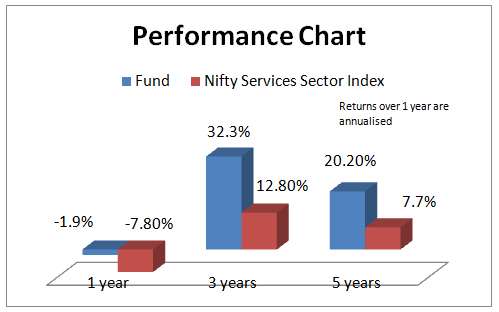

There are some funds in the mutual fund universe whose super-normal returns can be intriguing. ICICI Pru Exports and Other Services Fund is one of them. With an annualised return of 32.3 per cent in the past three years, the fund is way ahead of its index – the Nifty Services Sector (12.8 per cent annually), as well as the multi-cap equity fund average (17.8 per cent annually). Of course, that this is a broad-based theme fund lends higher risk and higher return potential. Still, how did the fund manage the returns that it did? Would its prospects continue to remain high?

The Fund

ICICI Pru Exports and Other Services Fund was launched at the end of 2005 under the name ‘ICICI Pru Services Sector’, and was renamed in 2013. As the name suggests, it is a theme fund, albeit with a broad universe including software, media, transport, pharma and auto ancillaries. The renaming provided clarity in terms of its scope of investment, including export-oriented sectors such as pharma and auto ancillaries (although it was investing in such sectors even before the name change).

It is noteworthy that while the fund has the Nifty Services Sector as its benchmark, the index has high exposure to banking, unlike this fund. Also the index does not have exposure to pharma or other manufacturing, which fall more within the ambit of exports for the fund.

Performance

While ICICI Pru Exports and Other Services Fund picked winning stocks from various sectors, its key contributors across several years came from IT and pharma. Stocks from sectors such as auto ancillaries, capital goods, media, telecom, hotels, and pesticides also helped deliver superior returns to the portfolio. But these were not so much about sector exposure and timing; it was all about picking the right stocks at the right time. And the fund did well on that count too.

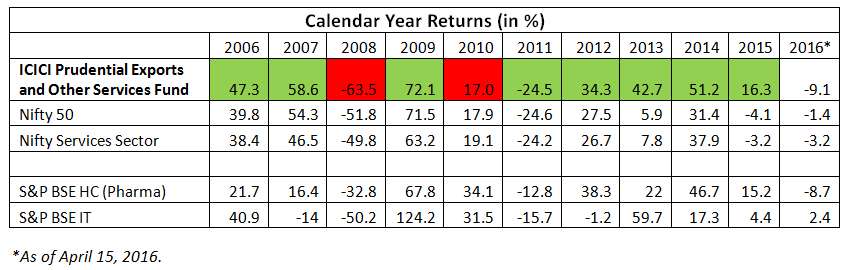

Take a look at the indices below and you will see where the fund’s returns came from. Either the pharma or IT sector, or both, have clearly managed to fuel the performance of the fund across years. Of course, that the fund outperformed these sectors too, in quite a few years, can be attributed to active stock picking across other sectors within the theme. We have highlighted in red, those years where the fund under-performed the Nifty or its own benchmark – the Nifty Services Sector.

The above data also suggests that the fund is not a defensive one. In years when the pharma or IT index contained declines better, the fund fell more. This was either due to exposure to other high beta sectors such as auto and capital goods, or due to exposure in relatively high-growth stocks within the IT or pharma space that also corrected sharply in a fall on account of premium valuation. That means the fund certainly carries higher risk than the seemingly defensive nature of the sectors it holds.

Surprisingly, on a rolling one-year return basis (taken for the past three years), the fund outperformed its benchmark almost 98 per cent of the times. That is a high level of consistency for a theme fund. Of course, it also suggests that the theme has been in prolonged favour in the markets.

Portfolio and stock choices

As of March 2016, pharma accounted for 34 per cent of the fund’s holdings, followed by IT at 28.4 per cent. In the past two years, some of the fund’s top picks came from outside these two sectors as well.

Over a two-year period, stocks such as Bharat Forge (capital goods) and PI Industries (pesticides) delivered well over 100 per cent absolute returns. In the pharma and IT space, NIIT, Lupin, Cipla and Sun Pharma were among those that contributed to portfolio returns.

However, winning stocks of earlier years such as Natco Pharma, and IPCA Laboratories, as well as larger ones such as Lupin and Pfizer have been on the correction mode, and have pulled down one-year returns, resulting in negative returns over the last six months to one year.

Prospects

How has this theme been working well despite the fact that exports in the country have not done well for a few years now? The returns stem from the performance of the pharma (growth) and IT (stability) space, and a few winning stocks outside it.

Structural bull run in pharma: Pharma companies were re-rated in the past five years, and stocks from this space have been beneficiaries of such a re-rating. This happened on the back of a strong revenue and earnings growth driven predominantly by Indian pharma companies diversifying into multiple geographies, with the US now accounting for about half of their revenue, India for a fourth, and the remaining coming from the rest of the world. Much of the growth came from generics, with India being the largest provider of generics globally.

Simultaneously, the Indian market and the demand for low cost generics here also meant healthy growth in the local market for Indian pharma companies. Other markets – Russia, Brazil, Mexico, South Africa, and Japan too became large export markets for Indian pharma companies.

According to research reports, the Indian pharma market is set to grow at 22 per cent compounded annually between 2015 and 2020. Companies that focus on research pipelines and new products in the US market, and generics in other developing markets, besides contract manufacturing, hold prospects over the next few years.

If you take IT, the sector may not have grown at the pace at which pharma grew, but saw pockets of out-performance in the mid-cap space, and stable growth in larger companies. This lent stability to this theme fund. Besides, one of the reasons behind this sector’s continued out-performance can be attributed to the depreciating rupee against the dollar. Just take the case of TCS (not held by this fund any longer) – In FY-12, while its revenue growth in dollar was 24.2 per cent (over a year ago), it was 31 per cent in rupee terms. Let’s take the just ended FY-16. Revenue growth in dollar terms was just 7.1 per cent. In rupee terms, it is double at 14.8 per cent. Clearly, the gains from the rupee’s depreciation did, and can continue to pep growth to this sector, though not at the pace at which it did in the last few years.

Looking at the above prospects, you may ask – so why not hold a pharma fund? Indian pharma companies have the maximum number of units catering to the US market (outside of the US) and have maximum product filings too for that market. This means, Indian pharma companies will increasingly be subject to stringent norms by the US Food and Drug Administration. Non-compliance of such norms can hurt in the near term, causing stock prices to react violently (as is seen already). Also, given the re-rating that has happened in the past five years, valuations would be a key, especially in a fall (where expensive stocks will be hit first).

For this reason, despite prospects being bright, higher volatility would mean the concentrated holding in pharma sector funds can hurt you if top holdings are hit.

Exposure through a broad theme fund such as ICICI Pru Exports and Other Services will likely ensure the volatility is less. Still, the fund remains high risk, and is suitable only for high-risk investors, and that too to the extent of 10-15 per cent of their portfolio value and not more.

It would be prudent not to expect the kind of returns that the fund delivered in the past as the re-rating story in its key sectors may not be repeated.

The fund is managed by Manish Gunwani and Yogesh Bhat.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.