero tax) is better than annual interest paid tax free bonds?

Thanks.

Venkat

Hi Venkat, if you have completed 180 days here, then you would become resident Indian (provided you are still a citizen of India).You can invest in your name as well if you are investing for the long term in equity mutual funds. They are anyway tax exempt if held for more than a year. I hope youa re aware that over the long term of 5-20 years, equity funds have proven to generate returns superior to all other asset classes like debt or gold.

If you wish to have advice in this regard, request you to complete your formalities with opening your FundsIndia account and you can receive our fund advice by using the ‘Ask Advisor feature (click help tab) in your FundsIndia account.

The current rates offered by tax free bonds would be superior to NRI deposits. But if you still have your NRI status, not all tax-free bonds will be available for you. Hence, you can consider investing in your wife’s name.

In any other investment which is taxable, pl. note the clubbing provisions of Income tax may be attracted if you invest your savings in your wife’s name. Although gift is exempt, the income arising from such gift/investment is taxable in the hands of the person who gifted. thanks, Vidya

Hi,

As u have mentioned hudco bonds cannot be bought by NRIs. I am a resident Indian and had bought hudco bonds. Now I am planning to shift base to outside India. What should be done now? Can I continue to hold the bonds or do I have to sell before I become NRI? What if I don’t get buyers?

hello Bikram, you need not sell it. Since you were a resident Indian at the time of buying, it holds good. But if there is any change in your bank account etc. pl. intimate your distributor or the company. thanks, Vidya

Hi Vidya,

I am not sure whether I am a welcome guy here on this thread or not, but just wanted to clarify that the current HUDCO issue allows “Eligible NRIs” to invest in its tax-free bonds. So, if somebody wants to or has already invested in these bonds, there is no such issue and he/she can very well do that.

Dear Friends,

Can u tell me hudco tax free bonds, ntpc ta free bonds when coming.

Helo Chetan, One tranche of HUDCO bonds issue is over. they may come out again. NTPC has just got approval. The dates are not yet out. Thanks

Hello Vidya

I would prefer that pl. do not to give my email in your reply.

if one retail investor buys a tax free bond and later gives gift to NRI close relatives is it possible,,,are there any tax issues in INDIA,,,one may not be able to sell but one can give gift????does close relative needs PAN no.

Kiran, I am afraid you will have to check with your auditor on this one. You will have capital gains on transfer but whether it will be treated as income in recipient’s hand is something you need to check. Gift tax is not applicable for ‘clsoe relative’ But pl. get the definition of ‘relative’ clarified.

can you pl tell me whether the nominee will get the full value of the tax free bond before maturity on surrendering to the concerned company in case of the death of the bond holder

hello, As far as I get, the nominee can only hold the bonds in his/her name and not surrender prematurely. If there is liquidity in the debt market, the same may be sold. thanks

Hi Vidya,

Read with interest your views on Tax free bonds.

My query is – whether the cap of 10 lacs for retail investor (for higher interest rate) is per tranche of same Issuer say HUDCO ? OR

Can a retail investor invest max of 10 lacs each in say REL/HUDCO/PFC/NHPC/IIFCL and still get ‘Tax Free Interest Income’ ?

hello Girish, The cap is for each issue and not a total cap. thanks, Vidya

Hi Vidya,

Have seen your various advises above.

If an NRI wants to Invest in these Tax Free Bonds from their NRO account in India, is that allowed. Will the Interest also be free of Tax for them.

Does Funds India also assist in developing a suitable Portfolio.

Rgds

Rajeev Gupta

Hello Rajiv, First check if the bonds are allowed for NRIs. While most of them are allowed, some aren’t. For instance, currently HUDCO does not allow NRI investments.

As for bank account, investment would be allowed on a non-repatriation basis if you invest through an NRO account. If you wish to repatriate you will need a NRE account. As for interest, it is tax free in India. but whether you would have to declare in the country of your residence would depend on the tax laws of country you are residing in. You would need a demat account with FundsIndia or quote an existing demat account no. (if you have them with any other broker), to buy through FundsIndia. You may call +91 7667 166 166 or contact@fundsindia.com to help you with this.

thanks, Vidya

my son is green card holder in USA , he is interested to invest in tax free bonds. How can he invest while staying in US. He does not have any demat account but have saving account in Axis bank. Please guide

PCG

Hello sir,

If you son has the status of an ‘NRI’ then some bonds allow investment by NRI. You need to first find whether the bonds that are open allow NRIs. If you do not have a demat, you will have to seek offline distributors to make the investment. thanks, Vidya

Can you please clarify which tax-free bonds can be purchased by US citizen holding PIO card and living permanently in India?

