DSP Equity Opportunities fund has traditionally been a volatile, opportunistic fund that can swing either way, heavily, in the short term. This large & midcap equity fund had one such volatile year in 2018 and is now showing some early signs of a recovery. Investors willing to take volatility or are investing through SIP can add this fund as part of their core portfolio. The fund’s 5-year return of 16.9% is a good 2.5 percentage points more than its benchmark S&P BSE 500 TRI and is also 1.5 percentage points higher than the category average. The fund’s 3-year return may not be quite comparable to the benchmark as the fund had a largecap bias until the change in categorization in 2018.

Returns are as of March 26, 2019

The fund and suitability

DSP Equity Opportunities is a go-anywhere fund. That means it can invest across market caps and across sectors. The fund not only seeks ‘opportunities’, but also takes some concentrated bets in its top stocks. For example, ICICI Bank accounts for 9% of its portfolio now. This trait, together with its ‘opportunistic’ characteristic, lends an additional element of risk to this fund compared with some peers. In fact, the fund scores among the top 5 funds in its category if 5-year SIPs are considered. This merely suggests heightened volatility and therefore better averaging.

The fund can be a good addition to a long-term portfolio. It is important to note that the fund (and other large & midcap funds) has lower exposure to large caps compared with peers in the multicap category. Essentially, large & midcap funds carry a higher risk than multicap funds in terms of market cap exposure. For those not wanting direct exposure to midcap funds, DSP Equity Opportunities serves to provide adequate midcap exposure.

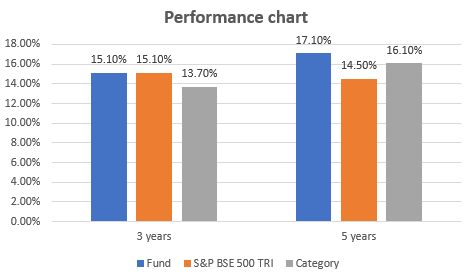

Performance

DSP Equity Opportunities beat the benchmark Nifty 500 TRI 75% of the times when 3-year returns were rolled daily for 5 years. That is not the best in the category but superior to the category’s outperformance (66% of the times) of the benchmark. The fund has a high risk-adjusted return (measured by Sharpe). But its standard deviation, which speaks of the swings in its return, suggests how volatile the fund can be. This is true on the downside as well. In 2018, for instance, the fund fell by 9% even while its category declined by 7.6%.

Portfolio

It is not wrong to call DSP Equity Opportunities an ‘impatient’ fund. The fund does not tolerate underperformance for long. Similarly, it does not hesitate to book profits when it sees some money on the table. This quality has been in vogue for several years now. As a result, the fund typically has a high portfolio turnover ratio compared with other funds.

If we take the past one year the following churns were made: the fund exited Yes Bank in September 2018, when the first spell of trouble was seen. Stocks such as BPCL, Bank of Baroda, Federal Bank, and ITC were well shown the door for poor performance while money was taken off the table early on from Bajaj Finance, Jubilant Foodworks, and Ashok Leyland, when the going was good. But then the fund has also incurred a cost for its impatience, at times. For example, the fund exited Havell’s India by October 2018 although the stock continued to deliver.

| Top exits over the past year | Top entries in the past year |

|---|---|

| Bank of Baroda | Axis Bank |

| BPCL | Jindal Steel & Power |

| Mahindra & Mahindra | Sun Pharmaceuticals |

| ITC | IPCA Laboratories |

| Shree Cements | LIC Housing Finance |

Some of the opportunistic but well-balanced moves came in the banking space. The fund not only accumulated stocks of giants such as ICICI Bank and Axis Bank on attractive valuations and rehaul of lending practices, but also added smaller and fast-growing players such as City Union Bank and RBL Bank.

While DSP Equity Opportunities has traditionally been biased towards a cyclical portfolio, it did not fail to curtail the pain from such exposure in 2018. It significantly cut back on exposure in the auto space and pruned holdings in cement, construction, and energy. It instead marginally increased holdings in consumer, IT, and pharma.

The fund’s biggest bet remains the banking and financial service space. Adjustments in the construction space (despite pruning) and some quality additions to the industrial manufacturing space can be bets that can play out post elections. The fund adequately made up for the cyclical exposure through exposure to consumer plays such as HUL and Dabur India and by increasing holdings in stocks such as Kansai Nerolac Paints, Hatson Agro Products, and V-Guard Industries.

Its portfolio moves appear to suggest that while the fund may be aggressive, it is certainly not willing to pay too high a price for growth.

The fund is managed by Rohit Singhania.