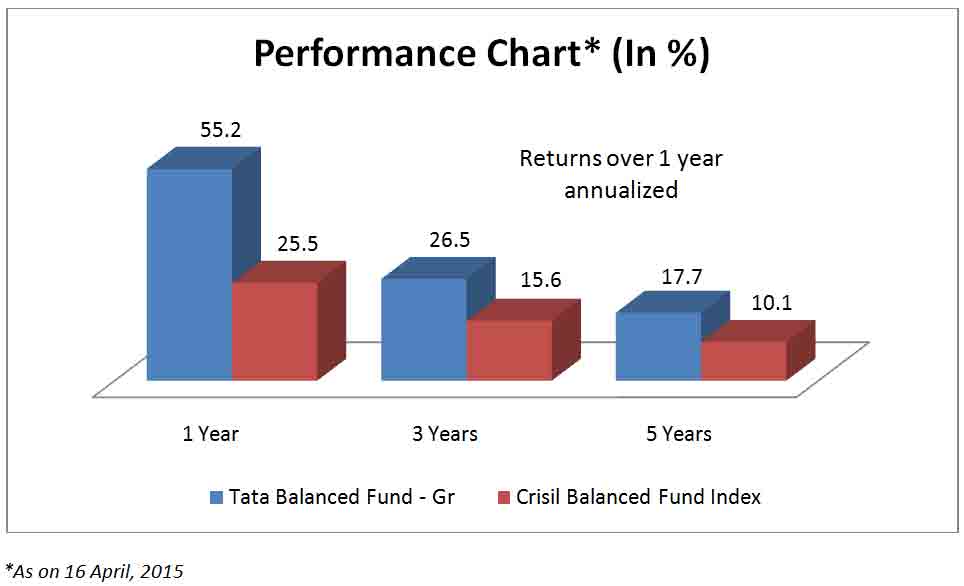

If you are starting out on a long-term portfolio, or are looking for participation in equity albeit with less volatility, you can consider investing in the Tata Balanced Fund. This equity-oriented fund, with about three-fourth of its assets in equities and the rest in debt, has a track record of delivering 17.7 per cent annually in the last 5 years. That’s not only a good 7.5 percentage points higher than the CRISIL Balanced Fund Index, but is also superior to the average returns of diversified equity funds by a similar margin.

Suitability

Tata Balanced Fund has a long track record, having been launched in the last quarter of 1995, making it witness several market ups and downs.

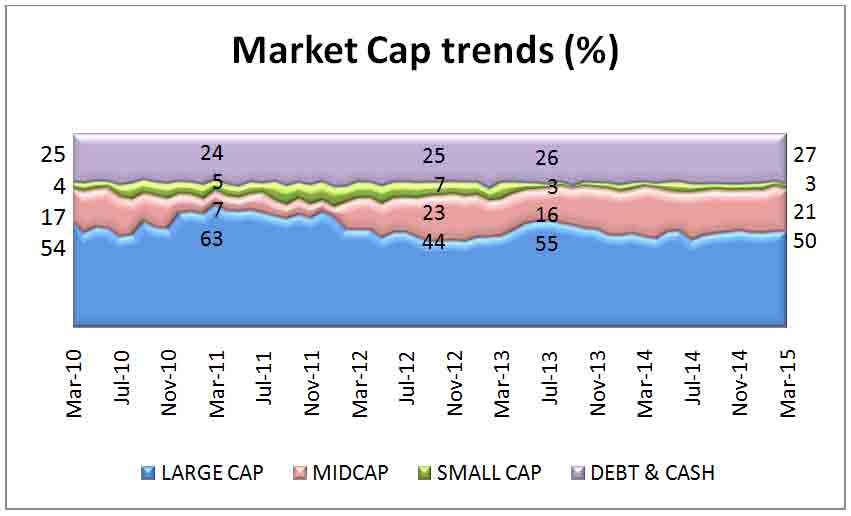

The fund invests about 70-75 per cent of its assets in equities on most occasions. While peers such as ICICI Pru Balanced Fund reduced their equity holding to 65 per cent levels, Tata Balanced Fund seldom reduced its holding below the 70 per cent mark in recent years. The benefit of such a holding is that the fund outperforms its index and peer groups by a significant margin in up markets.