Hello, Yes, provided the bond is available for investment by NRIs. You can provide proof of PIO card while applying. Some tax-free bonds are not open for NRIs. thanks.

Ma’am, can you please specifically name some bonds that accept investments from US citizens?

Hi Vidya,

An intuitive search led me to this page and I was impressed to see our answers to all the queries that were posted.

I am NRI and in last six months I have invested in NRE-fixed deposits where the interest is tax free.

I do not see any advantage in tax free bonds when I am already getting similar returns that are tax free. Also my NRE account is re-patriable, just in case funds are needed overseas.

Correct me if I missed any thing.

THsnk,

Vishal

Hello Vishal, yes for NRIs NRE deposits make sense right now, given that there is no taxation locally at present. Only, we cannot be sure if NRE deposits can become taxable in some future date. On the other hand, tax-free bonds – as stated – will remain tax free. I only hope you do not have all your savings in NRE deposits; they are not vehicles for superior returns in the long run, especially, if you are still in your working life and not retired. Vidya

Dear Madam

I would like to invest in tax free bonds which are listed in exchanges. can you suggest me which is highest yielding listed bond which I can invest immediately. please reply…

Hello Sir, We do not have recommendations on secondary market bonds. We go with a buy and hold of primary issues. thanks, Vidya

hi Vidya

Cud u give me comprision on following points between NSC and Govt Bonds – tax free

1) Safety

2) Liquidity

3) Interest Rates

Secondly does govt bonds give cumulative options to pick up funds at maturity

Cud u give me comparision between latest 3 optionsof govt bonds of Enmore, Indian Renewable and IIFCL

fourthly is their capital gains in tax free govt bonds and when

further is there any risk or taxation when interest rates are down in markets

1. safety – both

2. liquidity – tax-free bonds offer slightly mroe liquidity as they are traded (but whether they are all liquid in the market is something we will know only when they are traded)

3. Rates: tax-free bonds right now offer better rates.

No cumulative option since interest is tax free. You may directly compare the rates of the 3 bonds you mentioned. Ennore Port has a slightly lower rating. IIFCL and IREDA are similar.

There is capital gain only if yous ell in the secondary market. Since you will get back only principal on maturity (interest paid out every year) there is no question of capital gain if you hold till maturity.

No risk if you hold till maturity. If you trade in the market, risk of timing wrong and getting lower price (if rates go up) exists.

thanks

vidya

pls suggest upcoming bonds and how do i apply

Pl. see our page for latest tax-free bonds..http://www.fundsindia.com/content/jsp/fixedDeposit/FixedDepositAction.do?method=showFixedDepositHome

you can register with us and apply if you have a demat account with us or with anybody else.

Good article Vidya. Considering highest rated tax free bonds along with highest interest option could be good bet to get tax free returns in longer run.

Dear Sir / Madam,

My PPF account is maturing by August end after 15 years. The options available to me are

1. extend the PPF account

2. Close the PPF account & invest the corpus ? where – Tax free bond etc

3. After investing the corpus open fresh PPF account

My initial plan was to invest the PPF corpus in FMP & take indexation benefit. But with the new budget norms GOI has increased the tenure upto 3 years. My age is 48 & I fall in the highest tax bracket. Kindly suggest

Thanks

Hello Deepak, You need to be clear about your investment time frame/goal and risk appetite. If you have a 15-year time frame, then why not invest a part on equity funds to earn far superior returns? You do not always have to look at tax benefits and earn mediocre returns. You have to wait for tax-free bond issue if you have to deploy the money and we do not know if they will be issued this fiscal. You can always open a PPF account but ensure you are sufficiently exposed to other asset classes such as equity to earn superior long-term returns. thanks, Vidya

hi Vidya,

I have some tax free bonds in electronic form? If I want to sell them now, how to do that ?

If you wish to sell them before maturity, you have to place the trade using your brokerage account, like it is with shares. If the bonds are liquid enough, your trade will get executed. But first know the price at which they are trading before taking a call. thanks, Vidya

I have invested in various Tax Free Bonds which stand in my D-MAT account. Will the nominee to D-MAT account automatically inherit these bonds or a separate nomination has to be provided to the issuer of the bonds.

Thanks and Regards

Hello Deepak, Ideally having a nomination in your demat should reflect in all your holdings in that demat. This is the case with equity holdings Do check with your broker if this is indeed the case with bonds as well. thanks, Vidya