That the software sector is struggling is old news. Software results declared so far aren’t inspiring either. One AMC expanded the scope of its IT fund, while another plans to merge its technology fund with a diversified fund. Earlier in the year, equity funds had still seen some promise in the sector. A good share of large-cap funds were still overweight on the software sector, compared to the Nifty 100 and Nifty 500 indices. The steady and foreseeable growth, lower valuations, and the expectation that companies were adapting strategies to cope with the changing dynamics held funds’ attention.

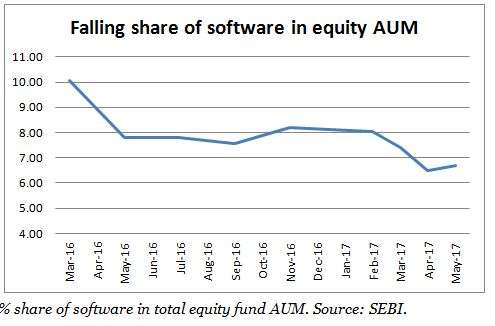

That appears to have dampened now. In the past couple of months, most large cap and diversified funds dropped stake in software and become underweight on the sector. Across all equity funds, SEBI data shows the software share at 6.7% of the total AUM in May, against the 10.6% in January 2016. The sector has now ceded the second spot in terms of AUM share to NBFC and related finance stocks. The falling share is also a function of the software stocks’ worsening market performance, apart from fund action.

That appears to have dampened now. In the past couple of months, most large cap and diversified funds dropped stake in software and become underweight on the sector. Across all equity funds, SEBI data shows the software share at 6.7% of the total AUM in May, against the 10.6% in January 2016. The sector has now ceded the second spot in terms of AUM share to NBFC and related finance stocks. The falling share is also a function of the software stocks’ worsening market performance, apart from fund action.

Going underweight

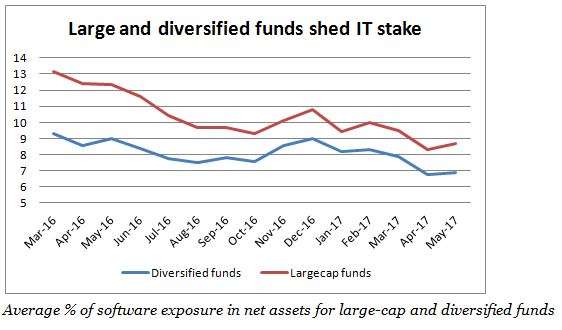

Large-cap funds are wont to hold software stocks given that the sector makes up the second-highest holding in the indices after banking and the large-cap universe features a good number of software stocks. Given the growth hiccups in the sector, funds would obviously have turned away from the sector. But the sector’s share in fund portfolios has not been an unbroken march downwards.

While funds did begin to reduce stake in mid-2016, several large-cap funds moved back into picking up software stocks in late 2016 post the US elections. That valuations were lower, especially after the market fall, and concerns seemed overdone could have prompted funds to pick up stake. They have now turned around and cut back. Most funds now hold at best maintain portfolio weight at the same level as software has in the Nifty 100, if not below it.

Up until February 2017, about half the 50-odd large-cap funds held exposure to the software sector at levels above that of the Nifty 100 index. The index weight has been around 10-13% in the past year. By the time April and May 2017 rolled around, only 2 in every 10 funds held software stakes at levels above the index. On an average, funds held 8.7% in the sector in May 2017, against the 12.4% the preceding May. Even contrarian and value-oriented funds dropped holding as the March quarter results showed continued pressure on numbers, and post the various bonus and buyback bonanzas.

For diversified or multicap funds, already fewer of them had been overweight on the sector compared to the Nifty 500 index. Given the sizeable proportion of mid-cap stocks that funds could take, there would be a lesser need to invest in large software companies. As with large-cap funds, the last quarter of 2016 and early 2017 saw diversified funds lift stakes only to pare it back in the past couple of months. Until March 2017, about a third of the 56 funds in the universe had held software stocks more than the 9-12% that the Nifty 500 has. As of May 2017, 2 in every 10 funds were overweight on the sector.

For diversified or multicap funds, already fewer of them had been overweight on the sector compared to the Nifty 500 index. Given the sizeable proportion of mid-cap stocks that funds could take, there would be a lesser need to invest in large software companies. As with large-cap funds, the last quarter of 2016 and early 2017 saw diversified funds lift stakes only to pare it back in the past couple of months. Until March 2017, about a third of the 56 funds in the universe had held software stocks more than the 9-12% that the Nifty 500 has. As of May 2017, 2 in every 10 funds were overweight on the sector.

(This article was first publised in The Economic Times Online)