In 2007 and 2009, for instance, the fund beat established peers such as HDFC Balanced Fund and ICICI Pru Balanced Fund by a massive 20-30 percentage points. On the flip side though, the fund does fall more than its peers in down markets. Hence, while you can expect this fund to contain declines better than diversified equity funds, if you are more conservative, you will do well to hold the above-mentioned peer funds over Tata Balanced Fund.

Dividend Payout Option: Tata Balanced Fund has a unique option that may help even relatively conservative investors looking for regular payouts. The fund has a monthly dividend payout option that was started in August 2010. Since then, it has been paying investors who chose this option every single month, although the quantum of dividends varied based on market conditions. Over the last one year, it has declared an average 3 per cent dividend every month.

Hence, for a retired investor with investments diversified across other fixed income products, this fund could be a good option to take exposure to the equity class.

Performance

Had you started a Rs. 10,000-a-month SIP in Tata Balanced Fund 10 years ago, you would have a handsome Rs. 32 lakh today. That’s an annual yield of 19 per cent. The benchmark, Crisil Balanced Fund Index, on the other hand, would have fetched just Rs. 21.9 lakh; that’s an Internal Rate of Return of 11.6 per cent annually.

Since 2000, Tata Balanced Fund has outperformed the benchmark by a cumulative 80+ per cent. On a rolling one-year return basis for the last 3 years, the fund beat its benchmark 88 per cent of the times. Over the last one year, the fund outperformed most of its peers by a good margin.

As mentioned earlier, Tata Balanced Fund has mostly sought to hold equities above the 70 per cent mark, even in down markets such as 2008 and 2011, although its peers reduced their holdings to around 65 per cent. This higher exposure though, delivered handsomely when markets moved to the green. In 2009, for instance, the fund managed a whopping 72 per cent return, a feat achieved by just a couple of other peers who held higher mid-cap stocks.

Portfolio

Tata Balanced Fund follows the Growth-At-Reasonable-Price (GARP) style, and stocks are selected on a bottom-up basis backed by rigorous research. The mid-cap focus is on niche businesses backed by high entry barriers like technology, brand franchise, distribution network, and relatively higher growth rate.

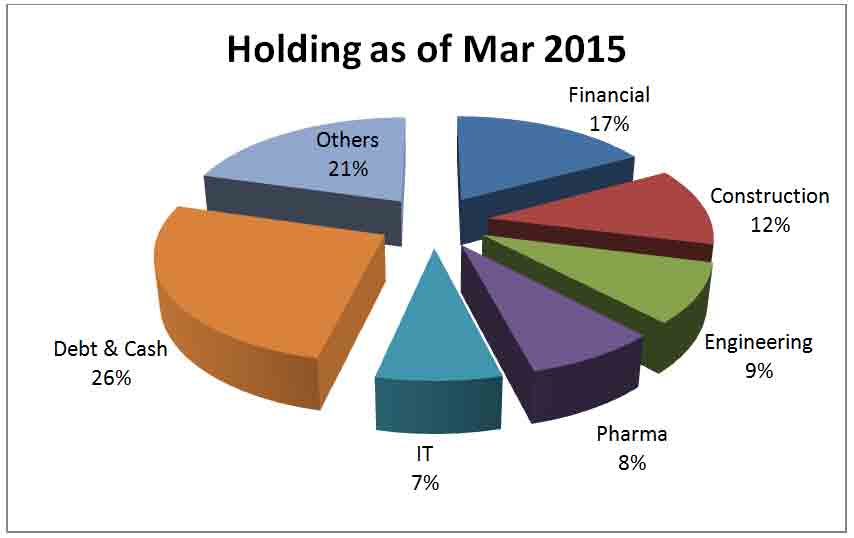

As of March 2015, 50 per cent of the fund’s total equity holdings were in large-cap stocks, and 21 per cent and 3 per cent were in mid-cap and small cap stocks respectively. The fund holds a more diversified portfolio of about 68 stocks over 15 different sectors. Its top 10 holdings account for 32 per cent of its portfolio. It also sports a low portfolio turnover ratio (just 0.56 times).

