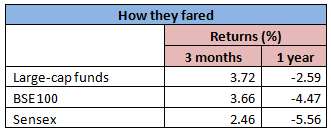

It has been quite a ride for the stock market, and especially large-cap stocks, since the Sensex peaked slightly above the 30,000 mark in March last year. The BSE 100 index, which represents large-cap stocks, is down 2.9 per cent in the year to date and 4.5 per cent for the year. But from the low in February this year, the index staged a comeback.

Returns of large-cap funds consequently slid sharply and then recovered smartly from the February 2016 low. The nature of the market rally in March and April have also seen funds with a cyclical portfolio tilt recover. Here’s what large-cap funds have done in the past year.

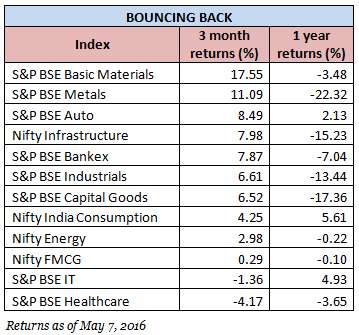

Making a comeback

As the euphoria from the strong election faded in 2015, and reform and growth predictions met with a reality check, the market headed south. From the high in March 2015 to the low hit in February this year, the BSE 100 index dropped a steep 17.8 per cent. The loss in the Sensex and the Nifty 50 were also around the same levels. Large-cap funds, on an average, lost 17 per cent. These funds have most of their picks coming from the top 100 or 200 stocks by market capitalisation.

But post the largely positive Budget, a return of foreign portfolio investors, fears over a US rate hike receding, and a prediction of normal monsoons this year, the market began to recover. Foreign Portfolio Investments (FPIs) ploughed in a net Rs. 29,558 crore in March and April alone, after being net sellers in nearly every month since last March. The BSE 100 index, thus, gained 11 per cent from March to date. The BSE LargeCap index, which is another representative of the large-cap segment, rose 18 per cent.

What’s different in this recent revival is that sectors and stocks that bore the brunt of the market fall in 2015 were accorded more importance. In the past three months, sectors that have logged the strongest gains are from the cyclical basket, recouping a good part of the losses they had made in the past year or so.

For one thing, these stocks were beaten down and thus, were ripe for plucking. Two, these stocks were trading at more reasonable valuations than the high-quality or consumption-themed basket. Three, efforts to clean up the banking system, rate cuts and their transmission into lower rates, signs of an uptrend in core industries, improvement in freight rates and commercial vehicle sales, all suggest that the worst of the economic slump is past, and the hitherto stagnant manufacturing and capital goods sectors can revive. Four, predictions of a normal monsoon and no sharp hike in MSP prices both point to steady inflation and a rural revival. Five, government spending on roads, railways, urban and rural infrastructure can also improve fortunes of the industrial sector.

Common causes

On an average, large-cap funds registered a loss of 2.6 per cent for the one-year period compared to the 4.5 per cent loss for the BSE 100 index. The uptick from the February low helped erase a good bit of the heavy losses several funds had suffered. In fact, at the February low the one-year average loss was 18 per cent.

Unlike mid-cap funds, the investible universe for large-cap funds is much smaller and there’s lesser scope for deviation from the index weights. One stock most funds held among their top ten was Maruti Suzuki, whose swift correction pulled down returns. Similarly, the underperforming ITC was an addition to several fund portfolios, being among the few reasonably valued FMCG stocks. Other popular stocks include Infosys and Reliance Industries; the comparatively better run of these stocks countered the falls to some extent.

In another thread running through most large-cap funds, the mild to steep correction in two fund favourites – software and pharmaceuticals – hit hard. Similarly, banking and financial services, the third must-have sector, had a rough time over 2015 and 2016, and this has affected the entire large-cap fund basket.

Fund performance

Outside these three main sectors pulling down returns, funds had different weights to sectors such as industrials, cement, oil & gas, telecom, automobiles, and so on. The differences in these sector weights played a role in the extent of the fund’s fall, and their recovery. Some funds followed the value strategy, with a long-term bet on economic revival, more than others. This resulted in their portfolios having exposure to sectors such as construction, oil & gas, petroleum, power, industrials, and so on. So while they slipped badly in the past year, their recent performance has picked up.

HDFC Top 200, for example, held over a third of its portfolio in financial services in August 2015. Within this sector, it held severely beaten down stocks such as SBI, ICICI Bank and Axis Bank. DSP BlackRock Top 100 leaned towards energy, construction, and industrials. ICICI Prudential Select Largecap was weighted towards energy and metals, while UTI Opportunities had a tilt towards construction. These funds were among the worst performers, with the one-year loss between 20 to 24 per cent at the low in February.

In the middle of the pack – losing between 16-18 per cent were ICICI Prudential Focused Bluechip Equity, Birla Sun Life Frontline Equity, Canara Robeco Large Cap+, and L&T India LargeCap. Even in the recent market upswing, these funds remained in the mid-quartile, indicating lower volatility in returns. While the ICICI fund was banking-heavy, it also held NBFCs such as Bajaj Finserv and auto company, Mahindra & Mahindra, that stemmed the fall. The Birla fund also held the better banks, as well as stocks such as Hero Motocorp and Grasim Industries.

SBI Bluechip was among the best in containing losses. It had a much lower banking exposure than its peers, and instead had higher holding in consumer goods and auto. So was BNP Paribas Equity, for which consumer stocks such as Asian Paints, Jet Airways, and Hero Motocorp worked well. Franklin India Bluechip, while holding a good amount of banking stocks had the better ones such as IndusInd Bank, Kotak Mahindra Bank, and Yes Bank, and thus, kept losses in check. Motilal Oswal Focused 25 countered its banking heavyweight with concentrated holding in stocks such as Eicher Motors, CRISIL, and Britannia, which did not fare too badly. Kotak Select Focus was another one that managed to keep its losses lower than its peers. Holding cement stocks that didn’t correct much, apart from names such as Britannia, helped. Cement holdings also helped the fund make strong returns in the market revival.

But the market’s recent love for cyclical sectors and beaten down stocks helped funds that relied on this theme cut back a good part of their losses. Stocks such as ICICI Bank, SBI, and Bank of Baroda gained between 6 and 14 per cent in from March. L&T, another popular stock for large-cap funds, was up 12 per cent while Tata Motors shot up 26 per cent. Cement stocks that funds held gained between 7 to 30 per cent.

The three-month return has thus seen some of the worst performers clock the highest return. Of course, this short term bounce back does not definitely indicate that the funds will continue to be the top performers over the long term. While market volatility persists, signs point to a gradual broad-based revival in both corporate revenue and profitability. The takeaway from the roller-coaster ride in the past year is that patience and a long-term perspective is needed.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

I believe that the last sentence says it all . Incisive article this one, compliments to the author .

I believe that the last sentence says it all . Incisive article this one, compliments to the author .