In its debt portfolio, the fund holds a good 16 per cent in gilt instruments, evidently to keep the portfolio’s credit risk at bay. It holds about 6 per cent in debentures and 4 per cent in money market instruments.

Like most other funds, the banking and financial sector remains the fund’s top pick, followed by construction, engineering and pharma.

HDFC Bank, Eicher Motors, Axis Bank, HCL Technologies, and Infosys were some of its top picks in the large cap (10,000 to 25,000 crore market cap) space. Sadbhav Engineering, VA Tech Wabag, Cera Sanitaryware, and Strides Arcola were some of its top picks in the mid-cap space (5,000 to 10,000 crore market cap).

*Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Past performance is not indicative of future results. To know how to read our weekly fund reviews, please click here.

Good article. Would also like to see information on fund manager, his/her style of investing/redemption, and also some samples of his/her calls during different market conditions, like you usually do.

If someone invests through SIP of a particular amount in a Balanced Fund for, say, a period of five years then her/his cost of units will get averaged over five years. Equities as an investment tends to follow ‘reversion to mean’ principal where in the markets tend to revert to mean either from a rise or a fall. Therefore, theoretically, over a long period (five years or above) of SIP in Balanced Funds (least volatile amongst equity funds) should result in a situation where in at least the capital will get protected from erosion. The returns may wary depending on the equity cycle at that moment. I was just wondering, could it be possible?

Yes, you are absolutely right. We can expect good returns from this category over the next five years.

Thanks

Sathya

We see nearly all good mutual funds NAV has gone up considerably in the last 1 year. This is also the case for Tata Balanced Fund. So do you think it is still a good time to invest lumpsump ? In case the market sees correction, some capital erosion would be inevitable unless the investors stays put for a long time ? OR do you think in today’s situation debt funds are better placed than balanced funds – specially for the investors who would like to make reasonable profit without taking a risk on capital ? Thanks.

Hello Sir, If you are not willing to take risks, equity funds and balanced are not for you. Capital risk is always high in the near term with equities. Such risk, though, diminishes over the long term.

As to your point on NAVs going up, NAVs are not like stock prices. They represent a basket of stocks and such a basket keeps changing. In other words, if a stock is very highly valued, the fund make book profits or exit and look for other opportunities. As they make profits, their NAV grows. That does not mean NAV is inflated. As long as a fund manager does not allow his portfolio fo stocks to be too overvalued and looks for new opportunities, the fund will always be worth investing from a long term perspective.

Thanks, Vidya

Looking for suggestions!!

If I want to invest in Tata Balanced fund for one year. what would be the return? I have gone through the performance graph and it seems that if I invest for long term such like more than one year, then the return will be good, unless I will have to bear loss. Is my observation correct?

Thanks,

Ankit Gupta

Hi Ankit,

Tata Balanced Fund requires a holding period of at least three years. It has a debt component, yes, but its predominantly equity and thus needs a longer horizon. Equity funds do deliver superior returns, as you have observed, only over such long time periods and not in periods of one year. The equity market is also correcting now due to domestic and global factors and will remain so until uncertainties are ironed out.

Thanks,

Bhavana

Looking for suggestions!!

If I want to invest in Tata Balanced fund for one year. what would be the return? I have gone through the performance graph and it seems that if I invest for long term such like more than one year, then the return will be good, unless I will have to bear loss. Is my observation correct?

Thanks,

Ankit Gupta

Hi Ankit,

Tata Balanced Fund requires a holding period of at least three years. It has a debt component, yes, but its predominantly equity and thus needs a longer horizon. Equity funds do deliver superior returns, as you have observed, only over such long time periods and not in periods of one year. The equity market is also correcting now due to domestic and global factors and will remain so until uncertainties are ironed out.

Thanks,

Bhavana

I m ready to plan out regard hybrid funds..

I m ready to plan out regard hybrid funds..

Hi There,

I needed a suggestion regarding investment. I have an option, whether to invest in Tata Balanced funds or SBI magnum balanced fund. Which of these would yield better returns over a period of say 2 to 3 years? Also are the interests earned on these investments are tax free?

Thanks,

Anuj

Hello Anuj,

If you are a FundsIndia customer, please route your query through the advisor appointment feature in your accoutn and we will answer it. We are constrained from offering portfolio-specific advice in this forum. To answer your other question, all gains in equity and balanced funds (there is no interest only gain) held for more than 1 year are exempt from tax.

thanks,

Vidya

Hi There,

I needed a suggestion regarding investment. I have an option, whether to invest in Tata Balanced funds or SBI magnum balanced fund. Which of these would yield better returns over a period of say 2 to 3 years? Also are the interests earned on these investments are tax free?

Thanks,

Anuj

Hello Anuj,

If you are a FundsIndia customer, please route your query through the advisor appointment feature in your accoutn and we will answer it. We are constrained from offering portfolio-specific advice in this forum. To answer your other question, all gains in equity and balanced funds (there is no interest only gain) held for more than 1 year are exempt from tax.

thanks,

Vidya

I am 62 years old male. Retired from service. Getting monthly government pension.

I want to further invest good amount in mutual funds.

I have already invested in Axis Long Term Equity Fund(ELSS), Tata Balanaced Fund (MD).

Please advise me if Large Cap funds, Balanced Funds or Debt funds would be suitable for me?

I have in mind to get some monthly dividend at present.

Kindly advise

P Kumar

Hello sir, Sorry for the delayed reponse.

Individual advice is based on understanding of the customer and his profile and portfolio. If you are a FundsIndia customer, please write to us or talk to your advisor, so that we can help you. thanks, Vidya

I am 62 years old male. Retired from service. Getting monthly government pension.

I want to further invest good amount in mutual funds.

I have already invested in Axis Long Term Equity Fund(ELSS), Tata Balanaced Fund (MD).

Please advise me if Large Cap funds, Balanced Funds or Debt funds would be suitable for me?

I have in mind to get some monthly dividend at present.

Kindly advise

P Kumar

Hello sir, Sorry for the delayed reponse.

Individual advice is based on understanding of the customer and his profile and portfolio. If you are a FundsIndia customer, please write to us or talk to your advisor, so that we can help you. thanks, Vidya

Good article. Would also like to see information on fund manager, his/her style of investing/redemption, and also some samples of his/her calls during different market conditions, like you usually do.

If someone invests through SIP of a particular amount in a Balanced Fund for, say, a period of five years then her/his cost of units will get averaged over five years. Equities as an investment tends to follow ‘reversion to mean’ principal where in the markets tend to revert to mean either from a rise or a fall. Therefore, theoretically, over a long period (five years or above) of SIP in Balanced Funds (least volatile amongst equity funds) should result in a situation where in at least the capital will get protected from erosion. The returns may wary depending on the equity cycle at that moment. I was just wondering, could it be possible?

Yes, you are absolutely right. We can expect good returns from this category over the next five years.

Thanks

Sathya

We see nearly all good mutual funds NAV has gone up considerably in the last 1 year. This is also the case for Tata Balanced Fund. So do you think it is still a good time to invest lumpsump ? In case the market sees correction, some capital erosion would be inevitable unless the investors stays put for a long time ? OR do you think in today’s situation debt funds are better placed than balanced funds – specially for the investors who would like to make reasonable profit without taking a risk on capital ? Thanks.

Hello Sir, If you are not willing to take risks, equity funds and balanced are not for you. Capital risk is always high in the near term with equities. Such risk, though, diminishes over the long term.

As to your point on NAVs going up, NAVs are not like stock prices. They represent a basket of stocks and such a basket keeps changing. In other words, if a stock is very highly valued, the fund make book profits or exit and look for other opportunities. As they make profits, their NAV grows. That does not mean NAV is inflated. As long as a fund manager does not allow his portfolio fo stocks to be too overvalued and looks for new opportunities, the fund will always be worth investing from a long term perspective.

Thanks, Vidya